Why I'm Buying Shares in Spotify

Why I'm Buying Shares in Spotify

Spotify ticks a lot of the boxes I look for in an investment: founder-led, market leadership, rapid product innovation, expanding margins, and a reasonable valuation. I'm a buyer at these levels.

This week I plan to initiate a starter position (1.5% portfolio weight) in the global audio streaming behemoth, Spotify (NYSE:SPOT). I’ve been casually researching Spotify for the past 24 months, but struggled to build enough conviction to pull the trigger and make an investment. However, two things changed for me in late 2021 which prompted me to take a deeper look at Spotify: (1) I switched from Apple Music to Spotify and have had a fantastic customer experience and (2) I listened to an outstanding pitch from TDM Growth Partners at the 2021 Sohn Hearts & Minds Investment Leaders Conference (see the pitch here), which articulated an excellent bull case for Spotify over the next 3-5 years. After spending the last few weeks digging into Spotify, it’s hard not to be bullish on the future of audio and Spotify’s role in that ecosystem. Here’s why.

1) Spotify is the dominant market leader in audio streaming which confers powerful network effects

At its core, Spotify offers two audio services: (1) music (established market leader) and (2) podcasts (recent market leader). Spotify purchases the rights to distribute music from the three record labels that control the majority of the market (Universal Music Group [AMS:UMG], Warner Music Group [NASDAQ:WMG], and Sony Music [TYO:6758]) and then resells that music to its customers, either through a paid subscription service or a free ad-supported version. Spotify also offers podcasts and recently overtook Apple (NASDAQ:AAPL) to become the largest podcast platform in the US (source), with over 3.2m podcasts available at the end of Q3 2021.

In Q3 2021, Spotify reported 381m total monthly active users (MAUs) with 172m (45%) of these being paid subscribers. Since Q1 2018, Spotify has, on average, gained 13.9m MAUs and 6.5m paid subscribers each quarter, almost like clockwork. There has not been a single quarter since Q1 2018 of quarter-over-quarter declines in total MAUs or paid subscribers.

How does this compare to competitors? As of Q1 2021, Statista reports that Spotify had a 32% market share of paid subscriptions in the global audio market, well ahead of competitors like Apple Music, Amazon Music (NASDAQ:AMZN), and YouTube Music (NASDAQ:GOOG). There are substantial network effects that come with being the dominant audio platform for consumers, including:

People naturally flock to the platform with the greatest brand recognition and most comprehensive range of content (music, podcasts, etc), which reduces Spotify’s customer acquisition cost (CAC) and enables them to spend more than competitors on the distribution rights for audio content.

Spotify acquires more data than their competitors (i.e., listening patterns, app engagement patterns, etc), which should help their recommendation algorithms to become more personalised and predictive over time.

Spotify is a cultural phenomenon with an almost cult-like following (at least in the West), which confers powerful network effects. I must admit that I was a first-hand victim of this cultural obsession with Spotify; the main reason I switched from Apple Music to Spotify (apart from primary market research) was to avoid awkward interactions with friends or colleagues who would express visible disgust and condemnation if I admitted to being a subscriber of Apple Music. Guess I’m not so contrarian after all …

2) Spotify: A future member of the exclusive FAANG club?

“History doesn’t repeat itself, but it often rhymes” (Mark Twain).

One of the most compelling aspects of TDM’s investment pitch on Spotify was their comparison between Spotify and constituents of the FAANG club at a circa $50b valuation. Indeed, at a $50b valuation, all companies shared the following six characteristics:

Clear market leadership;

Less than 15% market share of a $100b+ market (note: Spotify’s market share is sub 15% if we include non-linear audio, like radio).

Accelerating product innovation;

Growing competitive advantages;

Led by a visionary founder or founders; and

Trades at less than 14x forward gross profit.

Quite the comparison. If you cast your memories back to when each of the FAANG companies were valued at $50b (note: I was still in high school), it will come as no surprise how each of them performed since that point in time. Over the subsequent five years, each company generated stellar returns for investors, driven by an average 10% expansion in gross margins, and consistent outperformance of Wall Street estimates for both revenue and EBITDA growth. TDM Growth Partners (and quite possibly Mark Twain) foresees a similar fate for Spotify.

3) Radio still accounts for the majority of audio advertisement spend

According to Spotify internal estimates and third-party estimates, radio still receives more than 60% of global audio advertising spend. It is astonishing to me that radio — which I generally associate with shallow content and an almost insufferable amount of advertisements (particularly during peak hour traffic) — still constitutes such a large part of the global audio advertising market. As radio continues to decline in relevance and follows a similar path to what cable/traditional TV has experienced over the past decade, I believe Spotify as the dominant market leader in digital audio streaming is well positioned to capture a large portion of this advertising spend shifting towards music and podcasts. Some trends just seem inevitable.

While companies advertising via radio can choose specific radio stations and listening times that attempt to cater to their target demographic, advertising is still much less targeted than what digital streaming services like Spotify are able to offer. Think about the difference in return on investment (ROI) for a mortgage broker targeting millennials interested in purchasing their first home that advertises on: (1) a radio station with 40% millennial listenership at 5pm on a Wednesday afternoon when listeners are likely exhausted and mentally replaying events from work vs. (2) at the beginning of a podcast episode dedicated to helping millennials and gen z professionals navigate the process of purchasing their first home. In addition to more personalised ads, digital platforms like Spotify can provide much greater quantitative insight into the success of a marketing campaign (e.g., number of clicks, conversion rates, drop-out rates, etc) than traditional radio.

4) Audio is under-monetized compared to other forms of digital entertainment

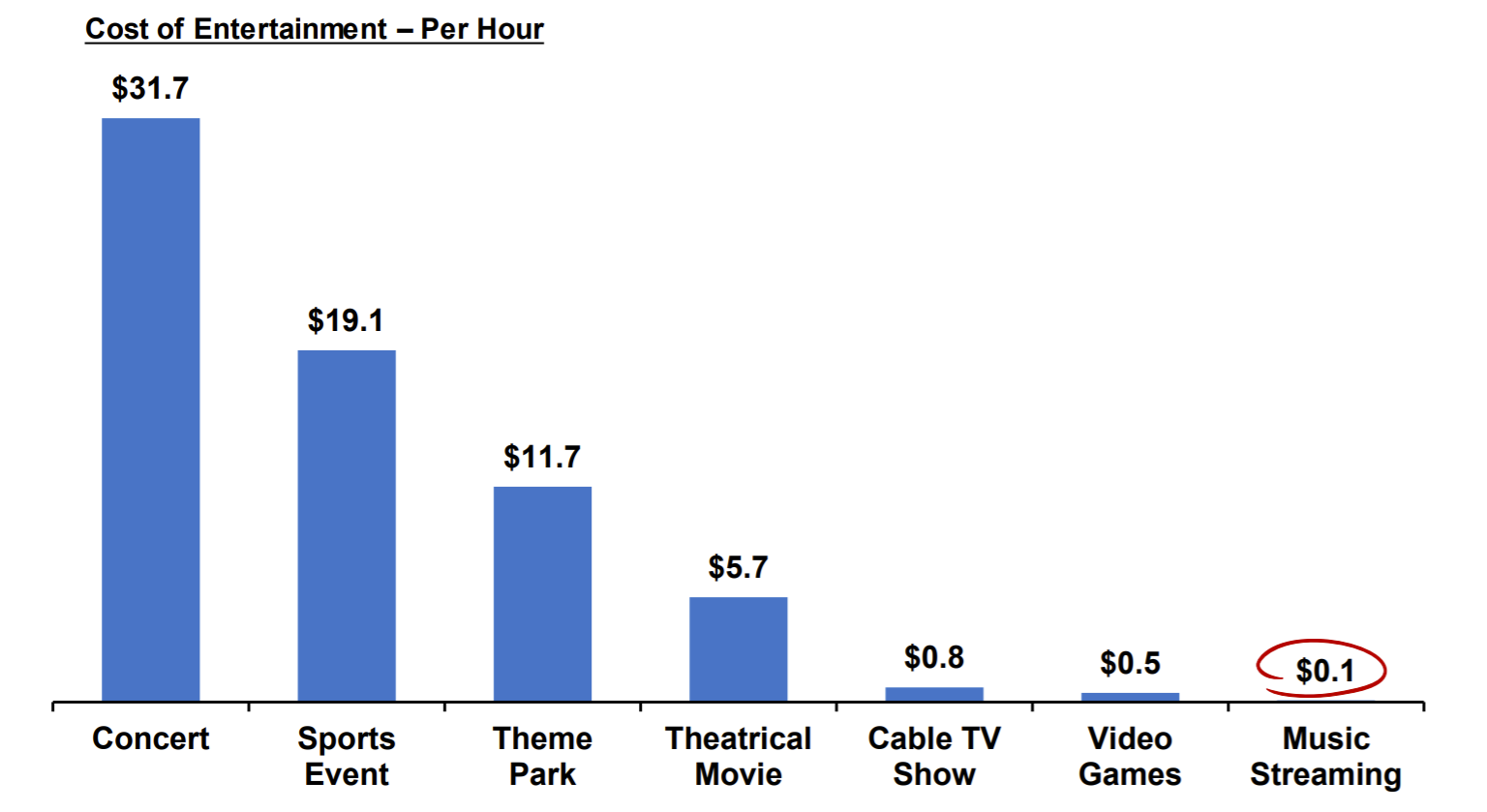

Spotify benefits from a number of long-term tailwinds, including the decline of radio and increasing consumer preferences for personalisation. Another tailwind for Spotify is that music streaming (and likely podcasts and audiobooks) is highly under-monetized relative to other forms of digital entertainment, such as attending a live concert, sporting event, or watching cable TV. And it’s not even close.

While people fork out up to $5.70 per hour to watch a movie in the cinemas or $0.80 per hour to watch cable TV at home, people spend a meager $0.10 per hour to stream music. When presenting the below figure, I am not arguing that music streaming should reach the same degree of monetization (in terms of cost per hour) as going to a live music concert or theme park, but it seems inevitable that over time digital streaming platforms will learn to better monetize the audio entertainment experience, either through higher subscription prices or a greater frequency of advertisements.

5) Rapid product innovation indicates Spotify is not resting on its laurels

Spotify’s pace of innovation over the past 24 months has been blistering, opening up additional opportunities for monetization while also strengthening their competitive position in the global audio market. Here are some of the innovations that Spotify has publicly announced in the past 24 months:

Spotify ‘Open Access Platform’ where artists can bring their existing subscriber base to Spotify and deliver paid content to them, for free.

Paid subscription platform (free until 2023) where podcasters can publish podcast episodes exclusive to paid subscribers, with Spotify charging a 5% fee for access to this tool.

Live audio events where creators and fans can discuss music, live sports, cultural events, etc, with the option of turning these conversations into a podcast.

Offering sponsored recommendations for artists, similar to YouTube recommended videos or Google AdWords.

Adding video versions of podcasts and interactive Q&A during podcasts to increase engagement.

These are logical innovations that enhance Spotify’s position as the ‘super-app’ of digital audio streaming. Adding live audio events emerged in response to the growth of Clubhouse and Twitter Spaces (NYSE:TWTR), while adding video podcasts and interactive Q&A helps Spotify compete with YouTube. Additional features like paid podcast subscriptions or sponsored artist recommendations should generate high-margin revenue that is accretive to gross margins.

Spotify’s ‘Open Access Platform’ also signals that Spotify is both aware of and planning ahead for a potential ‘Web 3.0 economy’ where artists have greater decentralised ownership over their audiences and assets. Spotify innovating in this domain is a great sign as disintermediation between creative artists and their audiences is one of the biggest existential threats to Spotify. More on this later.

6) Podcasts are a game changer for Spotify

After launching podcasts in 2015, Spotify has been investing heavily into building out their podcast database to compete with Apple Podcasts. In Q3 2021, Spotify reported organic growth of more than 100% in podcast advertising revenue, demonstrating significant traction (albeit off a much smaller base than the music side of their business).

Adding targeted ads to podcasts is a natural fit and offers an additional way for Spotify to monetize their ad-supported user base. Podcasts (at least compared to music) tend to be quite niche, enabling advertisers to market towards a specific target demographic, which should manifest in a higher ROI than generic above-the-line mediums (e.g., TV or radio).

Spotify should also be able to leverage lessons learned from their success in entering the podcast game to accelerate expansion into other identified audio verticals, such as:

Audiobooks (to compete with Audible and Apple Books).

Meditation apps (to compete with Calm and Headspace).

Given Spotify’s demonstrated track record of finding product-market fit with new innovations, I would not be surprised to see these audio verticals become meaningful contributors to revenue over the next 3-5 years.

7) Spotify is following the Netflix playbook with their investments in originals and exclusives

According to Hamilton Helmer in his seminal book ‘7 Powers: The Foundations of Business Strategy’, one of the pivotal moments in Netflix’s (NASDAQ:NFLX) success was their decision to invest in original and exclusive content. Why? Because it allowed them to translate their dominant market leadership (based on the number of paid subscribers) into a clear cost advantage.

Let’s use an example. If Netflix has 200m paid subscribers and it costs around $100m to produce season one of a potential award-winning TV show, that equates to a cost of $0.50 per paid subscriber. If a smaller competitor with 50m paid subscribers attempted to spend that same amount on a new TV show, the investment would be distributed across a smaller base of paid subscribers, resulting in a cost of $2 per paid subscriber, affecting their unit economics and margins. This scale advantage is a big reason behind Netflix’s success over the past decade.

In their Sohn conference pitch, TDM likened Spotify’s landmark $100m deal with comedian and UFC commentator, Joe Rogan, for the exclusive rights to his podcast show (the Joe Rogan Experience) to the success of Netflix’s ‘House of Cards’ in 2013. And Spotify has not only invested in Joe Rogan; they’ve invested in more than 200 original and exclusive podcasts over the past two quarters.

Similar to Netflix, Spotify has a much larger paid subscriber base than competitors, so investments in original and exclusive content can be distributed across a larger number of subscribers, affording them a cost advantage over Apple Music, Amazon Music, and YouTube Music. Originals and exclusives also help to draw more users into the Spotify ecosystem. Just think about how many people might have been content with their Apple Music subscription but were forced to swap to Spotify after they signed exclusive rights for the Joe Rogan Experience. At least a half-dozen of my friends.

However, one valid pushback to this argument of cost advantages from scale could be that, unlike Netflix’s competitors, Spotify’s competitors are flush with cash. So far, Apple, Amazon, and Alphabet all seem eager to invest some of their fortress balance sheets into original and exclusive content (so far mainly for TV streaming), but media is not their singular focus, so management must also consider opportunities to spend their cash outside of audio streaming. We’ll need to wait a few more years to truly judge whether Apple, Amazon, and Alphabet serve as genuine competitors to Spotify in terms of breadth of original and exclusive content.

8) Consistent and diversified revenue growth indicates demand is still strong

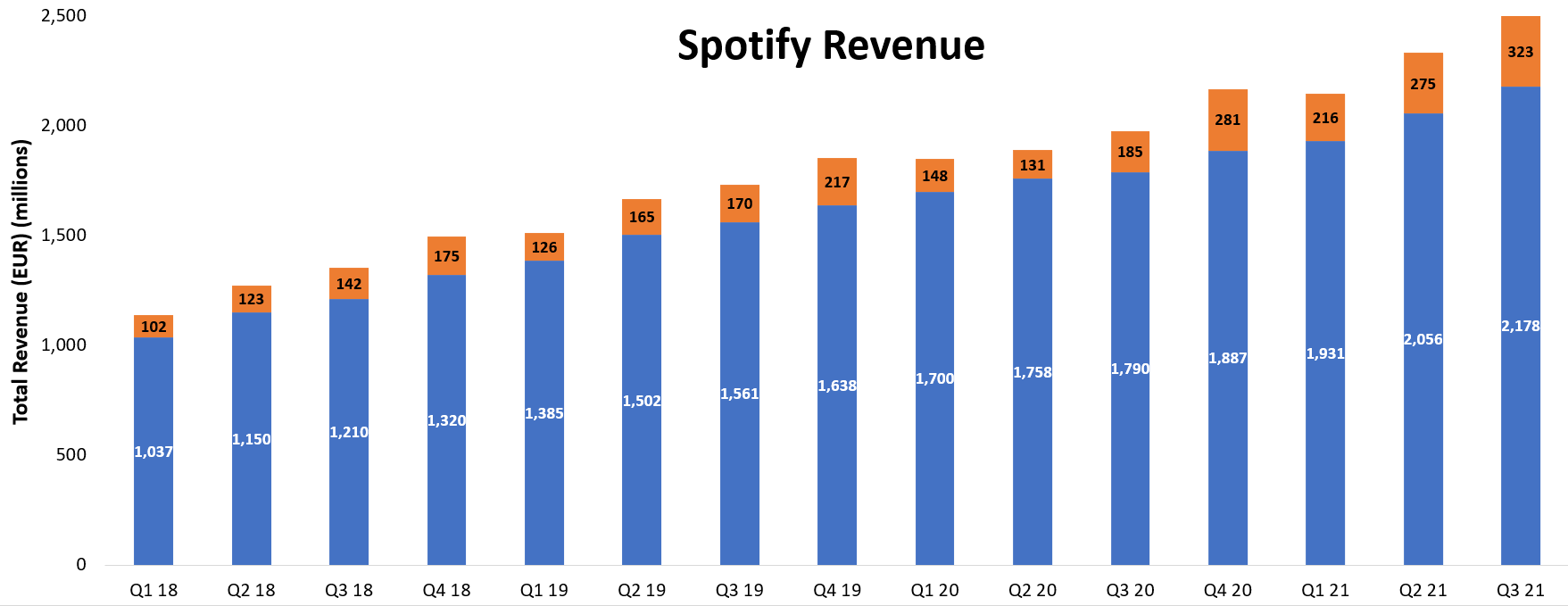

Spotify has reported consistent quarter-over-quarter revenue growth since Q1 2018, growing total revenues from €1.14b (Q1 2018) to €2.50b (Q3 2021) at a CAGR of 25%. Spotify’s revenue from paid subscribers (blue column) still accounts for 87% of total revenue and has grown at a CAGR of 24% since Q1 2018. Ad-supported revenue represents the remaining 13% of revenues and has grown at a faster CAGR of 39% since Q1 2018, albeit from a much smaller base.

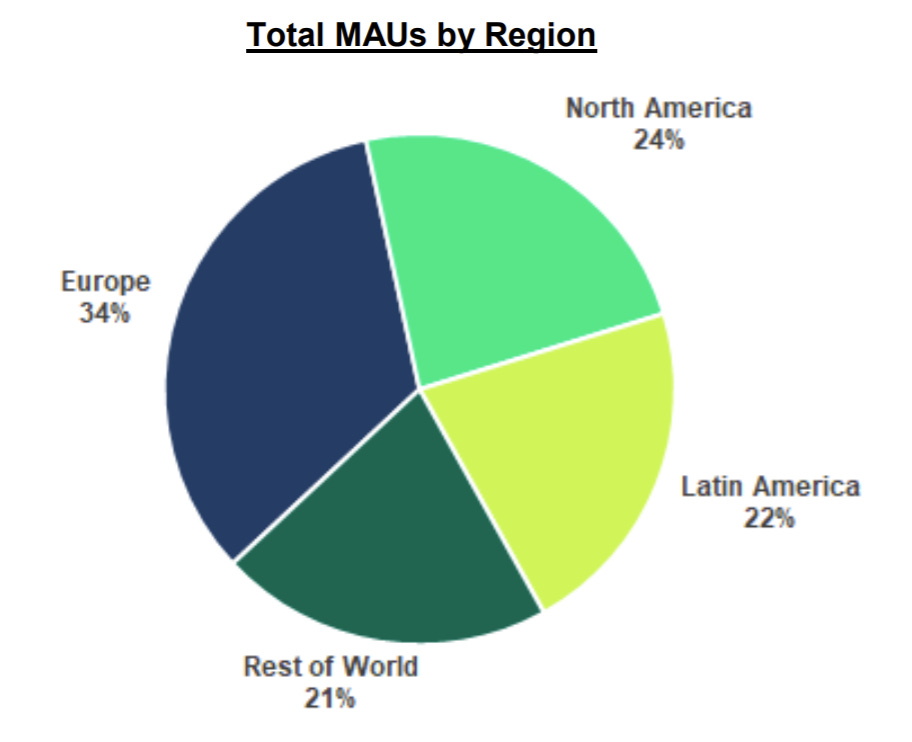

Spotify is also a truly global company with a very diversified subscriber base. Europe (34%) is their largest source of MAUs, followed by North America (24%), Latin America (22%), and rest of the world (21%).

9) Growth in podcasts and auxiliary services acts as a driver of gross margin expansion

Expanding gross margins are the critical ingredient for Spotify to become consistently profitable on an ongoing basis. While Spotify’s LTM gross margins of 26.8% are low in absolute terms relative to most technology businesses (e.g., software businesses), gross margins have expanded significantly from the 13-15% range in 2016 and trended higher since Q1 2018.

However, gross margins differ considerably as a function of revenue source. Premium subscribers have a gross margin of around 29%, while ad-supported users have a gross margin of around 11%. As a result, premium subscribers account for 87% of total revenue, but 95% of total gross profit. Revenue growth from ad-supported users (75% year-over-year growth in Q3 2021) is outpacing revenue growth from premium subscriptions (22% year-over-year growth in Q3 2021), and this trend has persisted since Q1 2018. It is impressive that Spotify has continued to expand overall gross margins from Q1 2018 even as ad-supported revenues have grown to represent a larger component of Spotify’s revenue base.

While accelerated growth in ad-supported revenue acts as a short-term headwind to gross margin expansion, it is important to note that all content costs related to podcast investments are classified in the ad-supported business, contributing to the differential gross margins between the premium and ad-supported business. Spotify is still in the very early stages of building out their podcast content database and monetizing their free user base, so it is unsurprising that podcast advertising revenue is not currently accretive to gross margins. Over time, Spotify management believe that ad-supported podcast revenues will become accretive to gross margins, as Spotify does not need to pay out royalties and fees in the same way it does with record labels.

“Right now, despite the significant growth [in ad-supported revenue], it is still a drag on margins. Over time, I think our belief is that if you think about where our gross margins are now, that the podcast business should have higher gross margins.” (Paul Aaron Vogel, Spotify CFO)

Additional medium-term drivers for gross margin expansion include growth in high-margin auxiliary services, such as paid podcast subscriptions and artist recommendations. Moreover, if Spotify expands into additional audio verticals (e.g., audiobooks and/or meditations apps), it opens up additional monetization opportunities amongst their enormous network of 381m MAUs.

Spotify management have forecast medium-term gross margins of 30-35% and I see no reason to doubt this forecast based on their track record of execution so far and future monetization opportunities.

10) Consistent positive free cash flow margins

While Spotify has only recently become profitable on a GAAP basis, they have reported positive free cash flow margins consistently since Q1 2018 (Q1 2020 being the lone exception). Spotify has an enormous runway for growth over the coming decade, so I do not want to see them pull back on product and marketing investments to maximise free cash flow in the short-term. I would prefer to see Spotify make the necessary investments to further build the stickiness of their ‘super-app’ ecosystem and retain subscribers (demand side) and high-performing content creators (supply side). Nonetheless, it is still pleasing that in the current climate where Mr Market’s enthusiasm for unprofitable growth companies appears to be waning, Spotify is not dependent on the capital markets to fuel further growth.

11) Led by a visionary founder with skin in the game

Spotify is a founder-led business with Daniel Ek at the helm as CEO. As he makes few public appearances, I made a concerted effort to listen to all of his podcast appearances and interviews in doing research for this article. Daniel appears a humble, thoughtful, and principled leader with clear long-term ambitions for Spotify. I highly recommend listening to his two appearances on the ‘Invest Like The Best’ podcast (see here and here) for more insight into his worldview and grand mission for Spotify to empower creators all across the globe.

As one would expect from a long-term founder, Daniel is Spotify’s largest shareholder with an almost 10% ownership stake, placing his net worth in the multi-billions. Investing in innovative companies with strong competitive advantages that are led by founders with skin in the game is a combination I like to see and Spotify fits this mould.

– The Blog of Author Tim Ferriss")

12) A very reasonable valuation for the growth potential

As of 17th January 2022, Spotify trades on a very reasonable forward EV/sales multiple of 3.0x and 11-12x forward gross profit if we assume no notable gross margin expansion in 2022. Given that 87% of Spotify’s revenue is subscription in nature with single-digit churn rates, this valuation multiple seems low for a high-quality business with a strong competitive position in a large, global (and growing) market. Spotify has not strung together enough consecutive quarters of GAAP net income to warrant a helpful discussion of P/E multiples, but as mentioned earlier, I expect Spotify to become highly profitable in the coming years as gross margins expand to the 30-35% range.

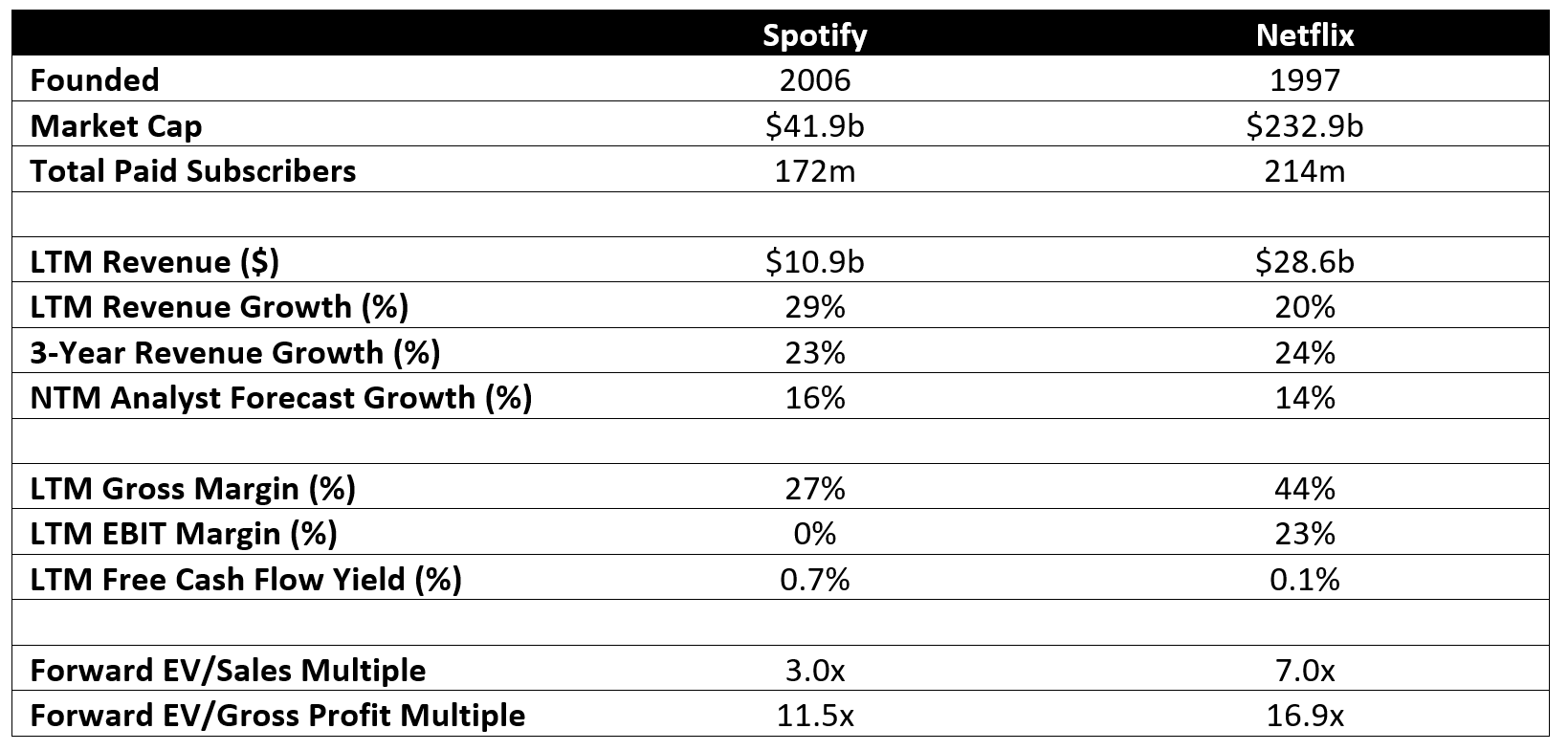

As Spotify’s direct competitors in the audio streaming market (Apple, Amazon, Alphabet) have multiple business lines of which audio streaming is just a small part, Spotify’s main valuation comparable is Netflix. When we compare Spotify’s valuation with Netflix, it is clear that Mr Market is placing a healthy valuation premium on Netflix, which makes sense given their higher gross margins and EBIT margins. However, Spotify outpaces Netflix in terms of both LTM and NTM revenue growth, and has a higher free cash flow yield. But here is the most striking comparison: Spotify has 80% of Netflix’s paid subscriber count, but only 18% of the market cap, indicative of the clear under-monetization of music streaming relative to other forms of digital entertainment, like TV streaming.

Thus, Spotify’s current valuation appears reasonable both on a historical basis relative to previous multiples since IPO and in comparison to Netflix, which is their most direct valuation comparison. If Spotify is able to continue to unlock new monetization opportunities and expand gross margins to the 30-35% range, the valuation differential with Netflix should narrow and I would not be surprised to see Spotify trade on 4-5x forward sales.

Spotify management agree that shares are undervalued at the current price, announcing a plan to repurchase up to €1.0b of shares in August 2021. At the end of Q3 2021, Spotify had purchased €30m worth of shares at an average cost of $223 per share, above the current share price of $218.56.

Web 3.0: Existential risk (or opportunity!?)

The rise of the ‘Web 3.0 economy’ poses an existential threat to all legacy media and content platforms, including both Spotify and Netflix. In a world where artists are able to directly monetize relationships with their fans through the use of tokens, Spotify’s role as an intermediary between creator and audience becomes less influential. However, I believe Spotify is well positioned to deal with the threat of Web 3.0 (a low-probability, high-consequence outcome) for the following reasons:

Disintermediation from large platforms might be possible for well-known creators with large audiences, but is less feasible for newer artists who use platforms with excellent distribution like Spotify or YouTube to market their work on a global stage. Even in a ‘Web 3.0 economy’, Spotify offers a valuable role in helping aspiring artists and podcasters to build an audience.

Daniel Ek is an innovative and forward-looking CEO who is well aware of the threat of Web 3.0 and is actively working to get ahead of potential disruption. For example, Spotify’s ‘Open Access Platform’ allows creators to deliver paid content to their existing subscriber base, for free. While there are potential short-term monetization opportunities here for the taking, I believe this is a brilliant long-term strategic move as it helps ensure that top artists remain committed to using Spotify, further enhancing their market leadership position. This move also differentiates Spotify from Apple Music who prevents artists from forming direct relationships with fans and monetizing that audience on Apple apps.

Conclusion

Terry Smith is a famous ‘growth investor’ from the UK who manages more than €28.9b for the Fundsmith Equity Fund. He runs a concentrated portfolio of 20-30 positions and has a stellar track record, generating 18.6% compounded returns since inception. He boils good investing down to three main things:

Buy good companies.

Don’t overpay.

Do nothing.

I refer to this checklist when I find myself overthinking an investment. With Spotify, I am almost certain I am investing in a “good company” providing a valuable service in the global audio streaming market. The valuation appears reasonable based on historic ranges and is attractively priced in relation to their most direct valuation comparable, Netflix. It seems unlikely that a business of Spotify’s quality would trade for long at a single-digit multiple of forward gross profits. And we haven’t even begun to talk about opportunities for expansion in developing markets …

Based on the above thesis, I feel confident initiating a starter position in Spotify around the current share price of $218.56. Now comes the third and hardest part: “do nothing”.

Another great read Jordan