Talkspace's Earnings Power is About to Become Obvious

I think Talkspace offers a compelling risk/reward, with potential for a 30%+ IRR over the next 3 years.

Talkspace is the largest in-network telehealth mental health provider in the US, benefiting from strong demand and a scalable, flexible clinician model.

The strategic shift to a payor model has driven rapid revenue growth, improved profitability, and created a more attractive, affordable consumer offering.

Financials are robust: 15%+ revenue growth, strong operating leverage, GAAP profitability, a fortress balance sheet, and active share buybacks support the investment case.

Talkspace offers a compelling risk/reward, with potential for a 30% IRR over the next 3 years.

Thesis summary

Talkspace (NASDAQ:TALK) is the largest in-network provider of virtual mental health services in the US, with almost 200m covered lives across major health insurers, employers, and EAP partnerships. On the Talkspace platform, users can access therapy via 1) real-time video or phone calls or 2) asynchronous text message conversations, where Talkspace pioneered much of the early research on the efficacy of this therapy modality. Talkspace has over 5,000 trained clinicians on the platform.

Talkspace has had a torrid time in the public markets since listing via SPAC in 2021 at a $1.4b valuation. Shares dropped more than 90% in 2022 from their 2021 high due to a combination of general investor pessimism around SPACs and telehealth companies, as well as concerns over the viability of Talkspace's D2C business model in the face of continued cash burn. Like many SPACs from the 2021 vintage, Talkspace quickly became discarded as a 'broken SPAC' and, for a short period of time, traded for less than their net cash (i.e., negative enterprise value).

In 2022, the Co-Founders were replaced by an experienced healthcare CEO (Dr. Jon Cohen), who doubled down on the shift from a D2C to B2B2C (payor-first) model. Since this point, Talkspace has quietly evolved into a capital-light, profitable business with defensible revenue streams.

While sentiment for Talkspace has improved somewhat (shares are up over 4-fold from their lows in late 2022), I believe the market still fundamentally under-appreciates the earnings power over the new B2B2C model, particularly over the next 12-18 months.

As I discuss later in this article, while the company may appear optically expensive at a 142x trailing P/E ratio, even under conservative assumptions, the 12-month forward P/E ratio could be as low as 21x. If this situation unfolds as I expect, the earnings power of the business will become obvious to all public market investors, and shares should re-rate to a much higher multiple, providing an attractive combination of earnings growth and multiple expansion.

Qualitative investment highlights

Structural demand for mental health services

Prior to a career in venture capital, I trained as a clinical psychologist in Australia and have experienced first-hand the rise in both prevalence and severity of mental health concerns amongst both adolescents and adults.

There is no doubt that the US (and the developed world) is in a mental health crisis. Recent estimates suggest that 23% of US adults live with a mental illness and 36% of young adults aged 18-25 live with a mental illness. These numbers have risen sharply when assessed over any longitudinal period.

With reducing mental health stigma and increasing acceptance of virtual care as a therapeutic channel, demand for mental health services is quickly rising. In short, mental health services are in high demand (and outstripping growth in supply of clinicians), and Talkspace is well-positioned to service this continued demand as the market leader in the US (as measured by in-network provider coverage).

Win-win-win model for all stakeholders

I look to invest in companies that benefit all stakeholders, as this is generally a core ingredient for sustainable long-term growth. Companies that strongly prioritise one stakeholder over another might see strong earnings growth in the short term but are more exposed to long-term risks (e.g., customer boycotts, competitor retaliation, lawsuits, regulator enquiries, etc.).

Talkspace has an offering that benefits all stakeholders in its ecosystem, providing a foundation for long-term growth:

Consumers: Can access mental health treatment in a modality of their choice (phone call, video call, text message) from the comfort of their own home without needing to travel, take time off work, or organise childcare. High consumer satisfaction is evidenced by strong online reviews (4.4/5 on Trustpilot, 4.8/5 on App Store, 4.6/5 on Google Play Store).

Clinicians: Can work flexibly at a time of their choosing and save time and cost on transportation (many of Talkspace's clinicians are mothers who work part-time due to childcare responsibilities; traditional in-person clinic employment models are often too rigid to accommodate such clinicians).

Customers (private payors, employers, EAP providers): Dollars spent on mental health services for staff produce a high ROI due to lower absenteeism, better staff wellbeing, and higher staff retention

Successful business model transition (D2C to B2B2C)

In Q3 2021, 71% of Talkspace's revenue came from its D2C segment, where consumers pay out-of-pocket for a subscription to access Talkspace.

Fast forward to Q1 2025 (only 3.5 years later), and only 9% of Talkspace's revenue came from their D2C segment vs. 73% for private payors and 18% for employer partnerships (direct to enterprise).

This revenue composition puts Talkspace in stark contrast with another public competitor – BetterHelp, which is owned by Teladoc Health (TDOC) – that is the largest D2C virtual mental health care platform in the US (over $1b annual revenue). With consumers experiencing cost of living pressures and more competition from players like Talkspace with extensive in-network coverage, BetterHelp is seeing softening consumer demand—revenue was down 8% in 2024 and down 11% YoY in Q1 2025.

I much prefer Talkspace's B2B2C (private payor) and B2B models. Unit economics are much stronger (despite lower gross margins), and the consumer proposition is much more attractive than comparable B2C subscription offerings. More than 50% of Talkspace customers have no co-pay, and the average co-pay per session (if not fully covered by a private health plan) is only $15, so even lower-income consumers can afford therapy. In contrast, BetterHelp's cheapest consumer plan starts at $70/week.

Overall, this shift from a B2C to B2B2C and B2B model has greatly improved both the predictability and defensibility of Talkspace's business. While larger competitors are reporting revenue declines, Talkspace grew revenues by 15% in Q1 2025, and their private payor segment grew 33% YoY.

Well-positioned for high-risk populations

Talkspace has been very adept at understanding the needs of high-risk populations (e.g., adolescents, military veterans, sailors) and signing large-scale partnerships to serve those populations. Some examples include:

November 2023: Talkspace signed a $26m contract with the NYC Department of Health and Mental Hygiene to provide virtual mental health services to over 400,000 NY-based adolescents aged between 13 and 17 years.

December 2024: Talkspace signed a partnership with Seattle Public Schools to provide mental health services to anyone aged 13-24 years.

January 2025: Talkspace announced they are now available to 9.5m active duty and retired military personnel (and dependents) through partnerships with TRICARE East and West region contractors.

March 2025: Talkspace announced a trial program with the US Navy to provide therapy and resources for 25,000 sailors and their dependents.

These partnerships provide predictable revenue streams and enable Talkspace to gain a foothold in populations linked with high rates of mental illness. I am most excited about the partnerships with school networks – adolescents who have a positive experience with Talkspace could develop lifelong brand affinity with Talkspace, returning as adults for either preventative or more acute care.

While other competitors focus exclusively on adults (a competitive market), building strong traction within adolescents could be a material differentiator for Talkspace.

Solid growth, profitable, exceptional operating leverage

When Talkspace was in the messy middle of their transition from a D2C to B2B2C/B2B model, it was hard to fully comprehend the quality and earnings power of their business model. With the transition now largely complete (more than 90% of Q1 2025 revenue came from private payors or employer partnerships), the financial picture is much more straightforward to assess.

Revenue trends

In Q1, Talkspace generated $52.2m revenue ($209m annualised), up 15% YoY. Management remains confident in their 2025 guidance for 17-25% revenue growth, driven by the benefits of higher marketing spend in Q1 and continued B2B2C penetration.

The private payor segment is the standout performer, with YoY revenue growth of 33% for the past 2 quarters. As this segment rises from 73% of revenue (Q1 2025) to the 80-90% range in the coming quarters, we should see total revenue growth begin to more closely approximate growth in the payor segment.

Exceptional operating leverage

The most impressive part of Talkspace's turnaround has been its exceptional operating leverage.

While revenue increased 56% from Q1 2023 to Q1 2025, operating expenses actually decreased 6% over this same period. As the chart below shows, general and administrative (G&A), sales and marketing (S&M), and clinical operation costs remained flat over this period, while R&D has come down.

S&M also declined from 40% of revenue to 27% of revenue over this period, indicating that S&M efficiency is much better for their B2B2C acquisition channel than their old B2C model.

With this disciplined cost control and better unit economics on the B2B2C model, Talkspace has improved from a -26% net profit margin in Q1 2023 to being GAAP profitable for the past 3 quarters.

For keen readers, it is worth noting that net income is slightly higher than EBIT and EBITDA margins due to interest received on their high cash balance.

While net income in absolute dollars remains very low (only $0.3m in Q1 2025), there is the potential for explosive profitability in the coming quarters.

As an example, if we assume Talkspace grows revenues by 20% over the next 12 months, they will be generating $233.2m in trailing 12-month (TTM) revenue. Given the cost base has actually declined in recent quarters while Talkspace has continued to grow revenues by 15%+, the incremental net profit margin is very high. If we assume a 50% incremental net profit margin over the next 12 months (this implies that half of the 20% revenue growth falls through to the bottom line), Talkspace will be generating $19.4m of TTM net profit in Q1 2026, equating to an 8.3% net income margin.

At this point, the earnings power of the business should be well understood by the market.

Clean, capital-efficient operating model

Talkspace has a clean and capital-efficient operating model. EBIT, EBITDA, and net income margins closely track each other as there is little need for CapEx or capitalised software development to sustain growth.

Moreover, stock-based compensation is reasonable (<5% of revenue for the past 3 quarters) and has trended down over time.

Fortress balance sheet

Talkspace's balance sheet is very strong. As of Q1 2025, the business had $108m of cash, equivalents, and marketable securities with no debt.

As Talkspace is now profitable and has such a strong balance sheet, management has been able to initiate a share buyback program, which is a big tick in my book. In 2024, Talkspace repurchased $11m shares and repurchased more than $7m shares alone in Q1 2025 ($28m annualised).

At the current valuation, share buybacks make a lot of sense and are a wise capital allocation decision.

30%+ IRR is possible at the current valuation

As of 17 July 2025, Talkspace has a $416m market cap and an enterprise value (EV) of $308m (net cash = $108m). The business trades at an EV/TTM revenue multiple of 1.6x.

While not the absurdly cheap revenue multiple of 2022 (net cash was greater than Talkspace's market cap, so the business had a negative EV revenue multiple for the period), a 1.6x EV/TTM revenue multiple is not demanding for a business expecting to grow 17-25% in 2025.

So, why is the business cheap? I believe there are a few reasons:

Talkspace has been incorrectly discarded by many investors as a 'failed SPAC'.

The market cap of $416m is too small for most sophisticated investors and sell-side analysts to cover the stock.

The business looks optically expensive with a TTM P/E ratio of 142x.

While the TTM P/E ratio is very high, Talkspace has only recently crossed the cusp of profitability, so P/E ratios are almost worthless. However, many investors using stock screens or relying on simplistic earnings multiples may discard Talkspace without appreciating the earnings power of the business over the coming 1-2 years.

Like my earlier analysis demonstrated, Talkspace can easily be generating 8% TTM net profit margins by Q1 2026. At the current market cap, this implies a 21x forward P/E multiple, which is below the median US public company, despite growing many multiples faster than the median company.

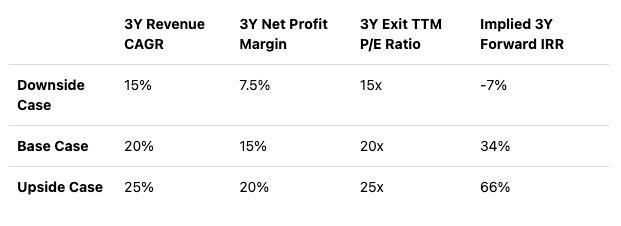

If we do some simple valuation modelling, Talkspace has the potential to generate a 30%+ IRR from current levels over the next 3 years. In my base case scenarios (34% expected IRR), I assume Talkspace:

Grows revenues by a 20% CAGR through to Q1 2028.

Achieves a 15% TTM net profit margin (as a reminder, my conservative numbers have them at an 8% net profit margin by Q1 2026).

Trades at a TTM P/E ratio of 20x (below the median US company).

As part of this modelling, I have not factored in any share buybacks or dividends, which would further improve returns.

Risks

An investment in Talkspace is not without risks.

This is a competitive and fragmented industry, which could mean Talkspace's S&M costs need to increase materially from recent levels to defend against well-funded competitors in the private markets (e.g., Lyra Health, Modern Health, Spring Health). My hypothesis is that private payors and large employers will gravitate towards the company with the highest brand recognition and credibility, which should benefit Talkspace, who has the largest in-network coverage, a public profile due to their NASDAQ listing, and is subject to stringent regulatory oversight as a listed company. Nonetheless, I will be closely watching the competitive environment.

Talkspace is also not a founder-led business, which is a deviation from my normal investment strategy. However, Dr. Jon Cohen appears to be a highly qualified and experienced healthcare leader who has executed very well so far in Talkspace's turnaround. Jon is a vascular surgeon by training who also served in a number of senior executive roles in the healthcare sector – he was CEO of BioReference Laboratories (one of the largest commercial pathology testing providers in the US) and was Chief Medical Officer of the largest healthcare system in New York (Northwell Health). I've listened to every interview available online with Jon and have high confidence in his ability to continue to drive sustained growth and profitability at Talkspace.

Talkspace is also a relatively small company ($209m TTM revenue) and has a transaction fee-for-service model with private payors. As such, results could be lumpy, and the loss of a large health plan or employer partnership could have a material impact on the overall business.

Summary

Talkspace is a classic under-appreciated asset that has been discarded by many investors as a 'broken SPAC', presenting an opportunity for diligent investors willing to dig beneath the headline numbers.

Talkspace is a market leader operating in a very large industry with clear structural tailwinds driving continued demand for mental health services. The shift to a B2B2C model has been highly successful, with consistent 15%+ revenue growth rates and exceptional operating leverage. While some investors may discard Talkspace due to the optically high TTM P/E ratio (142x), investors should focus more on the 21x forward P/E ratio as a fairer multiple for the business.

At the current valuation, I believe a 30% IRR over the next 3 years is highly achievable, a rarity in the current market where most technology stocks are priced for perfection.

I recently purchased shares in Talkspace and will continue doing so if the market continues to under-appreciate the quality and earnings power of their business model.