My Favourite Media Content - July 2023

A glimpse into the best podcasts, articles, videos, and books I consumed in July 2023.

To return the favour, please send me your favourite podcasts, articles, videos, or books from this month.

Stock recommendations also welcome (maybe I can even return the favour!). My email address is: jordan.martenstyn12@gmail.com.

Podcasts

1) We are introduced to Rentvesting (Equity Mates)

This was a fascinating podcast about rentvesting (explained below). I generally find that most podcast interviews with “property people” (you know the ones) are very biased and full of unsubstantiated cliches about the moral imperative to own a home (e.g., property always goes up, the best time to buy a house is now, etc). In contrast, this podcast was surprisingly insightful and balanced. Here were my main takeaways:

Rentvesting involves renting where you live (ideally in a desirable location) and owning an investment property in a cheaper area that fits within your budget (and ideally provides a high rental yield). This strategy allows you to also invest the difference saved vs. having a mortgage on a primary residence. For example, if it costs you $900/week to rent in Surry Hills but a mortgage in that same area costs $1,700/week, you would invest the $800/week difference in an investment property or other investments (note: these are actual numbers I went through recently).

He thinks the cost of housing in Sydney is unjustifiably high (as has been re-iterated by many other smart people like Matt Barrie and Chris Joye) and personally rentvests in Sydney, despite having a property portfolio of $24m!

You can borrow more when rentvesting because the future rental income from an investment property gets added to your income and thus increases your borrowing capacity. However, this needs to be weighed against the potentially higher interest rate for an investment property loan vs. owner-occupier loan.

Interest payments on an investment property (but not an owner-occupier home) are tax deductible, so there are tax advantages to consider with rentvesting.

His buyers agency looks for markets at the bottom of major re-rating cycles with 1) low vacancy rates and 2) solid infrastructure projects in the pipeline. He is currently actively looking around Brisbane, Adelaide and Perth (i.e., basically everywhere but Sydney and Melbourne).

He has a preference for “manufactured investments” to boost rental yield on investment properties (e.g., buying a single home and then adding a granny flat in the backyard to be able to get two sources of rental income from the single title). This increases the rental yield because rental income increases while the mortgage payment, council rate, and land tax remains the same (nice operating leverage).

He finds the best deals generally come off-market (i.e., not at auction). Over 90% of his transactions as a buyers agent come from off-market purchases.

2) Lightning in a Bottle and Microcap Investing with Ian Cassel (The Investor’s Podcast)

This was a super interesting podcast with a highly concentrated private investor who focuses on public small caps and microcaps. My main learnings:

During the GFC, Ian only had 3 stocks in his whole portfolio.

He looks for small caps that are 1) profitable, 2) have high organic growth rates, and 3) have less than 20m shares outstanding (so the share register is tightly held which can lead to price squeezes when there is a large influx of buyer demand).

As less small companies are going public (due to higher listing costs, increased regulatory scrutiny, and more access to funding in private markets), good opportunities are decreasing in the US. As a result, good microcap investors have turned to other geographies like Canada, Australia, and emerging markets.

Rather than generic quantitative screens which everyone uses to find potential investments (e.g., >20% growth, >70% gross margin, profitable, etc), he looks for large recent insider buying from management to identify interesting opportunities.

A simple screen to check for past management misconduct is to google the names of each member of senior management and then “fraud”. He’s even hired a private investigator in the past to delve into the background of senior management for prospective investments.

It’s very tough to be a “buy and hold” investor in small caps and microcaps. You need to constantly complete “maintenance due diligence” post-investment, involving chatting with former employees, suppliers, customers, etc. As a result, the holding period tends to be much shorter for small caps/microcaps than larger and more stable businesses.

He is finding the healthcare industry (likely healthcare IT software) very attractive and currently has 50% of his portfolio invested in that sector.

3) Value Investing: Down But Not Out? With David Einhorn (Money Maze Podcast)

It’s rare to find public interviews with David Einhorn, a prolific value investor who manages Greenlight Capital and is probably best known for his public shorts on Enron (successful) and Tesla (not so successful). He had some contrarian takes on the current structure of markets:

David has changed his approach to value investing to cope with the new market structure. In the past, he focused on finding cheap companies that people thought were going to have very bad outcomes (e.g., earnings to decline 20% in a year) that in fact turned out to only be slightly bad (e.g., earnings to decline 5% in a year). When the market realised that the company’s results were not going to be as bad as initially feared, big pension funds and other long-only investors would bid up the stock, which is when David would sell for a quick profit.

From David’s perspective, those kinds of value-conscious investors no longer have the power and capital to move markets (i.e., there is no eventual buyer who will see the value and bid up the stock). They have been replaced by passive funds (e.g., ETFs) and other quantitative-driven traders that are not trading on value, but rather volatility, momentum, and market correlations.

There is now a “wasteland of companies” that get almost no interest from sell-side analysts or funds, and are not big enough to be included in major indices, so they essentially have no demand from buyers.

Buying these forgotten companies on very cheap multiples (e.g., 4-6x P/E) with little debt that constantly return their excess earnings and cash flow to shareholders “has to mathematically work”. For example, if a company is buying back 15% of its shares outstanding each year with excess cash flow, there’ll be no shares left in a few years to buy unless the price goes up. These are the kinds of investments David is focused on right now.

Astute private equity buyers are becoming the last buyers of these forgotten and very cheap companies. They are buying at massive premiums to the last share price (e.g., 100% premium) but still well below book value (the net value of all assets), so while it looks like they’re overpaying, they’re in fact getting great deals.

David has become a lot more secretive about publicly disclosing his short positions because people used to deliberately try and short squeeze companies he was known to be short (e.g., Tesla).

4) Harry Stebbings on Starting 20VC, Being Underestimated, Investing, and Wealth vs. Happiness (Invested by Aleph)

In a rare moment, Harry Stebbings (of 20VC) was the interviewee in a podcast. Some learnings:

20VC fund has about $400m FUM (much more than I thought!).

Harry started 20VC podcast while he was still in high school. He didn’t get any money from the podcast until episode 125, which is a big testament to grit and perseverance.

He’s a very intense guy with some pretty strong opinions about work-life balance, discipline, and weight that I don’t necessarily agree with. In this podcast, he argues that burnout is a very “first-world problem” and only occurs when we hate our job.

He’s really professionalised the business of podcasting. He thinks of all episodes as his “product” and doesn’t publish around 30% of interviews he records. He also has a dedicated speaking consultant on staff who provides feedback to each interviewee about the episode and areas to improve on (I wonder if they did that to Rishi Sunak and Bill Ackman!).

One of my favourite quotes from the interview: “the best investors are hyper-curious and hyper-competitive”.

He believes the utility of operating experience as a VC investor is becoming less and less important as the pace of innovation increases. For example, being a senior VP at Adobe or Salesforce in the early 2010s has little relevance to being an investor in the AI-dominated 2020s. I’ve never heard that take before but I tend to agree (although I might be a bit biased!).

Articles & Presentations

1) Meet Dave: The Warehouse Worker Who Retired at 28 by Keeping it Simple (Livewire Markets)

This article was a great reminder that: 1) good investing is often radically simple (bordering on boring) and 2) dollar-cost averaging into a broad basket of ETFs provides, for most people, the most reliable and low-risk route to long-term wealth creation. For some context, here is Dave’s current portfolio:

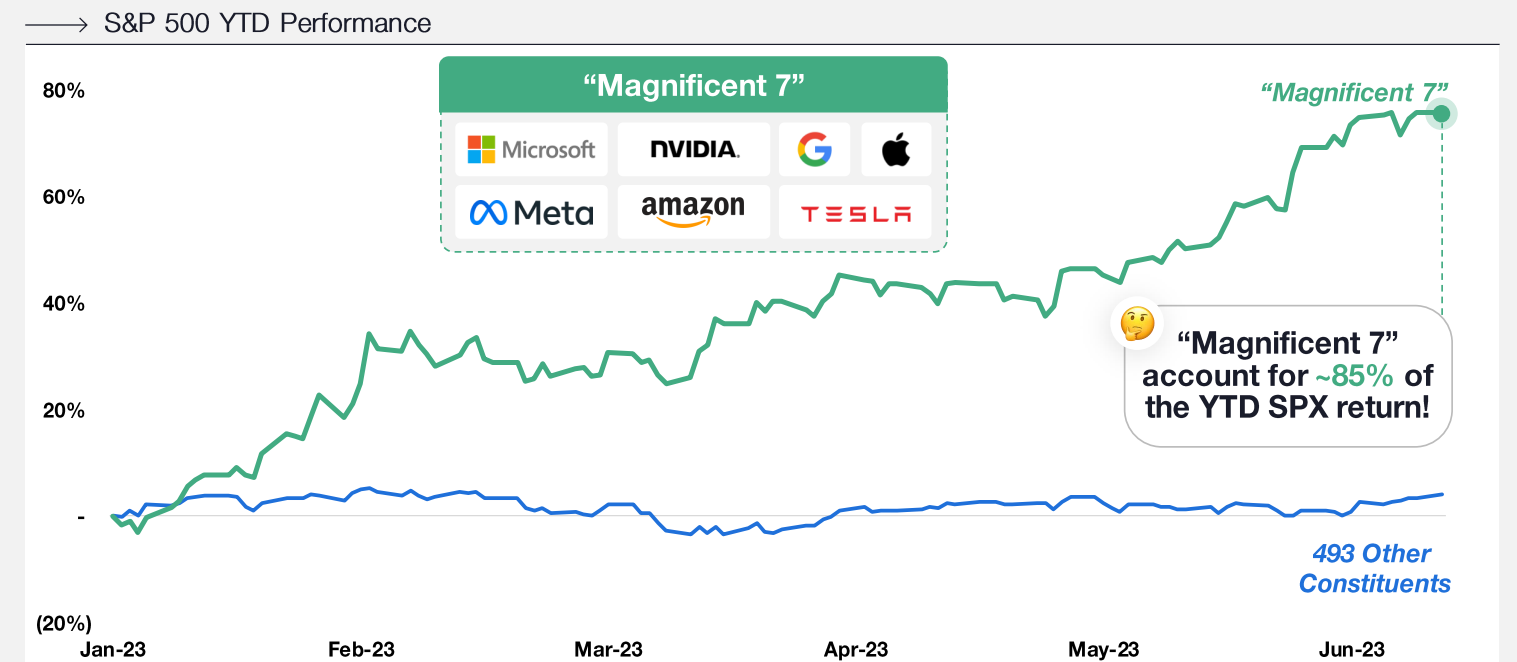

2) Coatue’s 2023 East Meets West Conference Slides

Thanks to Abhishek Maran (VC investor @ Rampersand) for bringing this presentation to my attention. This was a great summary from Coatue (one of the largest global growth investors) of the current macroeconomic landscape and the extent to which the “Magnificent 7” (Microsoft, Nvidia, Alphabet, Apple, Meta, Amazon, and Tesla) have driven index returns in 2023. Never seen so many emojis in a formal investor presentation either!

3) How Podcaster Andrew Huberman Got America to Care About Science (TIME)

A great read into the backstory of Andrew Huberman, a neuroscientist at Stanford who has risen from near obscurity a few years ago to become one of the most well-respected public intellectuals of the 2020s.

")

Books

1) The Total Money Makeover: A Proven Plan for Financial Fitness (Dave Ramsey)

This was one of the most impactful personal finance books I’ve ever read, which has redefined by approach to debt and the accumulation of wealth. Dave Ramsey’s simple 7-step framework (consisting of discrete “baby steps”) is summarised below:

In short:

Become debt free (including all personal credit card debt, student loans, and auto loans).

Save $10-25k in an emergency fund to provide peace of mind against future catastrophes (e.g., being made redundant, major health bills, being in a car crash, etc). In other words, become “antifragile” to major exogenous life shocks.

Invest 15%+ of gross income into simple ETFs or mutual funds for retirements (we have 10.5% of this already covered in Australia by superannuation).

Save a small amount each month for children’s future education costs (e.g., private school and/or university).

Aggressively save money to purchase assets (e.g., stocks or real estate) to build wealth. Like me, Dave is very conservative and recommends all investments are purchased 100% in cash (including real estate), which is quite the contrarian take for those living in expensive markets, like Sydney or Melbourne.

How has this book changed my approach to personal finances?

I’m planning to pay off my HECS debt (<$20k) in full sometime over the next month with existing savings to become debt free (excluding a small credit card balance that I pay off each month).

Move $10-15k into a separate checking account for future emergencies.

Begin saving a small amount each month for future children’s education expenses.

Rentvest and save aggressively to purchase an investment property in Western Sydney (<$600k with a rental yield exceeding 6%).

Twitter

1) Career advice for people in their 20s

A great thread on how young people in their 20s can stand out in the workforce (FYI Musk has blocked Twitter links appearing automatically on Substack …)

https://twitter.com/cblatts/status/1679953131315298304

YouTube

1) Dave Ramsey’s Real Estate Principles

Timeless principles of investing in real estate, including 1) the importance of putting down a solid deposit, 2) remember: location, location, location (i.e., buy the worst house in the best neighbourhood), and 3) the need to find a home with a solid structure and floor plan.

FYI you need to click on the video link to watch it on YouTube.

Companies I’m Researching

1) Spotify (NYSE:SPOT)

Spotify releases their Q2 results next week so expect an article from me. I’m expecting 15% revenue growth, sequential gross margin expansion, and material progress towards operating profitability.

2) Ambertech (ASX:AMO)

This came across my radar last week as an interesting (and cheap) business on the ASX. They make audio-visual products for consumers and professional clients (e.g., news studios). Some interesting metrics:

Market cap of around $22m AUD (with $2m cash).

Lots of insider buying in 2023.

Made a recent acquisition using $3m of cash reserves (love to see that vs. using debt or diluting shareholders with a capital raise).

$40.5m revenue in H1 FY23 with around $2m EBITDA.

Gross margin of 35%.

Valuation of around 5x annualised EBITDA and 0.25x annualised revenue.

Paid out around 2c in dividends over the last 12 months, representing almost a 10% yield (before franking).

Anyone done much research on this company before?

Best,

Jordan