Lemonade's Q3 2021 Results: Another Solid Quarter, But Not Enough to Silence the Bears

Lemonade's Q3 2021 Results: Another Solid Quarter, But Not Enough to Silence the Bears

In this short article, I summarise the good and bad from Lemonade's Q3 2021 results released to the market on the 8th November 2021.

Lemonade is a digital-native insurance business founded in 2015 with a big ambition to disrupt the global insurance market. In a previous long-form article, I discussed in depth the business model of Lemonade, their competitive advantages over both existing incumbents (e.g., Geico and Progressive) and newer upstarts (e.g., Hippo and Root Insurance), their financials, current valuation, and future growth levers. In this short article, I summarise the good and bad from their most recent Q3 2021 results released to the market on the 8th November 2021.

But let me first begin with a quote from Lemonade’s CEO Daniel Schreiber in their Q3 conference call which epitomises their long-term vision:

“Industries like insurance are reinvented once every few centuries. Optimizing for profitability is important, but can wait. We aim to grow fast and capture as much market share, mind share and as large a geographical footprint as possible”.

Lemonade (again) beats internal guidance for revenues and premiums

With each successive quarter, I become more and more convinced that CEO Daniel Schreiber is a shrewd operator who understands the game of Wall Street and makes a concerted effort to under-promise and over-deliver. Once again this quarter, Lemonade continued their impressive streak of beating internal guidance for revenues and premiums each quarter since IPO in 2020.

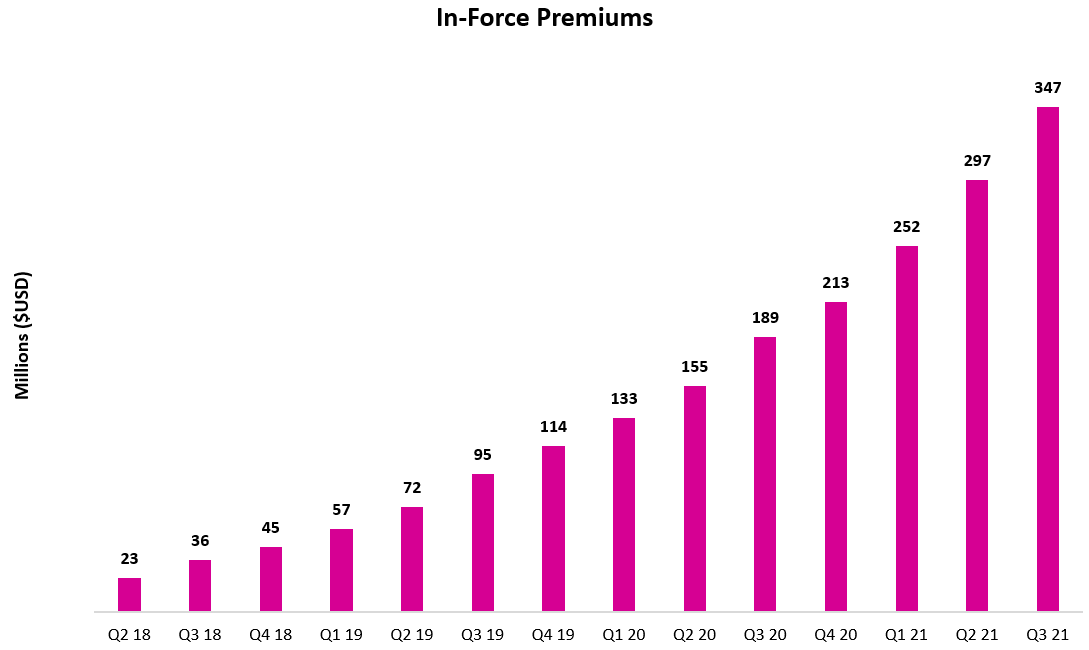

In Q3, Lemonade reported in-force premiums of (IFP) of 347m, up 17% Q/Q and 84% Y/Y, well ahead of their internal guidance of 336-339m. They also reported gross earned premium of 80m, up 19% Q/Q and 86% Y/Y, beating their internal guidance of 76.5-77.5m. IFP represents the total annualised premiums for customers at the end of a given period (kind of similar to annual contract value or ACV for a SaaS business) and is the main metric that I use to appraise Lemonade’s top-line growth. Seeing consistent quarter-over-quarter increases in IFP dating back to Q2 2018 is a pleasing sign and demonstrates excellent product-market fit.

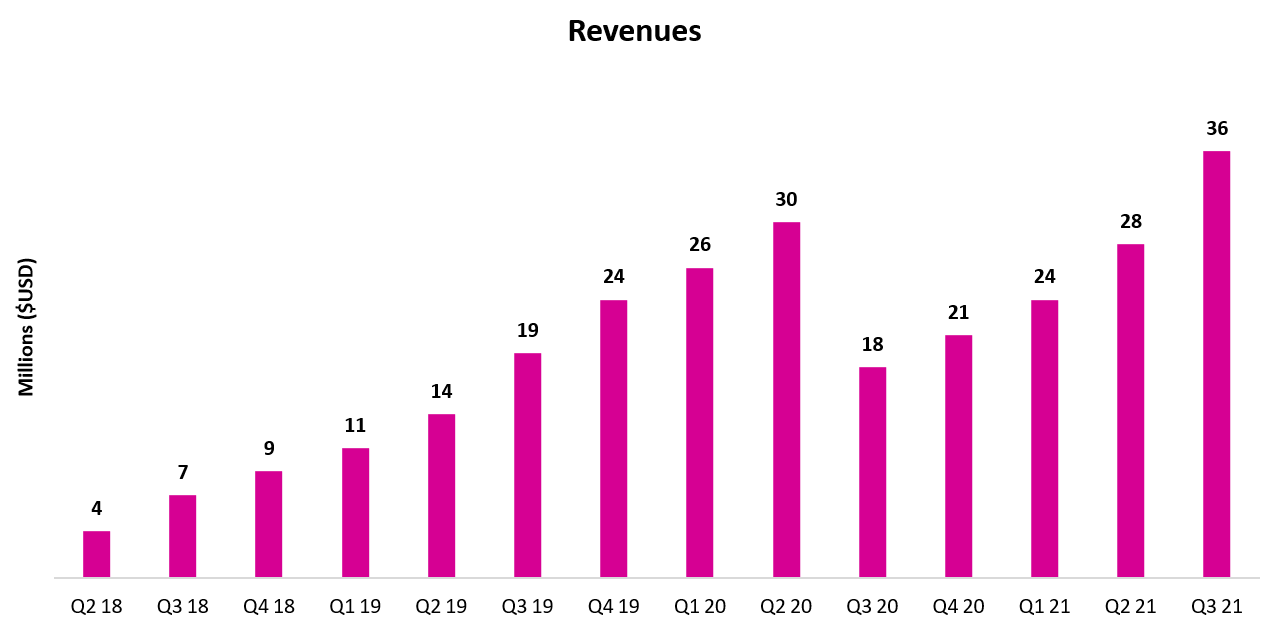

Lemonade reported 35.7m in revenue in Q3, representing impressive growth rates of 27% Q/Q and 101% Y/Y. As I explained in this article, I expect Lemonade’s revenue growth to outpace IFP growth over the next few quarters as the proportion of premiums ceded to reinsurers decreases. Recall that the period from Q3 2020 to Q2 2021 is difficult to judge in relation to prior corresponding periods as Lemonade changed their revenue recognition reporting. Without this change, we would see a similar smooth exponential curve for revenues to what we see above for IFP.

In Q3, Lemonade upgraded 2021 guidance for both gross earned premiums and revenues. Let’s take a look below at how their 2021 guidance has changed for each of their core metrics. IFP guidance has increased from 376-382m to 380-384m, gross earned premium guidance has been raised from 279-283m to 291-292m, and revenue forecasts have been upgraded from 117-120m to 126-127m. Adjusted EBITDA has not fared so well as Lemonade has downgraded guidance due to reduced marketing efficiency and increased investments into Lemonade Car insurance, which were initially planned for 2022. So, in a sense, widening adjusted EBITDA losses are due to pulling forward some expenses that were planned for 2022 into late 2021.

Lemonade added more customers in Q3 2021 than ever before … and these customers continue to spend more

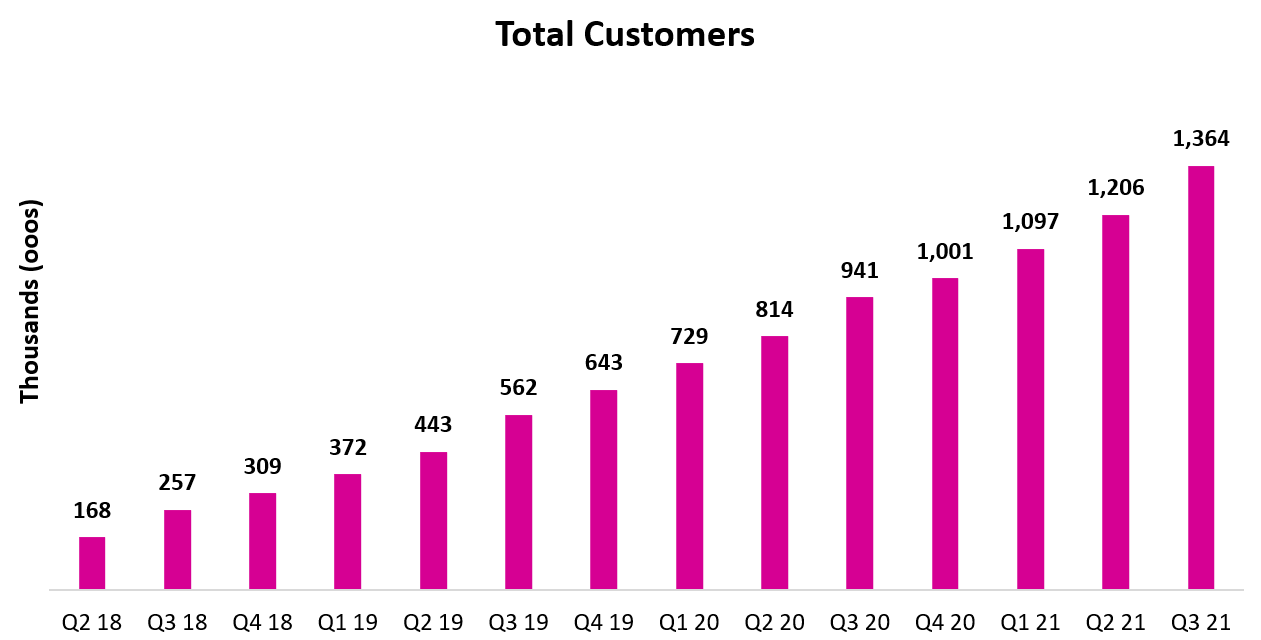

Lemonade added more than 150,000 net customers in Q3, which is their largest absolute growth in customers since inception. In relative terms, total customers increased 13% Q/Q and 45% Y/Y to 1.36m. Management explained that a large proportion of these new customers were signing up for renters insurance, which is Lemonade’s lowest margin product. Nonetheless, renters insurance serves as a stepping stone to higher margin insurance products, like homeowners or pet insurance.

One exciting statistic from the Q3 earnings report was that bundles (customers with two or more Lemonade products) now represent 8% of IFP, up from 0% in Q3 2020. During this same period, the number of customers with multiple policies increased more than 300%. Continued product bundling is a core element of my thesis for Lemonade because it acts as their main route to increasing customer lifetime value (LTV) and improving unit economics.

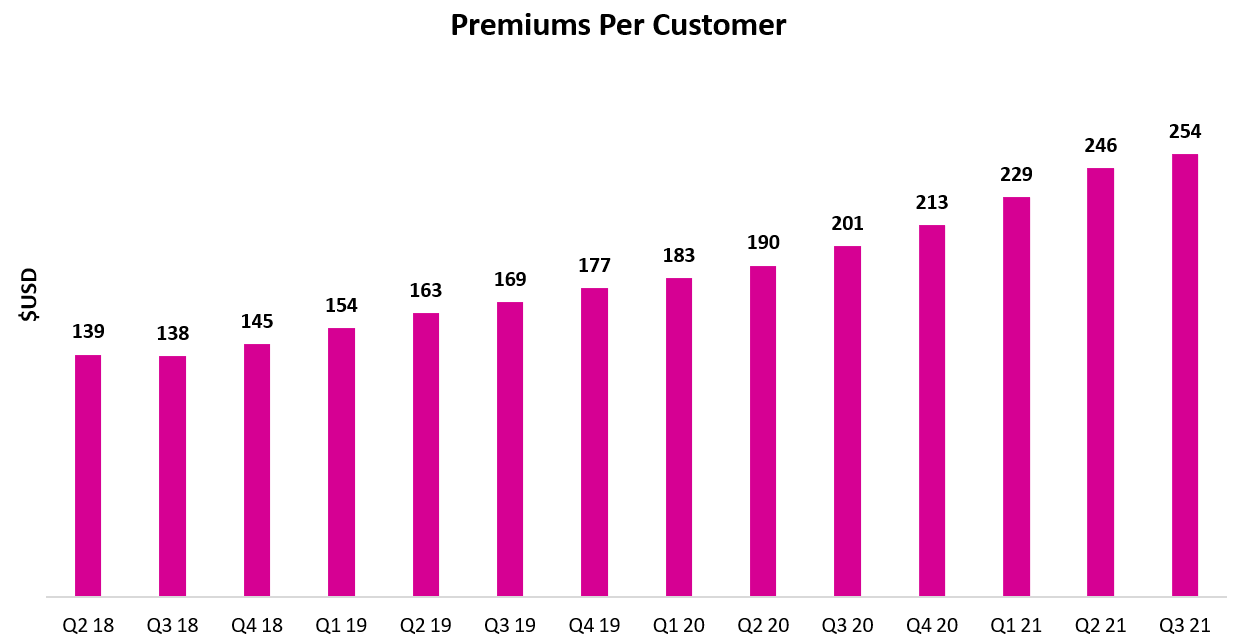

Average annual premiums per customer grew to $254 (+3% Q/Q; +26% Y/Y), which was a solid but not remarkable result and reflects the surge in new customers who signed up during the quarter for renters insurance. I expect this growth to accelerate in future quarters as rates of bundling increase. CEO Daniel Schreiber reported on the earnings call that customers who bundle multiple products together have average premiums up to 3x this amount, equivalent to almost $800 in annual premiums per bundled customer.

Continued product diversification reduces exposure to catastrophic tail events

With each successive quarter, Lemonade’s book of business becomes more diversified across product lines, reducing their exposure to catastrophic tail events (e.g., natural disasters) and helping them reduce their proportion of premiums ceded to reinsurers. The share of total IFP coming from non-renters insurance increased from 44% (Q2 2021) to 47% (Q3 2021), with pet insurance growing from 13% to 15% of IFP.

It is clear that Lemonade’s term life insurance product does not have the same degree of product-market fit as their other products. Consistent with their data-driven approach, Lemonade will be temporarily reallocating sales and marketing dollars from their term life product to expanding their business operations throughout Europe based on improving loss ratios. This move makes sense to me; around 70% of Lemonade’s customers are under the age of 35 so term life insurance is less of a concern at that life stage (I’m 23 and have never once spoken about, or even thought of, purchasing term life insurance). It will be interesting to see over the next few quarters whether Lemonade is able to gain significant traction in European markets.

Watch Lemonade’s loss ratios

Lemonade’s gross loss ratio increased in Q3 2021 to 77% (up from 74% in Q2 2021 and 72% in Q3 2020), which is not what we want to see from an insurance business. Lemonade attributed this spike to growing IFP contributions from newer products (e.g., homeowners and pet insurance) which are less mature with higher loss ratios than their more established renters insurance product.

However, management reported that these newer product lines are showing improving (i.e., decreasing) loss ratios, but that because their loss ratios are higher than that of renters insurance, Lemonade’s total loss ratios appear worse as these newer product lines became a larger share of Lemonade’s book of business. Management again reiterated their expectations for all Lemonade products to have loss ratios below 75% in the long-term.

Net losses are enormous … but manageable with Lemonade’s fortress balance sheet

One of the main concerns put forth by Lemonade bears is their astronomically high GAAP losses. While early-stage companies operating in hyper-growth mode generally have large losses, there is an implicit expectation amongst investors that these losses will narrow over time as the business demonstrates operating leverage. A lack of profits means a business is dependent on external capital to survive.

Founded in 2015, Lemonade is still investing heavily for growth and is not focused on producing GAAP accounting profits. In Q3, Lemonade reported a whopping net loss of 66.4m on 35.7m of revenue, which was up from a net loss of 55.6m in Q2 2021 and a net loss of 30.9m in Q3 2020. Most of the net loss in Q3 2021 was a consequence of increased sales and marketing spend, which Lemonade management rationalised based on increasing LTV metrics. If unit economics are indeed improving, then this increased sales and marketing spend makes sense, as for each dollar invested, Lemonade should generate multiples of that invested dollar over the coming decade. However, Lemonade does not disclose their unit economics in granular detail, so we are forced to place our trust in management. CEO Daniel Schreiber did note in the conference call that “all our products, all our campaigns, all our geographies have positive LTV to CAC” which is reassuring.

Lemonade still has around 1.1b in cash on their balance sheet, so there is a sufficient cash reserve to see them sustain these losses for another few quarters. Nonetheless, I expect these losses to narrow from 2023 onwards.

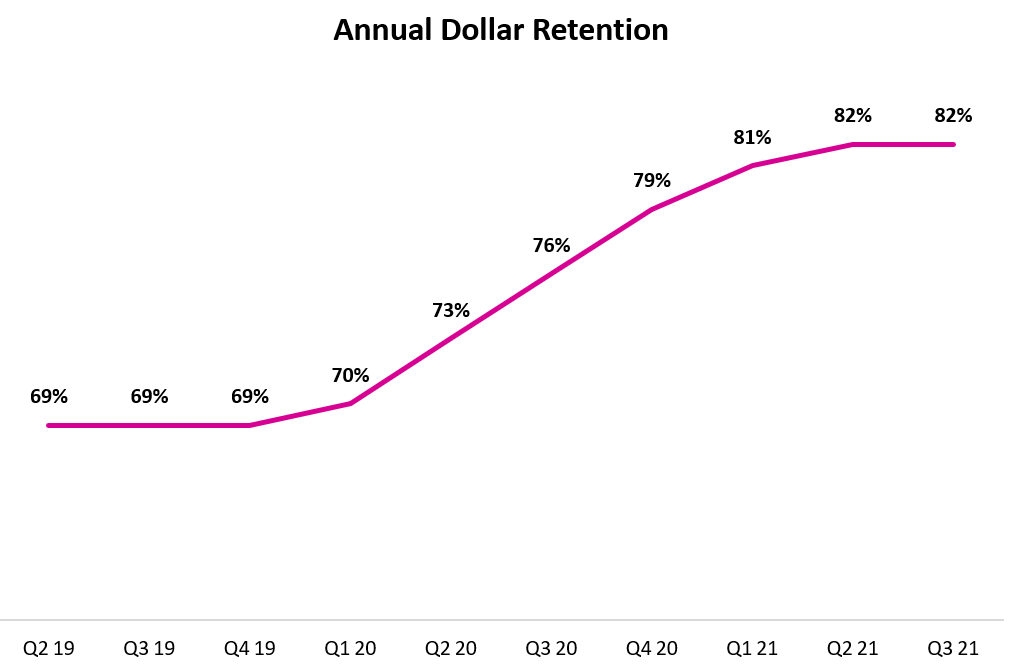

Has annual dollar retention rate plateaued?

Lemonade reported an annual dollar retention (ADR) of 82% in Q3 2021, unchanged from Q2 2021 and up around 600 basis points from 76% in Q3 2020. Lemonade defines their ADR as the percentage of IFP that it retains over a 12-month period. While this number is lower than I would have expected given their rave customer reviews, it is consistent with the averages for established insurance businesses across developed economies. However, a big element of my thesis for Lemonade is the belief that their product offering is superior to incumbents (based on greater UX, increased convenience, faster processing times through automation, etc), so this should manifest through to above-average ADR at some stage in the future. If this number continued to plateau over the coming quarters, it would be a cause for concern.

Lemonade launches car insurance … but the acquisition of Metromile raises more questions than answers

Consistent with their expectations communicated to the market, Lemonade gained approval for their car insurance product before the end of 2021. At present, it is only available in one US state (Illinois) but this should expand to several dozen states over the coming 6-12 months. As I mentioned in my last article on Lemonade, the opportunity in car insurance is massive. I estimated that the launch of car insurance alone could generate up to 100m of additional IFP for Lemonade just from existing customers.

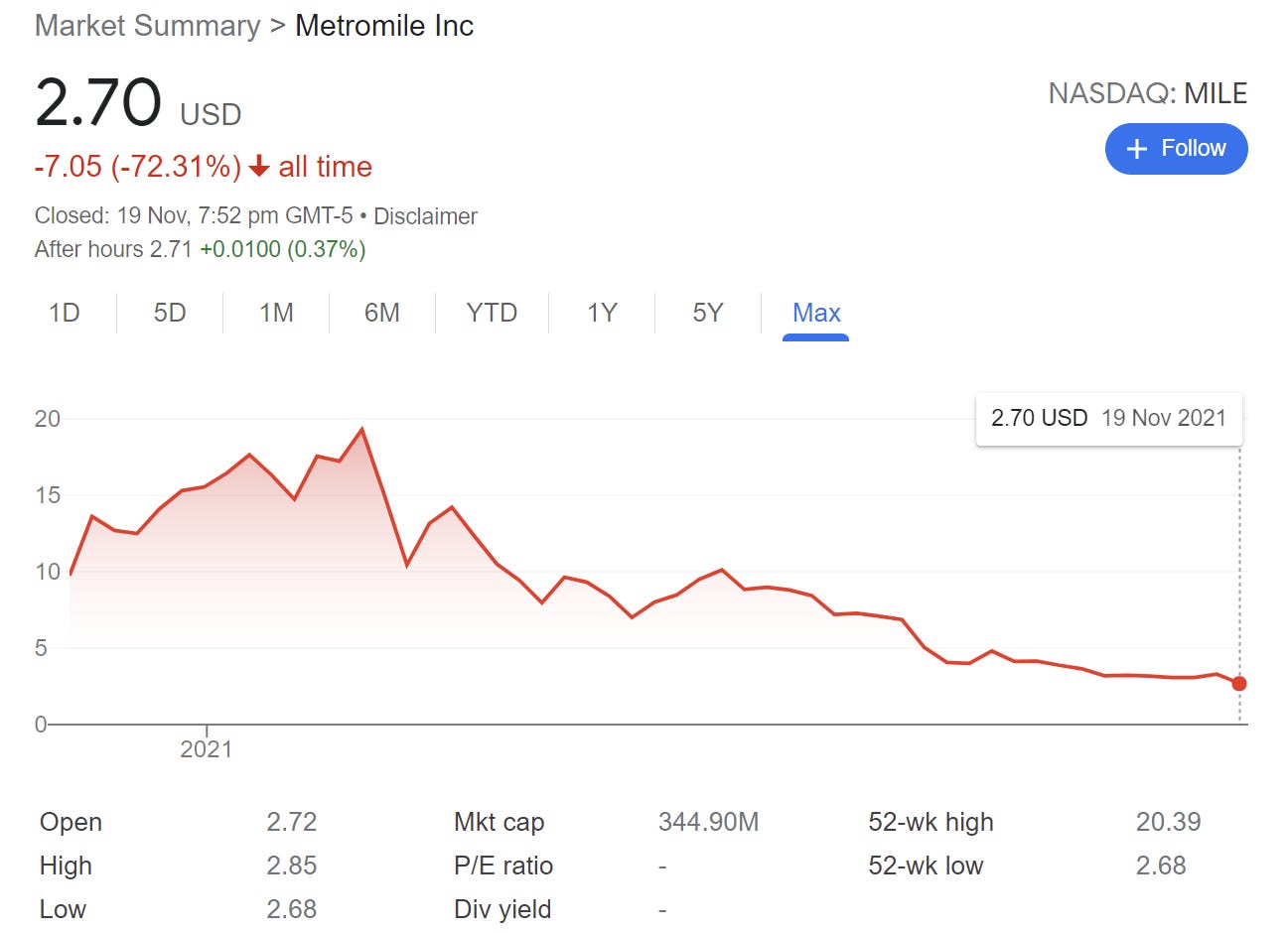

But what is more interesting about the launch of their car insurance product was the shock decision to acquire one of their competitors (Metromile) in an all-stock deal. Metromile is another new-age insurance business founded in 2011 that specialises in car insurance. Despite producing horrid returns for public market investors since their IPO (see below), Metromile boasts some impressive investors on their cap table, including Mark Cuban, Chamath Palihapitiya, and Bill Miller.

Metromile’s proposed competitive advantage was that their car-mounted precision sensors which assess driving behaviour (e.g., total miles driven, driving location, quality of driving, etc) — a methodology known as telematics — could be cross-referenced with actual claims data to provide more accurate predictions for losses per mile driven. This lies in contrast to incumbents (e.g., Geico) that are much more reliant on proxies like credit score and marital status, which are less correlated with driving abilities. On a theoretical level, the use of telematics should result in more accurate pricing of car insurance policies.

Lemonade is acquiring 100% of Metromile in an all-stock deal which values them at an enterprise value of around 200m and a multiple of less than 2x 2021 forecasted IFP. For context, Lemonade trades at an EV to 2021 forecasted IFP multiple of more than 5x so there is some valuation arbitrage where Lemonade can acquire around 100m of IFP at a lower valuation multiple than their own business. However, this valuation discrepancy makes sense as Lemonade has a 2-year compound annual growth rate (CAGR) in IFP of over 100% while Metromile has a 2-year CAGR in IFP of less than 5%.

Some benefits of the acquisition include:

Lemonade gains around 100m in IFP.

Lemonade gains access to an additional 100,000 customers to cross-sell other products.

Accelerates Lemonade’s expansion of their car insurance product throughout the US as Metromile has existing licenses in 49 US states.

Provides a decade’s worth of data that Lemonade can use to improve their machine learning algorithms.

Reduces the need for Lemonade to spend in 2022/2023 to build out the infrastructure to support their new car insurance product, such as hiring claims support staff.

However, Lemonade bears might come to the following less favourable conclusions:

Merging two unprofitable insurance businesses without clear competitive advantages to boost premiums/revenues does not address the fact that both businesses are structurally unprofitable. Time will tell if this assertion is correct.

The acquisition represents an attempt to mask a slowdown in organic growth. I see no evidence for this claim to date as premiums/revenues for all of Lemonade’s existing product lines (excluding term life insurance) are doing well.

If Metromile has so much available data that can be used to accurately price insurance policies, why have they not been able to succesd on their own?

Why fund the deal using equity near a 52-week low when Lemonade has a net cash position of over 1.1b?

I am mixed on this acquisition. The valuation multiple seems reasonable and it definitely makes it easier for Lemonade to expand their car insurance product throughout the US. Moreover, it provides them with valuable data in the car insurance market. The question is whether Lemonade will be able to utilise this data to more accurately price policies and accelerate the rate at which they are able to achieve sustainable loss ratios below 75%.

Overall

I still remain very bullish on Lemonade over the long-term. The stock has sold-off around 20% over the past few weeks due to bearish sentiment surrounding the business and the broader sell-off in unprofitable growth stocks with rising inflation numbers. It’s rare to find a business with a disruptive business model, huge total addressable market (TAM), high double-digit and accelerating organic growth rates, and a founder-led management team with lots of skin in the game that has seen multiple compression of more than 80% in the past 12 months. I expect long-term holders to be rewarded for their patience and persistence, but do not expect a smooth journey along the way.

Cheers,

Jordan

Hi Jordan,

I love your analysis and I could not agree more.

I'm also very bullish on LMND. But when LMND launched its new car insurance, I thought like: "Yeah, that's the right move. And it's going to be their 'proof of concept'. Since renter and pet are more like small markets, it really seems like car insurance is a huge and very competitive market. If they succeed in the car insurance market, the management really is top." But now I feel somewhat disappointed, because now we are not able to really judge them on their "own" work if they buy Metromile. Also, why spend millions in building the IT infrastructure, and a week after launch, buy a competitor that already has a (probably slightly different) IT infrastructure? Now they have to spend money on integration and data transfer...

Also I read the Metromile Q2 report. They started to build a distribution system with 600 independent insurance agents. How are they going to deal with this investments (sunk costs?) and people? Also, Metromile started a cooperation with Hippo (LMND competition), how are they going to deal with this?

As you mentioned, this acquisition raises - for me - more questions than answers.

Any thoughts?

Kind regards.