Lemonade: A Disruptive Insurance Business Firing on all Cylinders

Lemonade: A Disruptive Insurance Business Firing on all Cylinders

Lemonade has all the characteristics I look for in a secular compounder: a disruptive business model, exceptional organic growth rates, and a founder-led management team with lots of skin in the game.

General details (as at 15th October 2021)

Share price: $67.99

Market cap: 4.19b (USD)

Enterprise value: 3.03b (USD)

YTD return: -40%

Distance from 52-week high: 64%

Founding story

Lemonade (NYSE:LMND) was founded in 2015 by serial entrepreneurs Daniel Schreiber and Shai Wininger who have both worked in the technology industry since the late 1990s. The pair met through a mutual friend in 2014 when Daniel was on the hunt for a new business idea and conceived of Lemonade: a different kind of insurance business (hence the name!) that placed technology at its core and valued customer experience above all else. Just one problem. Neither Daniel nor Shai had any experience running an insurance business. So, they hired industry veteran Ty Sagalow — who had more than 25 years experience as an executive at American International Group (AIG) and Zurich — as their Chief Insurance Officer.

Shortly after founding Lemonade, Daniel (right on below image) and Shai (left on below image) met with the major software providers that service almost all large global insurance businesses and were told that it would cost them more than 1 million dollars to onboard the software with an anticipated wait-time of 12-18 months. Frustrated by both the cost and lag-time, Shai — who currently serves as Chief Operating Officer (COO) — cheekily remarked that “either I’m missing something really big, or I could code what they just showed us on my Apple Watch while driving home” (source). In a move that typifies the underdog mindset of Lemonade, Shai, along with a team of five engineers, coded the entire software stack for Lemonade from scratch within three months and launched version one of Lemonade to the public on 5th January 2016.

My (naïve) first impression of Lemonade … don’t be dissuaded by the name!

I first heard about Lemonade (the insurance business, not the drink!) in January 2021 when it popped up in my inbox on a rainy Friday morning as a stock recommendation from Motley Fool Stock Advisor. For some context, January 2021 was around the time when it seemed that every US technology company was reaching all-time highs and the SPAC market was going gangbusters. Naively, I quickly dismissed Lemonade as an overvalued, overhyped pseudo-technology company with a stupid name that relied too heavily on buzz phrases like “artificial intelligence” and “machine learning”. To be fair, Lemonade was trading at around $160 per share at the time (around 2.4x the current price), so there may have been some justification for this scepticism. However, Lemonade’s shares sold off more than 60% over the following months and the more I dug into their financial and operational metrics, the more impressed I became. At the time of publishing this article (15th October 2021), I truly believe that Lemonade can become one of the most disruptive technology businesses of the 2020s. I am officially a bear turned bull.

What is Lemonade?

Lemonade is an insurance company that uses artificial intelligence (AI) to simplify the process of purchasing insurance and making claims. Lemonade currently offers four products: renters, homeowners, pet, and term life insurance, with car insurance expected to be launched before the end of 2021. A lot of companies tout the use of AI to impress customers and investors, but AI truly sits at the core of Lemonade’s business.

Introducing AI Maya

While most legacy insurance providers (the “incumbents”) require prospective customers to endure cumbersome application processes and fill out extensive paperwork, Lemonade allows customers to purchase insurance within minutes from the comfort of their own home by speaking with their AI-powered chatbot, named AI Maya. AI Maya asks prospective customers 13 questions via the chat box on the Lemonade website and collects over 1,600 data points throughout this interaction. In addition to the standard data points collected (e.g., age, selected insurance product, location, etc), AI Maya collects a whole host of other variables, including whether people downloaded and read the terms and conditions, as well as time taken to respond to certain questions. Lemonade amalgamates all this information into an algorithm to determine the cost of insuring that specific person (i.e., their premium). There is no salesperson involved, no paperwork, and it only takes a few minutes to complete. It almost seems too good to be true.

Introducing AI Jim

While AI Maya is involved in the process of purchasing insurance, her male counterpart (AI Jim) handles the claims side of the insurance equation. In short, AI Jim asks customers to answer a series of questions about the claim and to record themselves explaining the circumstances of the claims request on camera. AI Jim analyses this video recording using facial and audio recognition software to detect inconsistencies from previous submissions, which helps to detect fraudulent claims.

While the process of purchasing insurance through AI Maya is 100% automated (i.e., requires no human interaction), not all claims can be processed by AI Jim alone. According to Lemonade’s IPO prospectus, AI Jim is able to process around 33% of claims (generally within seconds), while the remaining 66% of claims require some degree of human involvement, which is partially due to the fact that Lemonade does not allow claims to be auto-rejected by AI Jim without human confirmation.

An insurance business focused on delighting their customers … huh?

During the founding of Lemonade, Daniel and Shai hired Professor Dan Ariely (Professor of Psychology and Behavioural Economics at Duke University) as their Chief Behavioural Officer to help redesign the insurance process to be seamless, enjoyable, and trustworthy. Rather than make a small incremental improvement over the incumbents, Lemonade sought to upend the traditional insurance business model and one crucial element of this strategy involved aligning the incentives between Lemonade and their customers.

In a radical and highly controversial move, Lemonade registered as a Public Benefit Corporation (PBC) and Certified B Corp, which requires them to balance their social and environmental purpose with the pursuit of maximising shareholder value. In other words, Lemonade is legally obliged to consider a range of stakeholders (e.g., customers, workers, community) in addition to shareholders when making business decisions, which is very similar to the growing conscious capitalism movement which advocates for a multi-stakeholder orientation. While Lemonade is the only public insurance company in the world registered as both a PBC and Certified B Corp, there are a number of other well-known businesses with at least one of these designations, including Kickstarter, Ben and Jerry’s, Patagonia, Allbirds, Kathmandu (ASX:KMD), and Appharvest (NASDAQ:APPH).

It might seem odd that I — someone writing an investing newsletter that seeks to find secular growth companies that can generate 15%+ IRRs over the next decade — might be discussing a Certified B Corp. But the two are not mutually exclusive. One of the founding fathers of conscious capitalism (John Mackey) founded and operated the supermarket chain Whole Foods Market, which generated market-beating returns on the public markets for more than 25 years before being acquired by Amazon in 2017 for 13.7 billion (USD).

To be clear, a Certified B Corp is still a for-profit organisation and the maximisation of shareholder value remains very much at the heart of the business DNA. I would contend that most of the great technology businesses of the 21st century have implicitly adopted a multi-stakeholder orientation, albeit without the official title of being a PBC or Certified B Corp. For example, FAANG companies (Facebook, Apple, Amazon, Netflix, Google) have, for the most part, adopted an unwavering focus on attracting top talent and improving customer experience (side note: for those questioning whether Facebook fits with the list, please consider that Facebook’s customers are their advertisers, not their users). Businesses that do not prioritise providing exceptional value for their customers and hiring/retaining excellent staff are at the whims of business and technological disruption. A narrow focus on maximising profits in the short-term while exploiting customers is the antithesis of good business practice. Just ask Valeant Pharmaceuticals (link).

I believe that this decision by Lemonade to become a PBC and Certified B Corp is a brilliant strategic move to (1) build trust with customers, (2) cultivate their ‘purpose before profits’ brand image, and (3) attract top talent. More than ever, millennials and gen z workers are drawn to support companies that value social purpose in addition to financial outcomes (source). Lemonade is well positioned to attract these smart and ambitious millennial and gen z workers, which could confer a major competitive advantage over the incumbents. Time will tell if this supposition is correct.

Overall, Lemonade offers a much simpler and more frictionless customer experience than their incumbent competitors. Customers can purchase insurance within minutes and have entire claims processed within seconds. Lemonade is also incredibly transparent with their product offering; they actually post their policies prior to public launch on the open source platform GitHub (link) for community members to provide feedback on which parts are confusing, difficult to read, and/or contain unnecessary jargon. In short, this is a company that prioritises delighting their customers above all else.

Targeting a much younger customer demographic than their incumbent competitors

One major differentiator between Lemonade and their larger competitors is their target market, with Lemonade strongly focused on attracting millennial and gen z working professionals. Indeed, 70% of Lemonade’s customers are under the age of 35 and an incredible 90% did not not switch from another insurance provider (i.e., they purchased their first insurance policy through Lemonade). Daniel Schreiber, CEO, summed it up on a recent interview where he said that Lemonade focuses on “younger technologically driven consumers who are listening to their music on Spotify and staying at an Airbnb when they go on vacation”. That pretty much summarised my whole life in one sentence … am I that generic?

Targeting this younger demographic is a bold move that invokes short-term pain for long-term gain. Working professionals in their 20s and 30s generally have less income to spend on insurance policies in the present, but this amount should increase in the future as they become older and gain more personal and professional responsibilities. If Lemonade is able to develop brand loyalty and goodwill with these millennial and gen z customers at the earlier stages of their working life, they will be able to generate decades of recurring and increasing revenue from this existing customer base, reducing their dependence on new customer acquisition.

Let’s use the hypothetical example of a 23-year-old millennial (Luke) to make this more concrete. Luke purchased renters insurance a few months ago through Lemonade after moving out of home to begin full-time work. Renters insurance alone does not represent an overly profitable endeavour for Lemonade who would have spent a decent amount on sales and marketing to acquire Luke as a customer. However, Luke is likely to go through a number of predictable lifecycle events over the next 10-20 years which means that Lemonade should reap dividends for years to come if they can retain Luke as a customer. For example, Luke might:

Move in with a romantic partner at the age of 26 and buy a furry companion to keep them company, making him a candidate for Lemonade’s pet insurance;

Get multiple promotions at work and save enough with his partner to put down a deposit on a home at the age of 30, meaning he will upgrade from renters insurance to homeowners insurance;

Decide at the age of 35 (mid-life crisis) to treat himself with a brand new Porsche, making him a candidate for Lemonade’s car insurance; and

Begin to contemplate his mortality at the age of 43 and consider taking out a term life insurance product with Lemonade.

This above example demonstrates that if Lemonade can acquire a customer at the beginning of their working life and retain them as a customer, there are in a sense inherent price increases built into their customer timeline as they take out additional insurance policies to cover more domains of their life.

A rapidly growing product offering

When Lemonade went public in July 2020, they only offered renters and homeowners insurance. In the past 15 months, Lemonade has expanded their product offering to also include pet insurance and term life insurance, with car insurance expected to be launched before the end of 2021.

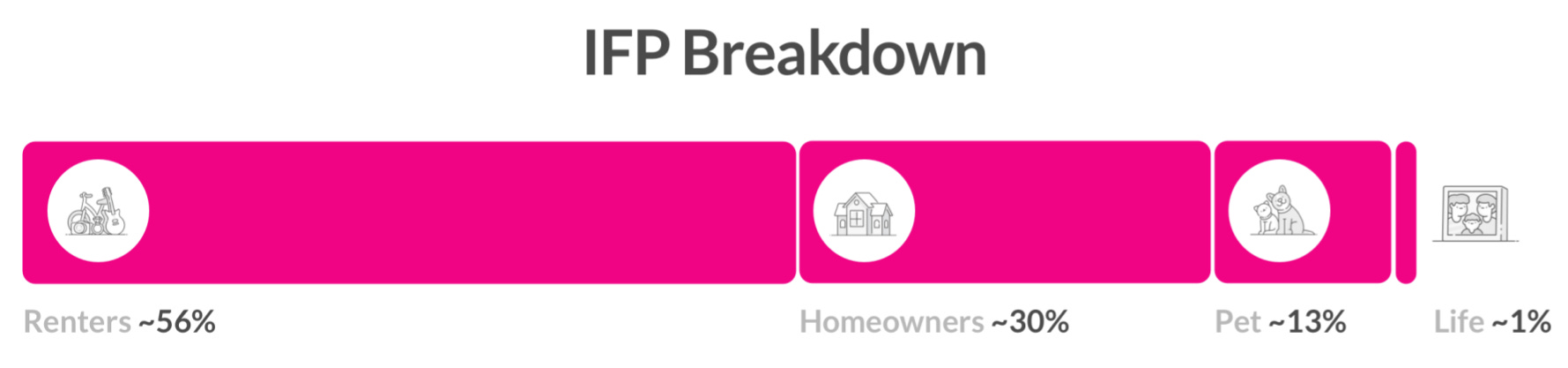

The below diagram indicates the percentage of in force premium (IFP; total premiums collected from active policies) generated from each of these product lines as at Q2 2021 (30th June 2021). Keep in mind that pet insurance was launched in July 2020 and term life insurance was only launched in January 2021, so they haven’t had a lot of time to meaningfully contribute to total IFP. While renters insurance still accounts for more than half of IFP, its concentration risk has reduced dramatically since IPO.

Each of these product lines are showing excellent traction (except possibly term life insurance). In Q2 2021, renters insurance grew at around 50% year-over-year, while homeowners insurance grew at more than 100% year-over-year. While growth rates for pet insurance are not reported, Daniel Schreiber noted that pet insurance achieved profitable unit economics within months of launching; a feat which took several years for their more mature homeowners product.

Lemonade’s pace of innovation in adding new products is a major competitive advantage. While established incumbents (e.g., Geico and State Farm) offer a range of insurance products, most of Lemonade’s modern competitors only offer single products. For example, Hippo (NYSE:HIPO) only offers homeowners insurance, while Metromile (NASDAQ:MILE) only offers car insurance. Nonetheless, these businesses had large enough total addressable markets (TAMs) to attract some big-name investors, including Chamath Palihapitiya (Metromile), Bill Miller (Metromile), Mark Cuban (Metromile), Ribbit Capital (Hippo), and Dragoneer Investment Group (Hippo).

Offering four (soon to be five) products allows Lemonade to (a) offer greater convenience for customers to collate multiple policies into a single platform and (b) offer price discounts for customers who bundle two or more insurance products together (e.g., renters insurance with pet insurance). CEO Daniel Schreiber frequently described Lemonade as operating with “one hand tied behind their back” when renters and homeowners insurance were their sole products, due to the absence of these bundling discounts. I’m excited to see where Lemonade can go with both hands free.

The opportunity in car insurance for Lemonade is massive

The US car insurance market is enormous. Recent estimates from Lemonade value the industry at around 300 billion (USD), which is more than 70x larger than both the renters and pet insurance markets combined (source). Lemonade’s internal estimates suggest that most of their existing customers are already car owners and spend around 1 billion per year on car insurance. Let’s conservatively estimate that Lemonade is able to convert 10% of existing customers who have car insurance with another provider through offering price discounts for bundling products. Such an outcome would equate to around $100m of IFP in 2022 alone (assuming car insurance is launched before the end of 2021). After Lemonade keeps 30% of that IFP (business model to be explained soon), that is approximately a $30 million uptick in revenue in 2022 from a 2021 forecasted revenue base of $123-125 million. Thus, there is enormous opportunity for car insurance to become a meaningful part of Lemonade’s business within 12 months of launch solely from their existing customer base.

Geographical expansion - another element of the growth equation for Lemonade

I won’t delve too deep into Lemonade’s geographical expansion plans because it doesn’t form a fundamental part of my thesis. The US insurance market is more than large enough for Lemonade to increase their IFP 10x and still represent a drop in the bucket of total premiums in the US. As at Q2 2021, at least one Lemonade product was available in each of the 50 US states and I expect this to be rolled out for all of their insurance products within 12-24 months, providing a powerful tailwind for growth.

Lemonade’s core market is the US and this is where they have focused most of their resources due to more attractive unit economics than Europe. Nonetheless, they have recently expanded some products into Europe to test the waters, including Germany (June 2019), Netherlands (April 2020), and France (December 2020). CEO Daniel Schreiber has noted in recent interviews that Lemonade is seeing increasing conversion rates and declining loss ratios in Europe, so will likely be investing more over the next 12-24 months into expanding their geographical footprint throughout Europe.

Personally, I am excited, but not in a rush, to see Lemonade go for world domination. Although operating on a global scale would further diversify Lemonade’s revenue mix, it also adds additional execution risk. Moreover, the US market alone is enormous; if Lemonade is unable to grow their premiums and revenue meaningfully over the next decade, it has nothing to do with the size of the TAM.

Lemonade’s technology advantage over incumbent competitors

Lemonade is a modern company founded by technology entrepreneurs who made a conscious decision to structure their business operations around digital automation. Their technology infrastructure (CEO Daniel Schreiber calls this their “digital substrate”) powers multiple facets of their business, including loan underwriting, claims processing, fraud detection, and sales and marketing. This digital substrate provides an enormous competitive advantage over less technology-savvy competitors, as Lemonade is able to add new products and expand into new geographies without a proportionate increase in the cost of capital and staffing costs, which affords significant pricing power at scale.

Lemonade also collects a tremendous amount of data (> 1,600 data points) during the loan underwriting process, which is fed into their algorithm to calculate premiums. On a theoretical level, as Lemonade gathers more data over time through more customer interactions, the success of their loan underwriting and claims processing should improve. Indeed, one of the best performing stocks in the US market over the past 12 months is Upstart Holdings (NASDAQ:UPST), which provides an AI algorithm as a subscription service to banks and financial institutions to improve their loan underwriting, and is valued at more than 30 billion USD with forecasted 2021 revenues of 750 million. There is enormous value to be gained from being the best at pricing risk in a loan or insurance context.

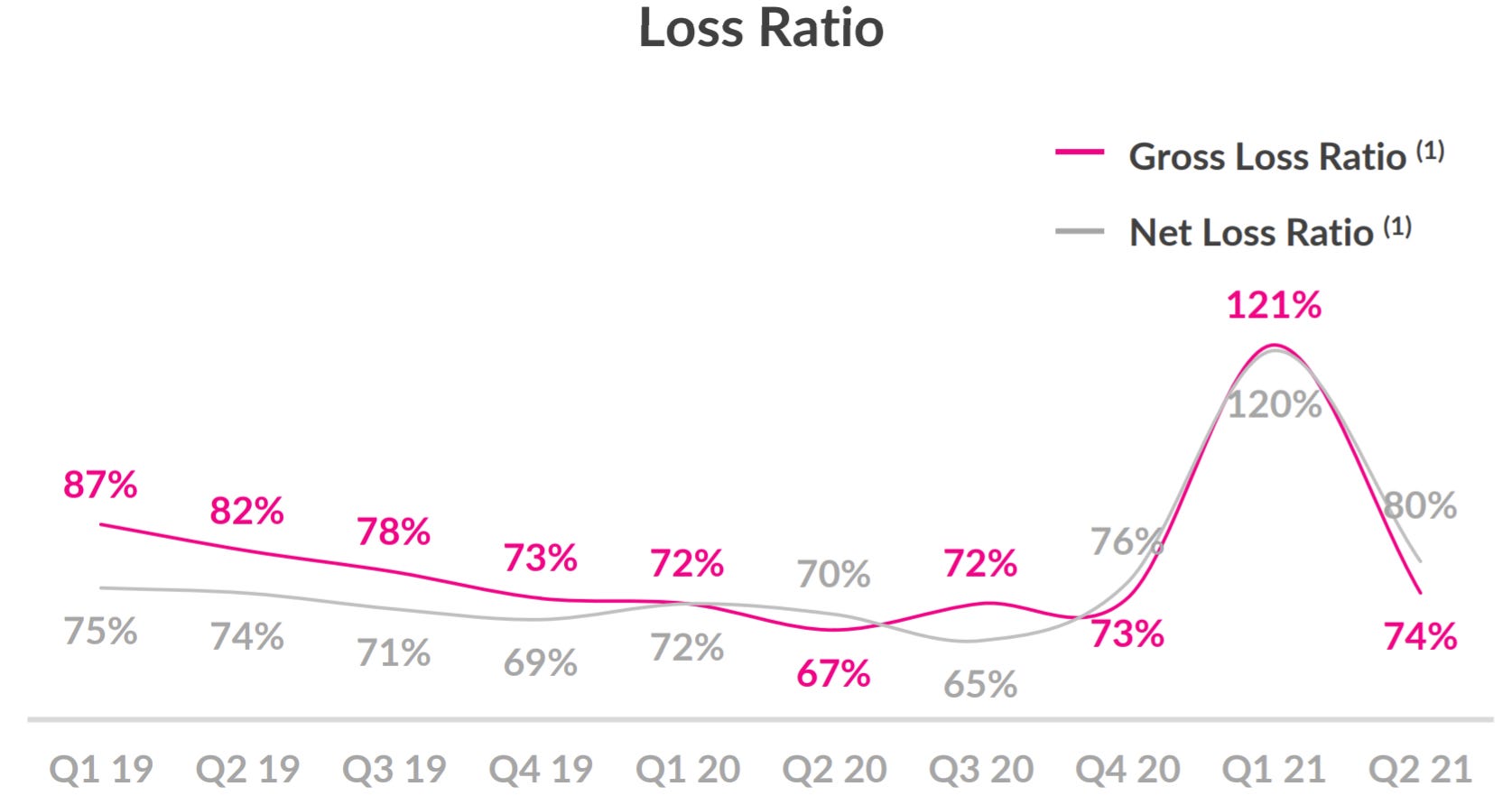

The continuation of this positive feedback loop is crucial to Lemonade’s future success and is evident in decreasing loss ratios (a measure of incurred losses divided by collected premiums) from Q1 2019 onwards (note: Q1 2021 was temporarily affected by the Texas Freeze).

While declining loss ratios suggest that Lemonade’s algorithm is becoming better at pricing risk over time, it is also helpful to consider other metrics that might indicate whether Lemonade truly has a technology advantage over their incumbent competitors.

Number of customers per employee

If Lemonade had a technology advantage over their competitors and was able to automate more of their business operations, it should materialise in a higher number of customers and policies per employee. Although it is very difficult to find more recent statistics than 2018, it appears that these assumptions broadly hold true. Lemonade has around 5x the number of customers per employee and 2x the number of policies per employee compared to their nearest competitor (State Farm).

Frequency of software upgrades

CEO Daniel Schreiber has noted in numerous interviews that Lemonade averages 20-30 software upgrades per day compared with 4-5 upgrades per year for their incumbent competitors. While I have no way of verifying whether these claims are true, it seems approximately believable and could provide an additional indicator of Lemonade’s ruthless focus on improving customer experience.

Geographical expansion without relocation

Perhaps the most impressive demonstration of Lemonade’s technology advantage is that they do not have a single employee based in either of their two largest US markets of California and Texas. Moreover, Lemonade offers contents and liabilities insurance in Germany but does not have a single employee based in Germany (although I assume there must surely be at least one employee in another country who can speak a little German!).

Overall, the combination of these three factors adds credibility to Daniel Schreiber’s claims that their digital substrate is indeed a major source of competitive advantage for Lemonade, as it allows them to expand into new products and geographies without significant increases in human capital.

Lemonade’s disruptive (and controversial) business model: the secret sauce?

Lemonade has an innovative business model that is a stark departure from standard practice in the insurance market. But, before we discuss what makes Lemonade’s business model unique, we first need to understand the modus operandi for an insurance business.

In its simplest form, insurance offers a guarantee to trade the risk of a possible future catastrophe with a certain and much more affordable loss in the present. Insurance acts as a safety net where people pool their dollars together so that these resources can be used to support unfortunate members during times of hardship (e.g., to cover unexpected medical bills for a sick pet).

All the money that customers pay for their insurance policies is referred to as premiums, which represent, in a simplistic sense, the inflows for an insurance business. If something happens to a customer that is covered by their insurance policy (e.g., they are involved in a car crash and have car insurance), they are entitled to make a claim for the insurance company to pay either all or some of the cost of the accident. The exact amount paid out by the insurance company depends on the level of cover provided in the insurance policy, which is stipulated in the contract. These claims represent, in a simplistic sense, the outflows for an insurance business.

Thus, an insurance business makes a profit when premiums (inflows) exceed claims (outflows), all other things being equal. Let’s ignore other factors, such as investment income and operating costs, to keep things simple. What this means is that an insurance business is incentivised to (1) collect as much in premiums as possible and (2) minimise the amount of claims paid out to customers. The larger this difference, the greater the amount of profit for the insurance business.

Does this sound like a conflict of interest? It is. While it can be profitable, this model creates strong misalignment between the insurer and the customer. On the one hand, customers are incentivised to (1) pay as little as possible in premiums and (2) receive as much as possible in claims. Insurers are incentivised to do the exact opposite. Sounds like a good old fashioned tug of war. No wonder why you see headlines like these in the media. Ouch.

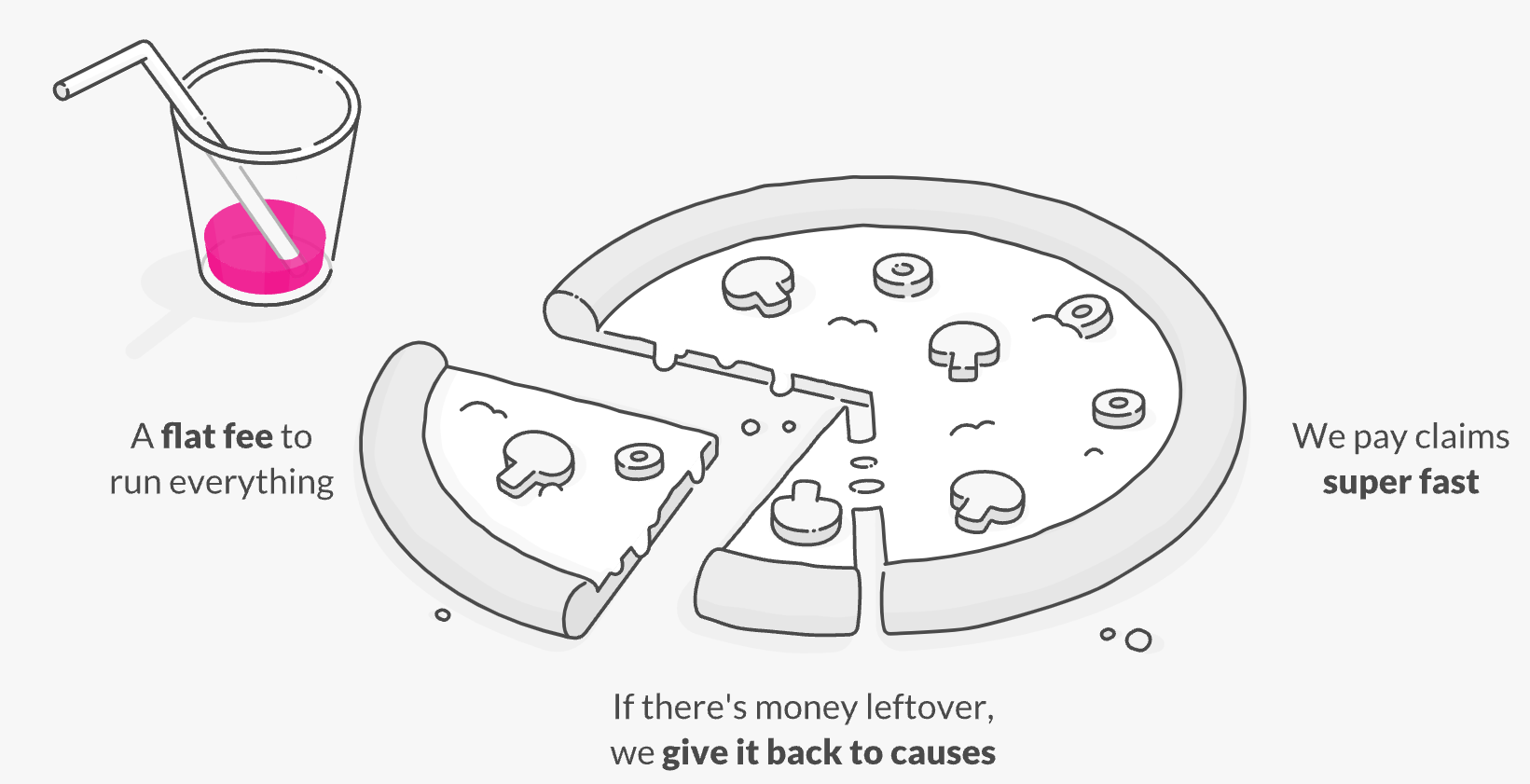

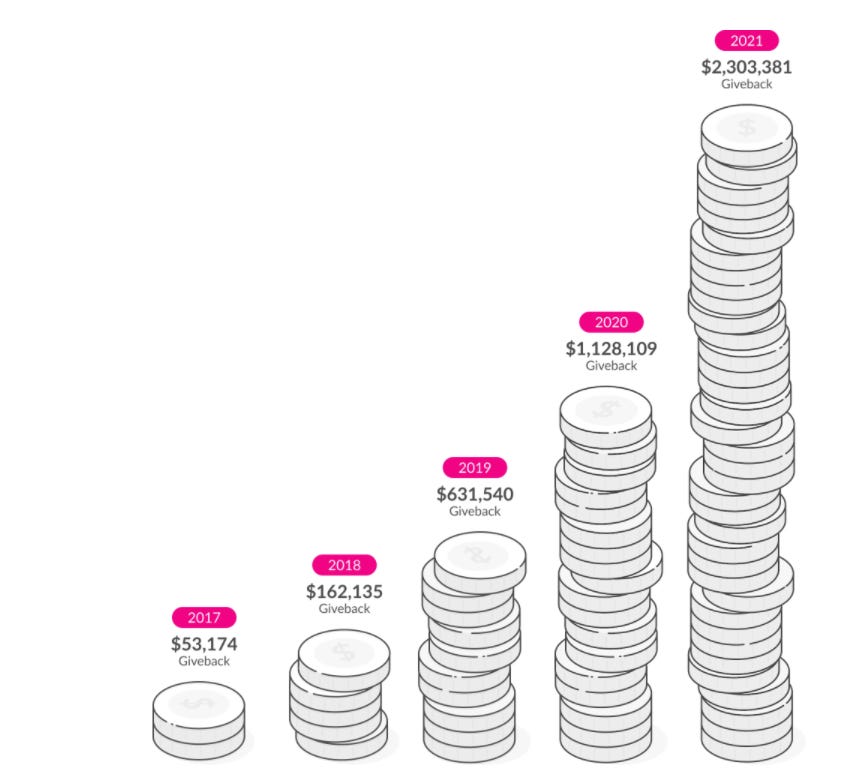

Lemonade flips this model on its head and creates alignment between a customer and the insurer (for context, the main slogan on Lemonade’s website is “forget everything you know about insurance”). Lemonade collects a fixed fee (currently 30% of premiums) that is used to cover expenses and their proportional share of customer claims, with the surplus being used to generate a small profit. The remaining 70% of premiums are ceded to reinsurers who cover their proportional share of customer claims. Anything that is left over at the end of the calendar year from this 70% is donated to charities as part of their giveback program (link), where customers vote on which charities they want their donations to be made to. Thus, incentives are aligned between Lemonade and their customers. Lemonade already keeps a flat fee (30%) and excess dollars that are not claimed from the 70% are paid out to charity, so Lemonade has no incentive to deny customer claims.

This giveback program is a critical element of Lemonade’s role as a Certified B Corp and in building trust with their customers. And it isn’t just a vanity metric; Lemonade donated more than 2.3 million (USD) to charities in 2021, which was more than double the amount donated in 2020, and up more than 40-fold from the amount donated in 2017.

Let me delve a bit deeper into Lemonade’s reinsurance model. Insurance is a complex business to forecast; it’s inherently very lumpy and insurance companies can be forced to cover large claims during one-off tail events, such as natural disasters, at short notice. Lemonade reinsures around 70% of their premiums which allows them to boost their capital efficiency and reduce their capital requirements for these one-off tail events. Without their reinsurance model, Lemonade would need to reserve as much as 50c per $1 of collected premium (2:1 ratio). With their reinsurance model, most of the surplus capital requirements are shifted to the reinsurer, so that the current capital requirement is more like 14c per $1 of collected premium (7:1 ratio). Thus, because Lemonade does not need to hold as much cash reserves on their balance sheet, they are able to re-invest more capital into the business for growth.

As part of this reinsurance agreement, reinsurers: (1) pay Lemonade a ceding commission of 25% of every dollar reinsured, (2) fund all of the corresponding claims (e.g., 70% of all Lemonade’s claims), but (3) receive all premiums in return. This reinsurance model worked exactly as designed in Q1 2021 during the Texas Freeze when millions of people were left without power, leading to shortages in water, food, and heat. Despite this crisis, Lemonade was shielded from 75% of the claims due to their reinsurance model (note: at the time they reinsured 75% of premiums, rather than 70%).

CEO Daniel Schreiber has noted in numerous interviews that Lemonade isn’t beholden to their current reinsurance model but deliberately chooses this model because it allows them to continue to invest more capital into their business for growth. Over time, he foresees that Lemonade will reduce the proportion of premiums ceded to reinsurers as the business becomes more diversified across product lines and geographies. This trend has already begun to play out; when I began researching Lemonade in March 2021, they reinsured 75% of their premiums, which was recently reduced to 70% in Q2 2021.

The current state of the US insurance market

Lemonade operates in one of the biggest markets in the world: the US insurance market. Recent estimates suggest that the total value of all premiums written in the US is around $1.3 trillion (USD), so Lemonade has lots of room to expand before even achieving a 1% market share.

Another interesting characteristic of the US insurance market is that it is highly fragmented. When we think of a US e-commerce business, we think of Amazon. When we think of a US electric vehicle maker, our mind goes to Tesla. In the US insurance market, however, there are almost 6,000 insurers (source), with no one insurer boasting more than a 5% total market share across all products. That is some serious fragmentation.

Circumventing the switching costs inbuilt into the insurance industry

How many times have you changed your car insurance policy over the past five years? I’m going to assume not more than once or twice (at most). Insurance isn’t like a Netflix subscription where you can easily cancel and re-activate your subscription depending on their monthly selection of movies or TV shows - it’s a complicated, time-consuming, and laborious process that involves filling out lots of paperwork and often speaking to multiple people on the phone. This moat (known as switching costs) is a big reason why large incumbents in the US insurance market have been able to survive (but not necessarily thrive) since 2000 in the midst of massive technological disruption in other markets.

The reality of the situation is that it is very difficult to convince a busy working professional who might have been with an insurance provider for more than a decade and receives bundling discounts to switch to a new-age insurance provider like Lemonade. The default option is to just stick with their current insurance provider and avoid the hassle of switching, even if there might be a small financial incentive to do so (e.g., a 5% yearly reduction in premiums).

But this is the beauty of Lemonade’s strategy. They are not targeting these older customers who have entrenched relationships with existing insurance companies. They are targeting millennial and gen z customers, 90% of whom are purchasing insurance for the first time. Of Lemonade’s 1.2 million active customers, almost 1.1 million of them have never purchased insurance before and have chosen to begin their insurance journey with Lemonade. This is a big advantage for Lemonade as it helps them circumvent the switching costs inherent in the insurance industry and reduces their degree of competition with incumbents.

Lemonade’s power advantage over incumbents: counter-positioning

Counter-positioning is one of the competitive advantages described in Hamilton Helmer’s seminal book 7 Powers: The Foundations of Business Strategy and suggests that upstarts can have an inherent advantage over incumbents when (1) they have a superior and unorthodox business model and (2) incumbents are unable to respond to the competitive threat. Let me explain in more depth.

As mentioned earlier, Lemonade has a radically different business model to that of the incumbents. They are a Certified B Corp and digital automation lies at the core of their operations. There is no way that Geico founded in 1936 with tens of billions in revenue will be able to quickly (or efficiently) upend their entire model of selling insurance policies through sales representatives and brokers to compete with Lemonade’s D2C AI chatbots (AI Maya and AI Jim). And why would they? Their customer base tends to be much older than that of Lemonade’s. What would a 60-year old who has four policies with Geico think if they were asked to submit claims via a chatbot rather than speaking on the phone with their normal client representative who they have been working with for more than a decade? I would love to be a fly on the wall for that conversation …

Moreover, redesigning their business model to be centered around automation would likely result in thousands of redundant staff, terrible PR, and significant short-term pressure on revenue and margins. There is little incentive for senior executives at an established insurance business to upend their business model, and risk reputational and financial damage to compete with an unproven upstart like Lemonade or Hippo. The default option for the management team at an incumbent business is to do nothing, continue receiving their large salaries and stock bonuses, and hope a natural disaster wipes out Lemonade.

But not all larger competitors have chosen the ‘do nothing’ approach. Some have tried (and failed) to wipe out or replicate Lemonade. Let’s be clear. In the context of the broader US insurance market, Lemonade is the clear underdog (i.e., David) and the incumbents are the favourites (i.e., Goliath). But what if we flip the equation and consider the US insurance market for millennial and gen z customers who want a digital and seamless customer experience? Lemonade is Goliath and the incumbents are a long string of David’s.

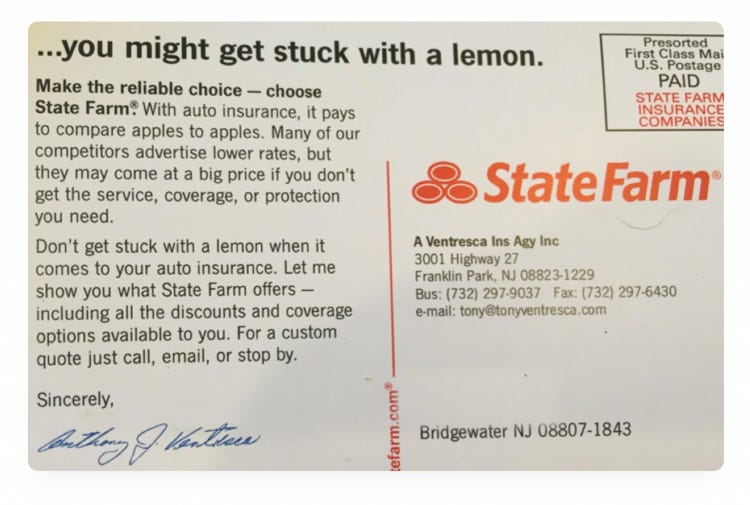

For example, in an attempt to dissuade customers from switching to Lemonade, State Farm (a company with over 75 billion in annual revenue) sent out postcards to customers in 2017 urging them not to “get stuck with a lemon”. They’ve clearly taken note of Lemonade.

Not to be outdone, Liberty Mutual (a company with over 40 billion in annual revenue) also attempted to deter customers from switching to Lemonade, but via direct replication of their offering. In 2017, they launched Lulo, a near-perfect imitation of Lemonade, copying their logo, font, pricing, and messaging. This was quickly shut down by Lulo and is no where to be seen in 2021. Copying Lemonade at their own game is a recipe for disaster.

How does Lemonade stack up to their modern competitors?

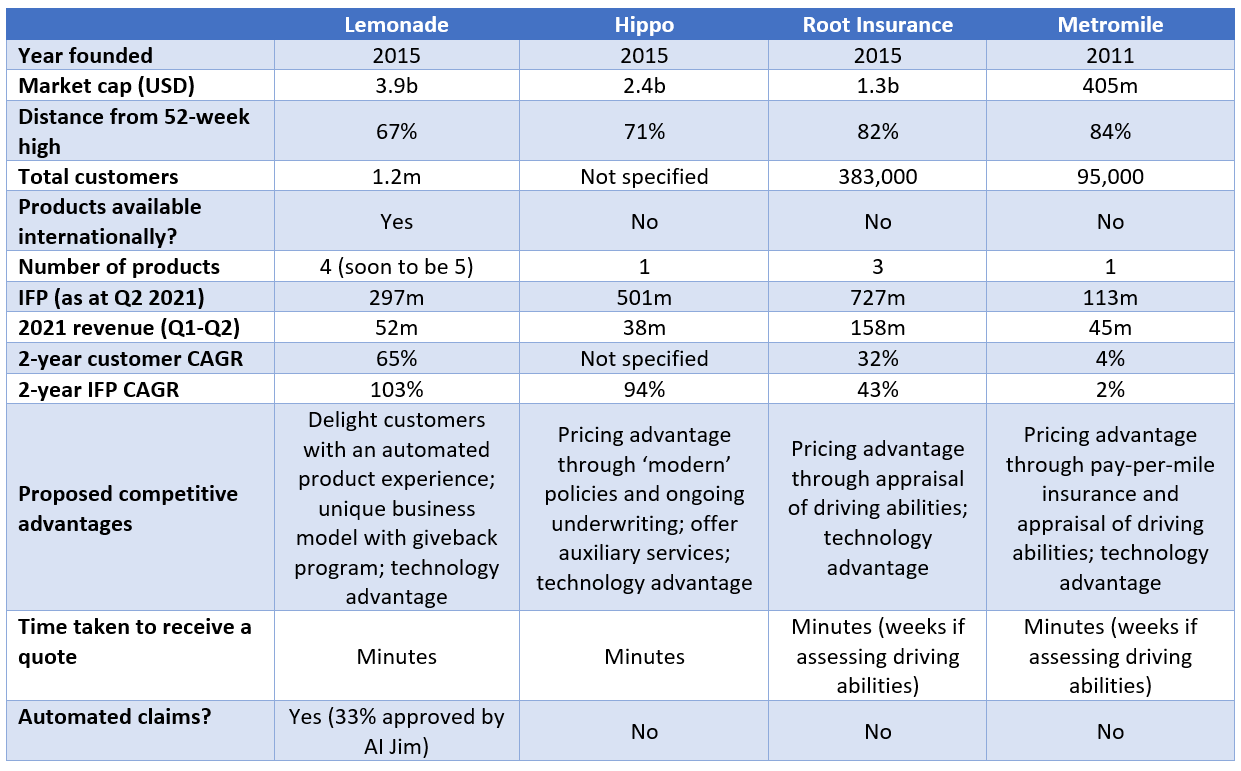

Lemonade is not the only new-age insurance business using technology to disrupt the incumbents like Geico, State Farm, and Progressive. So, what makes me confident that Lemonade will emerge as the leader of these new entrants? I outline a number of reasons below, but it is worth noting that insurance is not a ‘winner takes all’ market and Lemonade does not need to be the sole winner from this pack to generate attractive returns for investors. Despite large sell-offs in 2021, I expect that collectively these four new-age insurance businesses (in combination with many others which are not yet public) will take significant market share away from incumbents over the next few decades as millennial and gen z customers who value a digital-first product experience become a larger portion of the working economy.

Customers

Lemonade has the largest customer base, with over 1.2 million customers as at Q2 2021 (note: Hippo did not disclose customer numbers in their most recent shareholder letter).

Products

Lemonade is the only company with at least one product available in all 50 US states and an international presence. Moreover, Lemonade offers the greatest breadth of products with four available products (soon to be five with the upcoming launch of car insurance), which allows them to offer price discounts to customers who bundle multiple products. Root Insurance is the only other modern competitor with multiple products with car, renters, and homeowners insurance.

To remain competitive, Hippo and Metromile partnered in May 2021 to offer discounts to customers who bundle Hippo’s homeowners insurance with Metromile’s car insurance. While this could be a viable solution in the short-to-medium term, it suggests that Hippo and Metromile do not have the technological capabilities (or willingness) to launch multiple products, which reduces their ability to build a product ecosystem for customers. In addition, it decreases their ability to control the customer experience and adds unnecessary reputational risk. For example, if a customer signs up for Hippo’s homeowners insurance and bundles it with Metromile’s car insurance, and then has a poor customer experience with Metromile, Hippo suffers brand damage given their association with Metromile. Lemonade and Root Insurance have instead invested upfront to build out multiple products, which affords them greater control over the customer experience and increased access to customer data.

Premiums and customers

Of the four companies, Lemonade sits 3rd behind Hippo and Root Insurance in terms of in force premiums (IFP) and 2nd behind Root Insurance in terms of total revenue (note: Hippo reinsures 90% of their premiums which explains why they have less revenue through the first half of 2021 than Lemonade).

However, Lemonade is growing customers and premiums faster than their competitors, with a 2-year customer compound annual growth rate (CAGR) of 65% and a 2-year IFP CAGR of 103%. Hippo is a close second with a 2-year IFP CAGR of 94%. Root Insurance’s trailing 2-year growth rates are respectable, but their guidance indicates major growing pains ahead. In their Q2 2021 earnings update, Root forecasted year-over-year declines in both premiums/revenue in Q4 2021 and for the whole of 2022. For a business in only their 7th year of operations with multiple product lines, this guidance is very uninspiring. Metromile is the slowest growing of the four with a low single-digit CAGR in customers and IFP over the past two years. Thus, while Lemonade and Hippo are rapidly gaining market share and growing premiums, Metromile and Root Insurance appear to be plateauing, explaining the differential valuations between the four businesses.

Proposed competitive advantage

As expected, all four businesses highlight their technology advantage over incumbents on their websites, but interestingly shy away from directly comparing themselves with each other. All four use novel methodologies to price insurance premiums. For example, Lemonade (or AI Maya) collects over 1,600 variables when appraising a prospective customer, Hippo offers ongoing underwriting using non-traditional data sources (e.g., satellite images of a home) and offers auxiliary home-care services to reduce claims, Root Insurance assesses driver abilities for car insurance, and Metromile considers both driver abilities and number of miles driven. Thus, each business offers a unique proposition that appeals to different customers.

When considering which business has collected the greatest amount of data — which could confer a data advantage in terms of underwriting and cross-selling — it appears that Lemonade is the early leader with the largest customer base, greatest breadth of products, and coverage across all 50 US states. However, it is very possible that companies that specialise in a single product (e.g., Hippo for homeowners insurance) might have a specific informational advantage over Lemonade in that domain. I believe that it will take another 1-3 years to truly judge who has the greatest technology advantage, so I will be closely monitoring indicators such as margins, loss ratios, and retention rates.

In terms of convenience for customers, all four companies are able to offer an initial quote within minutes, but Root Insurance and Metromile extend this duration to weeks for those that want their driving abilities evaluated to receive possible discounts to their premiums. However, Lemonade is the only business that offers at least a partially automated claims process through AI Jim; the others require speaking with a customer support representative, similar to the incumbents.

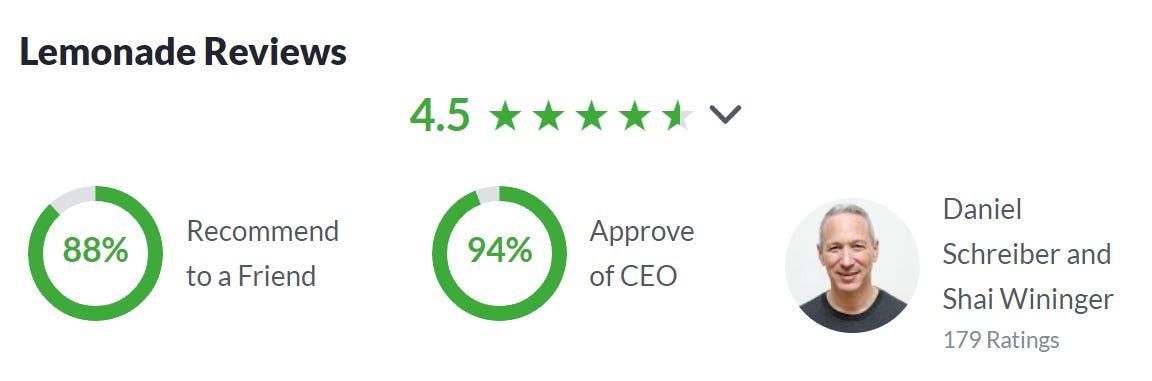

Follows the customers - and customers LOVE using Lemonade

It is reassuring to see that Lemonade’s obsession with customer experience materialises in their customer reviews. Lemonade receives consistent high scores from more than 60,000 reviews across multiple different websites. If we compare their reviews to that of both their legacy competitors (e.g., Geico, State Farm, Allstate, and Liberty Mutual) and modern competitors (e.g., Metromile, Hippo, and Root Insurance), it is clear that Lemonade is the most consistent performer with a simple average (4.7/5) that blows their competitors out of the water. Even on Trustpilot which is notorious for attracting the harshest reviews, Lemonade scores 4.4/5 which places them in the ‘excellent’ category. This is a bold claim but when I read reviews about Lemonade and see the passion with which people describe their experience it feels eerily similar to way people talk after driving a Tesla or ordering the latest product from Apple. Could that portend things to come?

Explosive organic growth across all key business metrics

By this point, you should have a solid understanding of what makes Lemonade’s business model unique, their technology advantage over incumbents, and their high levels of customer satisfaction. Let’s now dig into Lemonade’s key business metrics and evaluate whether they support the qualitative aspects of this investment thesis.

To preface this section, Lemonade’s management team is one that clearly understands the game of Wall Street, and has made a conscious choice to under-promise and over-deliver. In each quarter since their IPO in July 2020, they have beaten internal guidance for both in force premium, gross earned premium, and revenue.

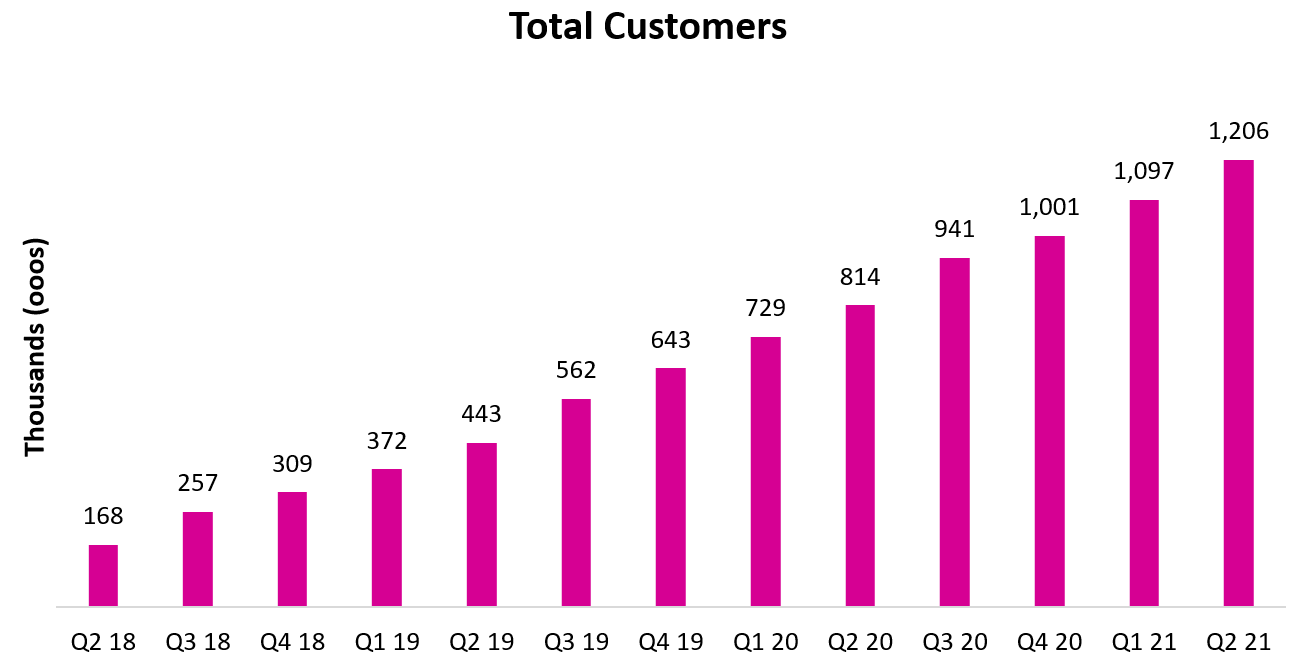

Number of customers

Lemonade has experienced phenomenal customer growth since inception. They reached 1 million paying customers in around 1,500 days (4.25 years), which is 4-11 times faster than the incumbents of State Farm, Allstate, Geico, and USAA. Indeed, Lemonade also gained 1 million customers faster than most of the B2C businesses that have become household names over the past decade, including Netflix, Spotify, and Amazon (source).

Drilling into the specifics, Lemonade has reported sequential quarter-over-quarter growth in total customers since Q2 2018, adding between 60,000-120,000 customers each quarter (this includes churn from loss of customers). During this period, Lemonade’s total customer count grew at a 3-year CAGR of 93%. I expect explosive customer growth to continue for the next 3-5 years (although likely not at a CAGR of 93%) as Lemonade continues to add new products (e.g., car insurance), expand their coverage for all products across all 50 US states, and enter new international markets.

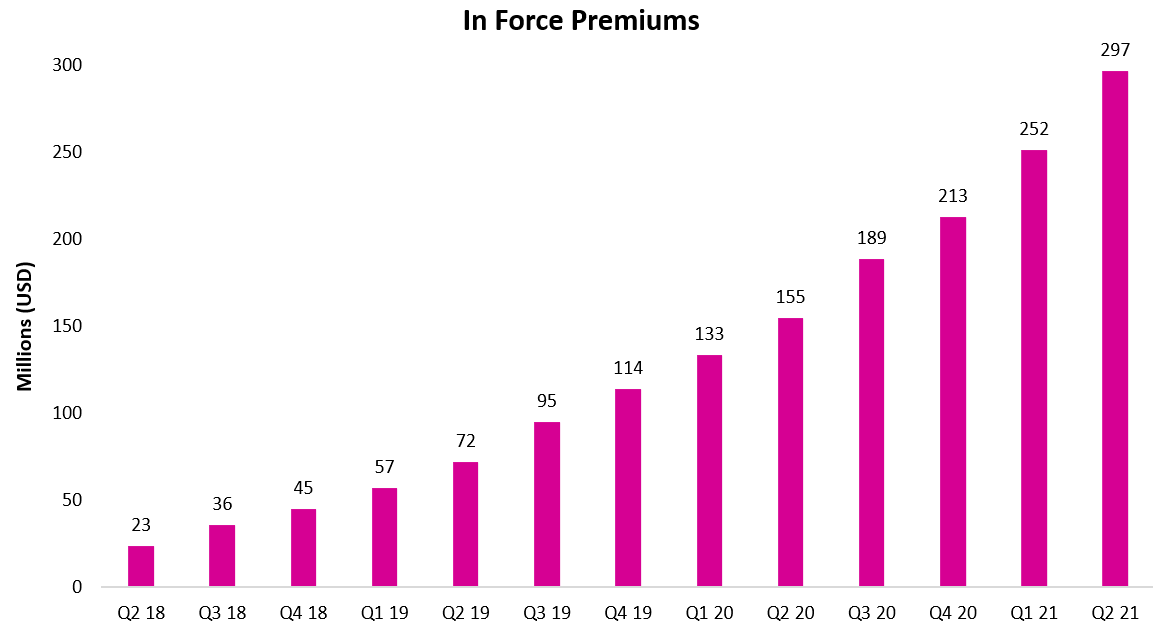

In force premiums

As with all insurance businesses, premiums are the oxygen for Lemonade. In force premiums (IFP) represent the total annualised premiums for customers at the end of a given period and is a combination of (1) policies underwritten by Lemonade and (2) policies placed by third-party insurance companies who recommend Lemonade products (accounts for < 1% of total IFP). IFP has grown at a 3-year CAGR of 135% since Q2 2018 and has accelerated in the past three quarters from 87% year-over-year (Q4 2020) to 91% year-over-year (Q2 2021). Lemonade is conservatively forecasting yearly growth in IFP of 78-80% in 2021, which does not include any contributions from the upcoming launch of their car insurance product.

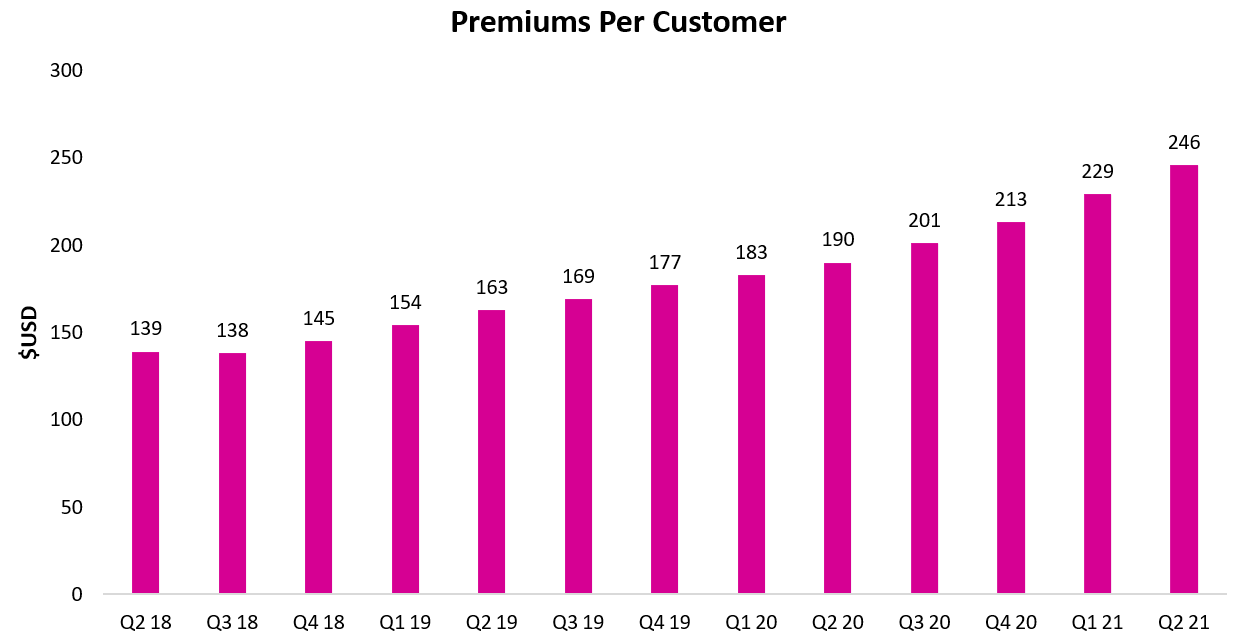

Lemonade also reports very consistent growth in premiums per customer since Q2 2018 resulting from (1) customers upgrading existing policies (e.g., changing from renters to homeowners insurance) and (2) greater opportunities for bundling from the launch of new products. Thus, Lemonade is rapidly growing their customer base at almost 100% year-over-year, and their existing customers are also spending more each quarter (3-year CAGR of 21%), providing a powerful tailwind for growth.

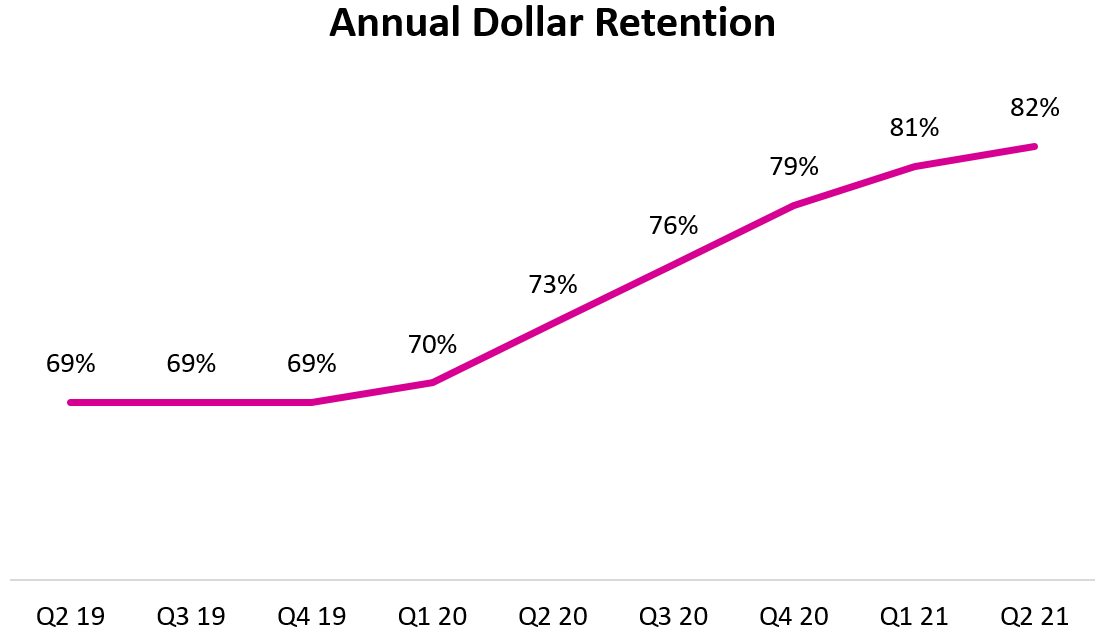

Annual dollar retention

Lemonade defines their annual dollar retention (ADR) as the percentage of IFP that it retains over a 12-month period and indicates their ability to (1) retain customers and (2) sell additional or more expensive products to these customers over time. It is broadly similar to a net dollar retention (NDR) rate for a SaaS business, but percentages are likely to be much lower as rates of churn are generally higher for insurance than SaaS businesses.

Lemonade reported an ADR rate of 82% as at Q2 2021, which has increased somewhat steadily from 69% in Q2 2019. Although this seemed low at first glance given Lemonade’s glowing customer reviews, it is within the average for insurance businesses in developed economies, which has ranged from 79-86% between 2009-2019 (source). What is pleasing is the rate of increase in ADR since 2019, which suggests that Lemonade is providing customers with better policies and has the potential to exceed those aforementioned industry retention averages over time.

Loss ratios

I have already mentioned Lemonade’s declining loss ratios in an earlier section, so I won’t dwell much on them here. The main takeaway is that that their loss ratios are consistently improving (excluding the one-off bump in Q1 2021 due to the Texas Freeze), which suggests that their algorithmic underwriting process is getting better over time. It is also important to note that their loss ratio is much higher for new products (e.g., pet and term life insurance) than more established products (e.g., renters and homeowners insurance) as their AI algorithm does not have as much available data to accurately underwrite policies. Thus, if Lemonade’s car insurance launch is successful and leads to a rapid surge in premiums, it is likely that Lemonade’s loss ratio will temporarily increase in the short-term.

Revenues

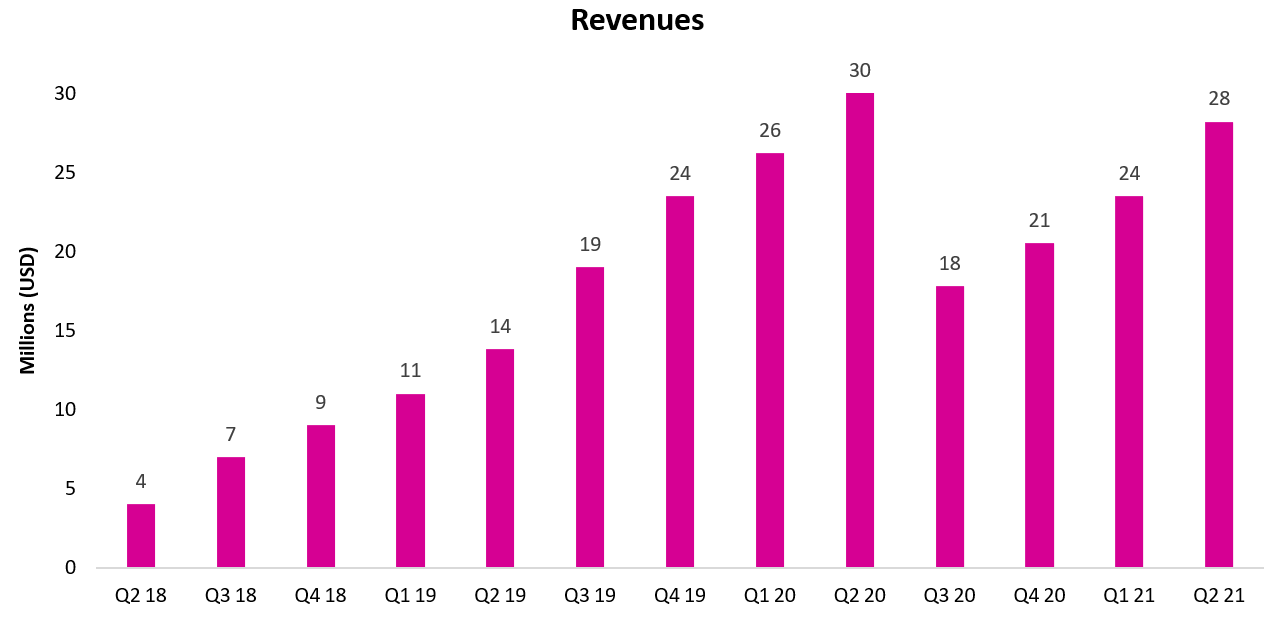

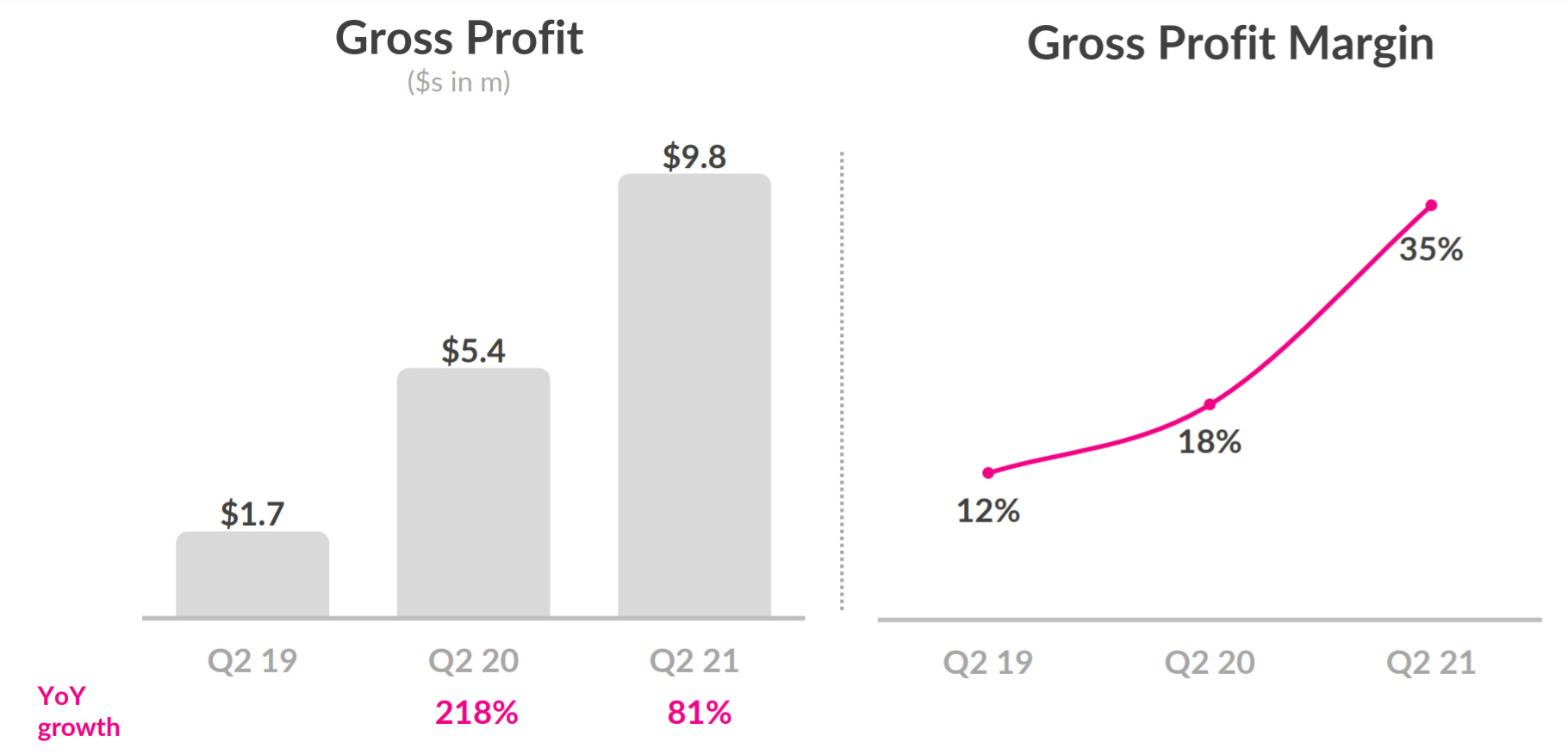

Lemonade has grown their revenues at a 3-year CAGR of 92%, which is impressive given that this includes a change in revenue recognition beginning in Q3 2020 where Lemonade decided to increase the proportion of revenues ceded to reinsurers to reduce capital constraints. As mentioned earlier, this reduces Lemonade’s required cash reserves and allows them to reinvest more capital into the business for growth, but translates to a reduction in premiums recognised as revenue. In other words, short-term pain for long-term gain.

As such, year-over-year revenue comparisons for the four quarters from Q3 2020 to Q2 2021 make it seem as though Lemonade’s business has plateaued, when in reality the business has gone from strength to strength. For example, revenue dropped more than 40% from 29.9m in Q2 2020 to 17.8m in Q3 2020, despite IFP growing 22% between quarters from 155m to 189m. If we just consider quarter-over-quarter growth rates since Q3 2020, Lemonade grew revenues at 15% from Q3 2020 to Q4 2020, 15% from Q4 2020 to Q1 2021, and 20% from Q1 2021 to Q2 2021, which are explosive quarterly growth rates.

From Q3 2021 onwards (next quarter), Lemonade’s yearly revenue growth rates should more closely reflect their growth in premiums, making it easier to appraise the strength of the business. It is even possible that revenue growth outpaces growth in IFP over the next 3-5 years as Lemonade benefits from (1) increasing premiums but also (2) reductions in the proportion of premiums ceded to reinsurers (note: this has already decreased in the past 12 months from 75% to 70%).

Margins

Gross margins have been temporarily inflated because of the change in revenue recognition from Q3 2020 onwards and have been quite lumpy over the past two years, ranging from 8% (Q1 2021; due to the Texas Freeze) to 41% (Q3 2020). CEO Daniel Schreiber has forecasted long-term gross margins of between 20-30%, which I think is a realistic estimate and consistent with Hippo’s long-term gross margin forecasts. Nonetheless, with gross margins in this range, Lemonade is reliant on large volumes to drive profit growth.

As is the fashion with most early-stage technology companies, Lemonade is not profitable, reporting a whopping net loss of 55.6m on 28.2m of revenue in Q2 2021. Although this is a large net loss, I am not overly worried at this stage of their journey given their strong net cash position (see below). The opportunity for Lemonade is enormous and it makes sense for them to continue to invest aggressively to grow their market share in the US, launch new products, expand into new geographies, and improve their customer experience. Given the potential lifetime value of a customer acquired in their 20s or 30s, it is worth spending up to acquire and retain these customers now. Nonetheless, I will be monitoring these net losses and expect Lemonade to demonstrate some operating leverage over the next 2-3 years.

CEO Daniel Schreiber also noted on their Q2 earnings call that he does not expect Lemonade to be cash flow positive for another 2-3 years as he wants to prioritise long-term value creation over short-term profitability. At this stage, I’m comfortable giving Daniel the benefit of the doubt given his track record of under-promising and over-delivering, and significant ownership stake.

Net cash position

As at Q2 2021, Lemonade has a fortress balance sheet with 1.2 billion (USD) in cash and no debt after their IPO and a secondary stock offering in January 2021. CEO Daniel Schreiber noted on their Q2 earnings call that their current cash balance should get Lemonade through to becoming cash flow positive, so I would be surprised (and disappointed) to see significant shareholder dilution from here.

Management and corporate culture

Lemonade boasts a strong management team with high levels of inside ownership, including almost 10% combined ownership between the two co-founders. Below I introduce some of the key players:

Daniel Schreiber (co-founder, CEO, and chairman of the board) appears to be an articulate, principled, and visionary leader who thinks in decades over quarters. It is well worth listening/watching some of his podcast appearances to see what I mean (start here and here). I have watched more than 10 hours of his interviews and media appearances, and become more confident in Lemonade’s ability to execute on their mission each time I hear him speak. Prior to Lemonade, he served in senior executive roles at a number of technology companies (e.g., Powermat Technologies, SanDisk, and M-Systems) and co-founded an internet security software business (Alchemedia) which was acquired by Finjan Software in 2003. He owns 4.4% of outstanding shares and has an excellent 4.5/5 rating on Glassdoor with a 94% approval rating.

Shai Wininger (co-founder and COO) has previously founded four companies, the most notable of which was the online freelance marketplace, Fiverr, which went public in June 2019, has a market cap of 6.5 billion (USD), and is up more than 460% since IPO. He owns 5.5% of outstanding shares.

Tim Bixby (CFO) previously served as CFO of Shutterstock from 2011-2015 and has an MBA from Harvard. I would highly recommend listening to this interview where he explains Lemonade’s business model in a tremendous amount of depth. He owns less than 1% of outstanding shares, so not a lot of skin in the game (at least relative to Daniel and Shai!).

Dan Ariely was a founding team member at Lemonade and served as Chief Behavioural Officer. He is renowned for his research on behavioural biases (you might have heard of his book Predictably Irrational), building upon the established work of Daniel Kahneman (see below image) and Amos Tversky which formed the basis for Thinking Fast and Slow. Ariely was tasked with designing an incentive system where Lemonade could build trust with their customers, and was instrumental in Lemonade’s decision to register as a PBC and Certified B Corp, and institute their giveback program.

In addition to Dan Ariely, it appears that Daniel Kahneman — who won a Nobel Prize in Economic Sciences in 2002 — was also informally involved in the founding of Lemonade. While it is unlikely that Kahneman or Ariely played major roles in day-to-day business operations, I find it reassuring that Lemonade sought out the two most foremost experts on behavioural economics in the early stages of Lemonade to help design their user experience.

Riding on the shoulders of giants

I won’t dwell too much on this point, but it is worth mentioning that Lemonade has some impressive investors on their cap table, including Google Ventures and Sequoia Capital Israel who were both involved in their Series B. Their Series C involved follow-on investments from Google Ventures and Sequoia Capital Israel (always a good sign) as well as investments from SoftBank (who currently owns 19.5% of outstanding shares) and Allianz (a larger European competitor to Lemonade). Their Series D involved follow-on investments from Softbank, Google Ventures, and Allianz.

Valuation (as at 10th October 2021)

Since January 2021, Lemonade has suffered a more than an 80% contraction in valuation multiple (see below chart). Even at current levels, Lemonade trades on a forward EV/sales multiple of around 20x, which is well above that of their larger competitors who generally trade on low single-digit EV/sales multiples. Of course, Lemonade demands a higher multiple than incumbents due to their much higher growth rates, their technology advantage, and the fact that they are still very early in their growth curve (for context, most of their legacy competitors were founded before 1950). The question for investors is whether Lemonade can generate attractive returns from the current price? Let’s look at a few indicators below.

Market cap

One simple approach to valuation (popularised by David Gardner) is to look at the current market cap of a business and consider whether it could realistically become much larger over time. Using this framework, there are more than 50 public insurance companies with a market cap of over 10 billion (USD), as at 10th October 2021 (source). If Lemonade was able to break into this top 50 list (they currently sit at 71st), investors would achieve a more than 2.5x return on invested capital at the current price. While simplistic, this seems achievable over the next 5-10 years.

Estimation of future revenues and EV/sales multiple

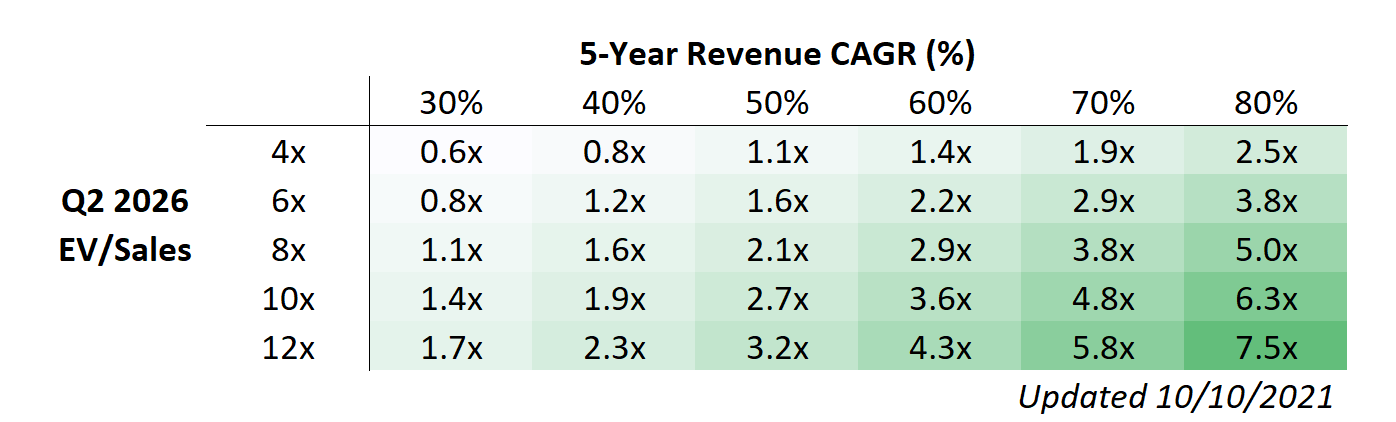

Lemonade is an early-stage, unprofitable business with lots of optionality to expand into new products and geographies. If investors evaluating Lemonade at IPO attempted to forecast future premiums, revenues, and cash flows, they would have been relying on available data from two products: renters and homeowners insurance. This same investor in late 2021 would now also need to consider future contributions from pet, term life, and car insurance. The point here is that so much can change with early-stage technology businesses, so I am wary of overly precise valuation models based on historical data. Instead, I have presented a table presenting returns on initial investment from the current price under a range of (1) 5-year revenue CAGR and (2) exit EV/sales multiple assumptions.

The range of Q2 2026 EV/sales assumptions imply at the lower end (4x EV/sales) additional multiple compression of around 90% from the current multiple as at Q2 2021 (40x EV/TTM revenue) and further multiple compression of around 70% at the higher end (12x EV/sales). Keep in mind that this follows a compression in multiple of more than 80% since January 2021. As with all my valuation work, I have attempted to be conservative so that any multiple expansion from the current price offers pure upside to these forecasts.

Let’s conservatively assume that Lemonade grows revenues at a CAGR of 40% over the next 5 years (20 quarters) and trades on an EV/TTM sales multiple of 6x at Q2 2026. This assumes a dramatic deceleration from their prior 3-year revenue CAGR of 92% and significant multiple compression from the current price. Under these assumptions, Lemonade returns a 1.2x return on initial investment, representing an IRR of 4%.

If we assume as a base case that Lemonade grows revenues at a CAGR of 50% and trades on an exit EV/TTM sales multiple of 8x at Q2 2026 (greater than 80% multiple compression from the current valuation), this generates a 2.1x return on initial investment and an IRR of 16%.

If we assume as a aggressive outcome that Lemonade grows revenues at a CAGR of 60% and trades on an exit EV/TTM sales multiple of 12x at Q2 2026 (70% multiple compression from the current valuation), this generates a 4.3x return on initial investment and an IRR of 34%.

While this is inherently more of a qualitative than quantitative thesis, the above valuation calculations suggest that Lemonade is still attractively priced given their future growth and optionality.

Thesis

To summarise this 9,000 word article as simply as possible, the thesis for Lemonade is as follows:

Insurance is one of the largest and most fragmented industries in the US;

Lemonade offers a much simpler and more frictionless customer experience than competitors;

Lemonade has a large technology advantage over incumbents and benefits from counter-positioning, which makes it very difficult for larger and more resourced competitors to replicate their business model;

Lemonade targets a much younger customer demographic than incumbents which helps to circumvent switching costs and will allow them to generate decades of recurring revenue if they can develop brand loyalty with these customers;

Lemonade has the highest product reviews of all US insurance businesses, averaged across multiple websites;

Lemonade has four routes to grow revenues and premiums: (1) adding new customers, (2) existing customers spending more over time on Lemonade insurance products, (3) adding new insurance products (e.g., car insurance), and/or (4) expanding their coverage of products within the US and in overseas markets. Lemonade is making significant progress on all four fronts;

The proportion of premiums ceded to reinsurance should decrease over time as their total in force premium becomes more diversified across products and geographies;

Lemonade has experienced rapid organic growth in all key business metrics since inception and shows limited evidence of decelerating growth;

Lemonade has experienced an 80% multiple compression since January 2021 and modelling suggests attractive IRRs over the next 5 years, even with conservative revenue and exit EV/sales multiple estimates; and

Founder-led business with high inside ownership (the two co-founders together own around 10% of outstanding shares).

However, there are a number of risks to this thesis which must be considered:

Lemonade is not the only disruptive insurance company in the US. There are a number of other technology-focused competitors founded since 2014, such as Hippo, Metromile, and Root Insurance, who might have informational advantages for specific insurance products;

Possible execution risk from Lemonade expanding too quickly into different product lines;

Lemonade’s AI and machine learning capabilities are overstated and loss ratios do not continue declining over time;

Either of the co-founders resign from the business or sell a significant amount of shares;

Multiple tail events result in catastrophic losses for Lemonade; and

Lemonade is unable to become cash flow positive and is forced to engage in a dilutive capital raisings to fund future growth strategies.

Lemonade is an exciting business firing on all cylinders with an ambitious goal to disrupt the US insurance market. Leveraging the power of technology and a business model informed by collaborations with world-leading behavioural economists, Lemonade reached 1 million paying customers in a fraction of the time of their larger competitors, and have experienced explosive growth in premiums and revenues. They have a long runway for growth ahead of them both within the US and an international markets, and boast a founder-led management team with high levels of inside ownership.

Overall, Lemonade ticks a lot of boxes for a secular growth compounder, but is clearly at the higher end of the risk spectrum for public market investors. I initiated a position in April 2021 at around $90 per share and have continued to average down over the past few months as shares have traded between $60-75 per share. I plan to continue to add to the position if management is able to execute on the above thesis and am comfortable averaging up as I gain greater clarity around Lemonade’s perceived competitive advantages over both their incumbent and new-age competitors.

Best,

Jordan Martenstyn

Sick article! Could definitely see myself being absorbed into the Lemonade ecosystem with renters, pet and car insurance all in one...