Kaspi: A High-Quality Technology Business Trading on a Dirt Cheap Multiple

I'm back! In this article, I dig into Kaspi, the largest technology business in Kazakhstan growing 20%+ with 40%+ net income margins, trading at 7x forward P/E. I bought shares earlier this month.

Introduction

Kaspi (NASDAQ:KSPI) is the largest technology business in Kazakhstan with a market cap of US$18.8b, trailing 12-month (TTM) revenue of US$4.9b (growing 38% YoY), and 41% TTM net income margins.

Kaspi has built a 'super-app' that incorporates mobile payments, e-commerce and classifieds marketplaces (general goods, groceries, cars, etc), banking and financial services, and an online travel agency. Kaspi's diversified super-app is a combination of well established businesses like Amazon (NASDAQ:AMZN), Alibaba (NYSE:BABA), PayPal (NASDAQ:PYPL), Block (NYSE:SQ), and Booking.com (NASDAQ:BKNG), but hyper-localised for the Kazakhstan market.

Kaspi first listed on the London Stock Exchange in 2020 but transferred their listing to the NASDAQ in January 2024 for greater exposure and investor coverage. Shares are up modestly from their 2020 listing price but broadly flat over the past 12 months.

Business Description

Kaspi has three core segments, with net income split roughly even across all segments, offering broad sector diversification.

1) Payments

Kaspi has built a complete end-to-end payments network that enables customers to pay bills, make online and in-store purchases, and facilitates peer-to-peer (P2P) payments. Via Kaspi’s network, customers can make payments both within Kazakhstan and globally to any Mastercard or Visa card. Kaspi also offers a PoS device to help merchants accept payments, similar to Block (NYSE:SQ).

Kaspi primarily generates payments revenue from transaction fees related to the total payment volume (TPV) flowing through their network. Take rate in recent quarters has been around 1.2%.

As of Q3 2024, Kaspi's payments business had 13.4m active customers, out of a Kazakhstan population of 20.7m (65% penetration within Kazakhstan).

The payments segment is growing strongly (+25% in Q3 2024) with astonishing 66% net income margins and contributes the most net income for Kaspi (37% of Q3 2024 net income).

2) Marketplace

Kaspi also boasts a thriving marketplace business, consisting of largely a 3P e-commerce marketplace (including real estate and car classifieds portals) but also a fast-growing 1P marketplace for purchasing groceries. Around 40% of e-commerce deliveries are made to Kaspi out of home lockers.

Similar to other e-commerce companies, Kaspi generates revenue from seller fees and takes a small clip of all the marketplace transactions (or GMV) that occur on their platform. Kaspi's blended marketplace take rate was 9.5% in Q3 2024, which is well below other established e-commerce marketplaces like Etsy (NASDAQ:ETSY) and eBay (NASDAQ:EBAY). Over time, I would expect Kaspi to flex some pricing power and increase their take rate to the 15-20% range to be more consistent with large marketplace competitors.

In Q3 2024, Kaspi had 7.8m active marketplace customers. Revenue growth was very strong (+43% YoY) with 47% net income margins. Kaspi's 1P marketplace segment (e.g., online groceries) has lower margins than their core 3P marketplace business, so net income margins will likely reduce over time in this segment as 1P revenue growth continues to grow strongly.

3) Fintech

Kaspi also offers a range of financial services, including consumer and corporate banking, and a range of loan products, such as buy now pay later, SME loans, and car loans. Financial services are offered online but also in some branches; their main competitors are traditional banks and financial institutions within Kazakhstan that are heavily reliant on physical in-person branches.

The main drivers of revenue for the fintech segment are the value of outstanding loans and associated interest rates.

In Q3 2024, Kaspi had 5.5m active fintech customers and 6.4m customers with outstanding loans. Revenue growth was 24% YoY with net income margins of 27%.

Core metrics related to defaults, loss rates, and delinquency rates have remained very low in recent quarters.

Financial Summary of Segments

Financials

Kaspi has a very attractive financial profile with strong revenue growth and world-class margins. If we use the classic Rule of 40 metric (revenue growth rate + EBITDA margins), Kaspi scores around 80 in recent quarters, which is in the top 1% of public companies I have studied. For some context, investors generally look favourably on companies generating a Rule of 40 score above 40 (hence the name).

Revenue

Revenue has compounded at around a 40% CAGR over the past 2 years with TTM revenue growth of 38% (in USD). Last quarter revenue growth was 29%.

All segments are growing strongly (payments and fintech in the mid-20s, marketplace in the low 40s), driven partially by new customer growth but primarily increasing engagement amongst existing customers.

While Kaspi already has very high penetration within the Kazakhstan market, there are multiple levers to continue growing revenue in the 15-20% range for the foreseeable future:

Population growth within Kazakhstan (grown 1-2% annually for the past decade)

Increasing GDP per capita in Kazakhstan (contingent largely on oil prices, so could reverse)

Continued digitisation within Kazakhstan (driven by Kaspi, cashless payments have rapidly increased from 13% of TPV in 2016 to 86% in 2023 but e-commerce rates of roughly 14.5% remain below that of the USA at 16% and China at 47%)

Price increases on existing services (particularly if inflation increases)

Launch and scaling of new products

Expansion into new overseas markets (e.g., Turkey)

All of the above factors provide solid tailwinds for Kaspi.

Profitability

Kaspi is a highly profitable business with some of the highest margins I have seen in public markets. Net income margin has consistently exceeded 40% in recent quarters (41% in Q3 2024) while EBITDA margin has consistently been above 50%.

Margins are strong across all segments and have remained strong over the past two years. There has been some compression in marketplace margins due to increasing contribution from newer 1P marketplace services (e.g., online grocery delivery) which are inherently lower margin than their core 3P marketplace and will take time to scale.

What accounts for such strong margins? Kaspi has a dominant market position across all their core segments with high rates of repeat usage and strong organic brand recognition. As such, customer acquisition costs are low and unit economics are very strong. Moreover, as Kaspi has largely built out their core payments and marketplace technology infrastructure, which are inherently high margin businesses at scale, incremental profits for new customers are very high.

Kaspi Investment Thesis

My thesis for Kaspi is relatively simple and is outlined below.

1) Dominant Market Share (Scale Economies)

A core focus of my investment philosophy is looking for market leaders operating in attractive growth industries with high barriers to entry and/or achieving scale. Kaspi meets all of these criteria.

Based on public filings and recent interviews with the CEO, Kaspi is the market leader in Kazakhstan across most of their five core market segments. Below are some stats which indicate Kaspi's market dominance:

As seen above, Kaspi has a strong market position across all segments, affording them solid pricing power. Scale also allows Kaspi to distribute their marketing and R&D spend across their entire suite of products and customer base, which puts them at a distinct advantage vs. smaller single-line competitors with less scale.

Moreover, Kaspi's business segments are all relatively difficult to scale. While any founder could theoretically raise $1b from SoftBank or Tiger Global to compete with Kaspi (which seems highly unlikely as they would want to target a bigger initial market than Kazakhstan), such an upstart would struggle to:

Replicate Kaspi’s technological infrastructure with their payments and marketplace networks

Displace existing customers who are habitual users of Kaspi

Disrupt the customer goodwill and brand recognition of Kaspi

Gain sufficient market share (before going bankrupt) to achieve the same level of profitability as Kaspi who can spread customer acquisition and R&D spend across their large customer base and range of services

Overall, while Kaspi is not immune from competition, their dominant market position and relatively weak competition (at least vs. more competitive markets like the USA or Europe) should protect Kaspi for the medium-to-long term.

2) Very Strong Brand and Customer Engagement

Kaspi has astonishing engagement metrics that rival any global super-app (perhaps with the exception of WeChat in China). At the time of this article, Kazakhstan has a population of around 20.7m people, of which:

14.4m are monthly active users (70% of the national population)

Almost 10m daily active users (DAU:MAU ratio of 67% which is very high; for context, Duolingo's DAU:MAU ratio is 33%)

The average customer uses Kaspi 72 times per month (about 2.5 times per day) and this number has been steadily increasing over time

Customer NPS was 87 at time of their London IPO in 2020 (note: I have not seen a more recent number), which is world-class

Online customer reviews appear very strong, which is supported by the above engagement metrics. This is a sticky business with a national brand that is ingrained in the daily lives of Kazakhs. This brand recognition and loyalty is incredibly difficult for any competitor to disrupt.

3) Self-Reinforcing Customer Flywheel (Network Effects)

Kaspi offers a range of interrelated services where growth in one segment reinforces growth in other segments, a benefit other single-product competitors do not have. For example:

A customer purchases an item from Kaspi’s e-commerce platform (leads to marketplace revenue)

Each e-commerce transaction is processed via Kaspi’s payment network (leads to payments revenue)

Kaspi has access to that transaction data (which other banks and retailers do not have), which increases their data advantage and helps them build a more detailed customer profile for future lending decisions and ad targeting

With this data, Kaspi is able to better personalise ads and assess credit worthiness, resulting in more relevant ads and more effect credit decisions (leads to advertising and fintech revenue)

These customers then have more to spend on Kaspi's marketplace, with lower default rates

Another source of network effects is the high adoption of P2P payments within Kazakhstan - if all of one's friends and colleagues use Kaspi for P2P transfers, it becomes much easier to opt into that network than use a competitor.

Such network effects are unique to Kaspi in the Kazakhstan market due to their enormous scale and bundled super-app strategy.

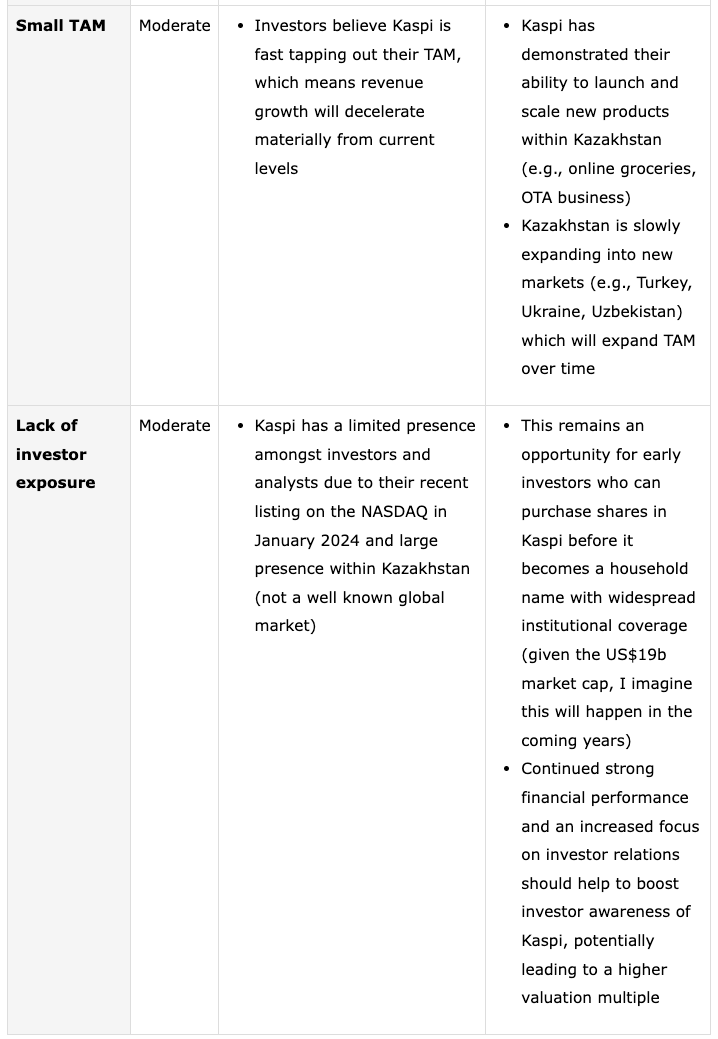

4) Track-Record of Successfully Scaling New Services

One of the main initial concerns I had about Kaspi was that their total addressable market (TAM) was too small, being almost exclusively based in Kazakstan with a population of only 20.7m.

There are two primary ways a company can increase their TAM:

Launch additional products and services

Expand into new markets

Kaspi has a demonstrated track-record of launching (often via tuck-in acquisitions) and scaling new services that serve customers into market leaders within Kazakhstan, which helps to alleviate some concerns about TAM.

Online Travel Agency

In December 2020, Kaspi launched an online travel agency (OTA) business, beginning with a simple offering allowing customers to book domestic and international flights. Over time, Kaspi expanded into train tickets and also whole trip travel packages. In just four years, Kaspi’s OTA business has quickly grown to become the largest in Kazakhstan.

Online Groceries

In 2022, Kaspi acquired 90% of an e-commerce business in Kazakhstan which formed the foundation for their online grocery business. In just two years, Kaspi has quickly grown this segment to become the largest e-grocery business in Kazakhstan, with 725,000 customers. GMV growth remains very strong at 88% in Q3 2024 and the business is profitable, with a long runway ahead of them to take sure from incumbent in-person grocery businesses.

Online Classifieds

In August 2023, Kaspi acquired a 40% stake in Kazakhstan’s leading online classifieds business (Krisha.kz) which has the leading national real estate and automotive platform, as well as a generalist marketplace site. Over time, Kaspi appears to have increased this stake past 50% to gain control of the business. This segment is very new but management are very bullish on its growth potential (particularly the automotive classifieds business).

B2B Fintech Services

To date, Kaspi has focused their fintech offering on consumers, but is expanding more in recent quarters to B2B services. Kaspi launched business deposit accounts for merchants in mid-August 2024 and reached 41,000 customers by the end of Q3 2024. Their B2B payments segment is growing very quickly with a long growth runway:

Kaspi B2B Payments is the fastest-growing component of our TPV and during 9M 2024, accounted for 5% of TPV. We expect B2B Payments to continue growing significantly faster than Payments TPV. (Kaspi Q3 2024 Earnings Release)

Other Services

There are a range of other potential services Kaspi can monetise over time, including:

Advertising on their e-commerce platform (recently launched)

Digital gift cards that can be used on Kaspi's marketplace (launched in Q3 2024)

Cloud infrastructure services (author speculated potential future service)

Subscription offering like Amazon Prime or Coupang WOW (NYSE:CPNG) (author speculated potential future service)

5) Promising International Expansion Opportunities

Expanding into new overseas markets is arguably an even bigger lever for Kaspi to expand TAM than new products. The CEO has a clear goal of reaching 100m consumers in the long-term, up from 14m in their latest quarter.

The CEO is laser focused on international expansion into Eastern Europe and Asia. I expect their focus will be on markets where traditional e-commerce and payments incumbents (e.g., Amazon, PayPal, Alibaba, MercadoLibre) do not have dominant market positions, leaving the door open for a new entrant like Kaspi.

“For a long time, we have said investing in our growth including international expansion is our top priority” (Kaspi Q3 2024 Earnings Release)

The game plan for Kaspi appears to be to gain an initial foothold and regulatory compliance via tuck-in acquisitions and then invest in organic expansion within that market. Below is a short breakdown of Kaspi's recent international expansion efforts.

Ukraine

In October 2021, Kaspi acquired 100% of Portmone Group (purchase price unknown), a payments business based in Ukraine to enter the Ukraine market (37m population). Clearly with hindsight of the Russia-Ukraine war, this acquisition was premature and Ukraine currently accounts for less than 1% of consolidated revenue and is therefore immaterial to Kaspi. Perhaps when the war is over, this will become a more material growth driver for Kaspi.

Uzbekistan

In mid-2024, Kaspi submitted a non-binding letter of interest to participate in the privatisation of Humo, one of the two core payments networks in Uzbekistan (36m population). While Kaspi withdrew their formal interest in November 2024, this move showed their desire to expand to the Uzbekistan market.

Turkey

In October 2024, Kaspi acquired 65% of NASDAQ-listed Hepsiburada (NASDAQ:HEPS), a Turkish e-commerce business that serves over 12m consumers and 101,000 merchants. This transaction cost US$1.2b and was financed from Kaspi's existing cash flow with the potential for some debt financing. The transaction is expected to close in Q1 2025.

Below is a brief rationale for the deal as mentioned in Kaspi’s Q3 2024 earnings release:

“Serving 12 million consumers and 101 thousand merchants, we believe Hepsiburada is a strong cultural fit with Kaspi.kz given its innovative culture, focus on providing high quality services to consumers and merchants and commitment to long-term sustainable growth. Like Kaspi.kz, Hepsiburada is a highly entrepreneurial company and home-grown eCommerce champion, built by a visionary founder. Both companies are driven by a similar purpose, namely to improve consumers’ and merchants’ lives.”

This acquisition expands Kaspi’s TAM to also include the 85m people who live in Turkey (more than 4x the population of Kazakhstan), whilst materially increasing Kaspi’s base of GMV, customers, and merchants at a much cheaper valuation than their own listing. Over time, I would expect Kaspi to cross-sell their other services to the Turkish market, looking to replicate their network effects within Kazakhstan in Turkey.

It is still early days of Kaspi's venture into the Turkish market, but my gut feel tells me this could be a highly accretive acquisition. I would expect more insight into Kaspi's strategy for Hepsiburada in their upcoming Q4 2024 earnings release.

6) Visionary CEO, High Inside Ownership

Mikheil Lomtadze (CEO)

Kaspi is led by CEO, Mikheil Lomtadze, who I do not believe is technically a founder, but joined Kaspi in 2007 to run the business during the GFC (it was previously a commercial bank). I think after a tenure of 17 years, Mikheil is a quasi-founder and certainly exhibits many of the hallmark traits of a world-class founder.

In preparation for this article, I listened to all public interviews with Mikheil. With every incremental interview, my conviction in Mikheil as a leader increased - he is highly intelligent, ambitious, obsessed with the customer experience, and data-driven. This is not a person I would want to bet against.

From 1995 to 2000, he founded and built GCG Audit, a strategy consulting and audit firm which later became part of the Ernst & Young network in Georgia. He then became only the second person from Georgia (the country) to attend Harvard Business School and shortly after became a partner at a private equity firm, Baring Vostok Capital Partners, where he reportedly rose through the ranks to became a partner within 12 months. While working at Baring, Mikheil was involved in their investment in Kaspi, which led to him subsequently joining as CEO.

Inside Ownership

A core factor I look for with all potential investments is high inside ownership. Kaspi has the highest inside ownership I can remember seeing in a long time. Mikhail (CEO) owns 23% of the company, closely followed by the Chairman (Vyacheslav Kim) who owns 21%. Baring Funds (the PE investor) owns 25% of the company - typically, private equity firms sell down their stake once a company goes public, so the fact that Baring remains a long-term holder is unique and a very bullish sign.

All in all, insiders own an astonishing 73% of the company, which is about a strong a signal that insiders are bullish on Kaspi’s future prospects.

7) Strong Company Culture and Ability to Attract Talent

I won't dwell much on this point, but it's worth a quick mention. Given their scale, Kaspi appears to have become one of the most sought after employers in Kazakhstan with a 2% graduate acceptance rate and strong Glassdoor reviews (4.2/5 from 91 reviews). Kaspi appears to be a crown jewel in the Kazakhstan technology ecosystem and I can imagine that the smartest, most ambitious and hardest working graduates in Kazakhstan (who do not emigrate to a larger country like the US) would be applying for jobs at Kaspi. This intangible 'culture' or 'talent' factor is hard to quantify, but is material.

Valuation

It is hard to argue that Kaspi is an expensive stock. Investors might have concerns about geopolitical or other risks, but I doubt any investors are passing on Kaspi due to valuation alone.

Kaspi trades on a forward P/E ratio of roughly 7x and has the cheapest multiple of a broad basket of global e-commerce and payments businesses I track (includes those operating in frontier markets like China, South America, and South East Asia). Of note that includes Chinese e-commerce businesses like Alibaba (NYSE:BABA) and JD.com (NASDAQ:JD), which have been in the dog house with investors for a long time.

Despite this low relative valuation vs. comps, Kaspi has one of the stronger revenue growth rates (40% 2-year CAGR) and easily the highest net income margins. In simple terms, Kaspi is cheap, growing fast, and highly profitable on any measure.

Any quick back of the envelope maths indicates that Kaspi can generate attractive shareholder returns from the current valuation. In this section below, I present a simplified valuation analysis that does not include any contribution from dividends or buybacks to be conservative. While returns in the base and upside case are very strong, I caution investors from being too attached to specific scenarios and focusing more on the big picture calls that need to go right to make money in Kaspi, namely:

Can Kaspi continue growing for the foreseeable future in the double digits?

Can Kaspi avoid substantial margin compression?

Can Kaspi maintain their competitive position in Kazakhstan?

Will Kaspi be successful in launching new services and/or expanding into new geographies?

Will Kazakhstan avoid being dragged into major geopolitical conflict?

Can the Kazakhstan economy avoid major hyperinflation?

Valuation Scenario Breakdown

Bear case - I've tried to be quite conservative, assuming revenue growth decelerates significantly to a 10% CAGR over the next three years (vs. 40% 2-year historical CAGR), net income margins of only 20% (vs. 41% currently), and exit at TTM P/E ratio of 10x (in line with current levels). Under this bearish scenario, investors lose about 1/3 of their capital. Not a good outcome, but a low probability.

Base case - I've assumed revenue growth still decelerates to a 20% CAGR, net income margin contracts to 30%, and business exits for a 15x P/E multiple. In this scenario, IRR is a very healthy 25%.

Upside case - I've assumed revenue growth rates remain broadly stable at 30%, Kaspi maintains net income margins at 40%, and there is notable P/E multiple expansion to 20x (possible if the geopolitical storm clouds begin to dissipate and Kaspi continues to execute). Under this upside case, investors generate a very strong 64% IRR.

Given the relative balance of probabilities and very strong expected returns in the base and upside scenarios, I am happy to take a starter position in Kaspi and monitor the ongoing risks.

Why is Kaspi so Cheap?

At a 7x forward P/E multiple, 'Mr Market' is clearly giving a strong signal with Kaspi. By my estimation, I believe Kaspi's low multiple is due to the following four factors. Some of these risks are elaborated later in this article.

While there are genuine risks with Kaspi (particularly geopolitical), I believe the low current valuation, quality of business model, and quality of the CEO more than compensates investors for these risks.

Risk Factors

I’ve identified three core risk factors for Kaspi. Unlike my other portfolio holdings, none of these risks relate to the quality or defensibility of Kaspi’s core business or competitive position, but rather relate to broader external factors.

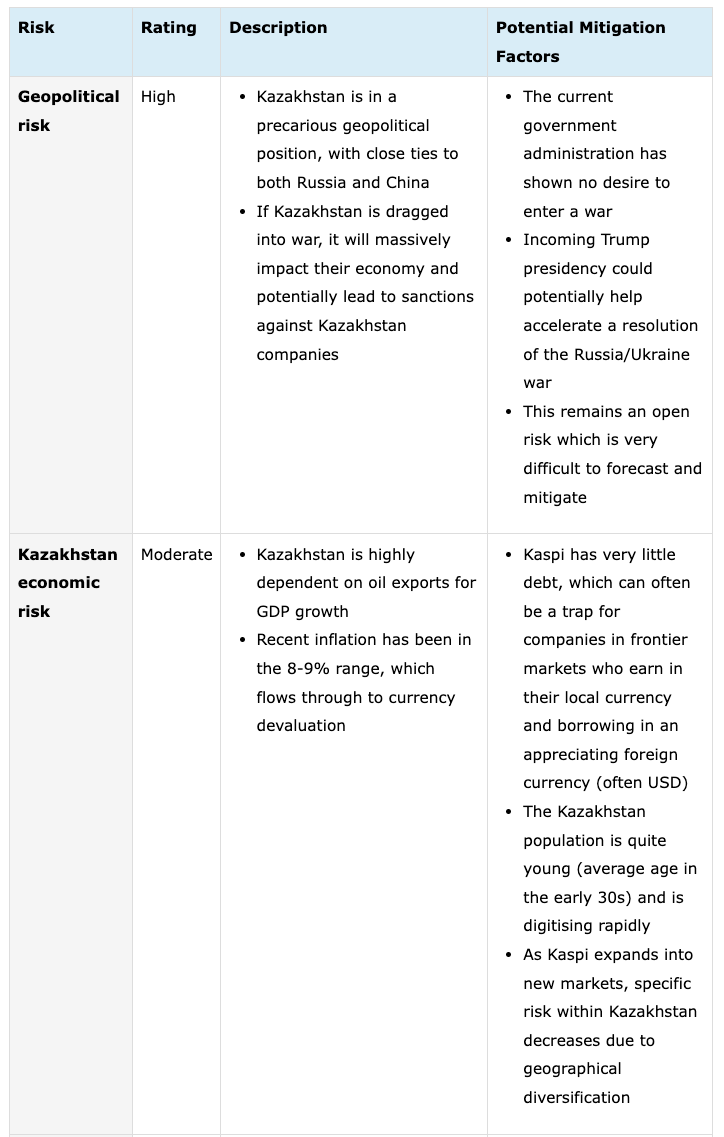

1) Kazakhstan Economic/Currency Weakness

Kazakhstan is an interesting market. It is the 9th largest country in the world by land mass and closely borders Russia and China, placing it in a precarious geopolitical position. With a population of 20.7 million, it has the 53rd highest GDP globally and the 57th highest GDP per capita. Of note is that Kazakhstan’s GDP per capita is higher than Argentina, Chile, Mexico, China, and Brazil.

As an economy, Kazakhstan is highly dependent on oil exports, similar to other countries in this region. It is also the world’s largest producer of uranium. Their largest export partner is China, while Russia is their largest importer. With a high dependence on resources and China/Russia, Kazakhstan has a much more unpredictable economic path over the next decade than established Western countries.

In 2023, GDP growth was just over 5% while inflation has sat around the 8-9% range in recent quarters, resulting in GDP contraction in inflation-adjusted terms. Growth could accelerate in line with changes in the oil and uranium markets, but could also realistically decelerate or decline, which would impact consumer spending and delinquency rates.

Currency weakness remains a very real threat for investors and, in my opinion, explains a notable portion of the low multiple.

2) Geopolitical Risk

Another major factor is geopolitical risk, which is the most unpredictable of all risk factors and the hardest to mitigate. Kazakhstan sits in a precarious region, bordering Russia, China, all while being located near Ukraine, which is an active war zone. Any escalation in war, particularly if Kazakhstan somehow becomes involved, will lead to a material slowdown in Kazakhstan’s economy which in turn hurts Kaspi due to their very high exposure (>99% of revenue currently) to the Kazakhstan economy. In a worst case scenario, there could be sanctions of companies based out of Kazakhstan (similar to what happened with Russian companies in 2022/2023).

On the flip side, any resolution with the Russia/Ukraine conflict and/or reduced threat of Chinese involvement with war could lead investors to become more comfortable investing in the region and an inflow of capital. As the largest technology business in the country, Kaspi will undoubtedly benefit from foreign investment.

I'll leave the prediction of complex geopolitical events to the experts, so I will avoid making any forecasts in this article.

3) Negative Government Intervention Risk

In any frontier market, the risk of government interference in corporate actions is elevated (as we have seen with Chinese companies since COVID). However, I am relatively comfortable with this risk for Kaspi because:

Kaspi appears to charge fair prices for consumers, has strong online customer reviews, and very high customer engagement

Kaspi is a large employer in Kazakhstan, particularly for engineers

Kaspi provides a lot of free services for the government and appears to have built strong goodwill - via Kaspi, people living in Kazakhstan can pay their taxes, parking fines, issue birth certificates, and register a business or marriage

These above factors are very hard to replicate for upstart competitors and require substantial time and political investment (of time, not money). In some sense, the Kazakhstan government is dependent on Kaspi for provision of some government services (which they receive for free), so there is little incentive for them to disrupt the status quo and go after Kaspi.

I am not a politician though (and never will be), so treat the above sentiment with a grain of salt.

Conclusion

Kaspi is one of the highest quality and highest margin businesses I’ve come across in public markets, albeit with significant exposure to the volatile Kazakhstan economy. The business has a dominant market position across their payments, fintech, and marketplace segments, and is led by an exceptional CEO who has successfully scaled several new services since COVID into market leaders. With promising adjacent products (e.g., advertising, B2B payments) and promising international expansion plans (largely in Turkey to date), Kaspi has several levers to expand their TAM and support continued strong revenue growth.

Although Kaspi is exposed to material geopolitical and economic risk within Kazakhstan, I believe the current valuation of 7x forward P/E multiple more than compensates investors for the risks.

I've taken a starter position and I encourage investors looking to diversify their portfolio outside of the US to take a look at this under the radar gem in Kazakhstan.

Nice write-up! Thanks!

My understanding after talking to people from Kazakhstan is that without Kaspi life there would suck a lot.

High quality business led by a competent team, trading cheap/reasonably. Terry Smith would approve.

Kazakhstan business environment is more developed than people realize regardless of the “stan” in the end, bordering Russia, being in the neighborhood of Iran and Afghanistan. It sounds more exotic than it is.

How do u like fintech in mid-south America other than Meli? Such as Nu and Intr?