Doctor Care Anywhere: The Fastest Growing Telehealth Company You've Never Heard Of

Doctor Care Anywhere is a UK-based telehealth business founded in 2013 that listed on the ASX in December 2020. Shares have fallen more than 65% in the past 12 months despite outstanding FY21 results.

Doctor Care Anywhere (ASX:DOC) is a UK-based telehealth business founded in 2013 that listed on the ASX in December 2020. Like almost all global telehealth businesses, DOC’s share price has taken a beating over the past 12 months, falling more than 65%. However, this drop in share price does not reflect DOC’s exceptional business performance since IPO, growing revenues greater than 115%. It is rare to find a situation where the share price of a business continues to fall while the business itself continues to execute and report stellar results. DOC represents one of the most striking examples of this uncoupling between business and share price performance I’ve seen since I began investing in late 2016. I continue to average down into the position.

A quick primer on DOC’s business model

Before we delve into DOC’s outstanding FY21 results and attractive valuation, we first need to understand their business model and how they generate revenue. DOC partners with large private health insurers, such as AXA Health and Allianz, to offer telehealth services for their clients. DOC’s services are free for clients who have private health insurance with one of these partners and DOC receives revenue (from the private health insurer) each time an insured customer uses one of their services. The situation is a win-win-win where:

DOC gains access to clients who want to access telehealth services;

The private health insurer is able to offer their customers a high-quality telehealth service, helping them differentiate from competitors; and

The customer gains access to a ‘free’ telehealth service (free in the sense that they do not pay for each consultation, but they still pay for private health insurance).

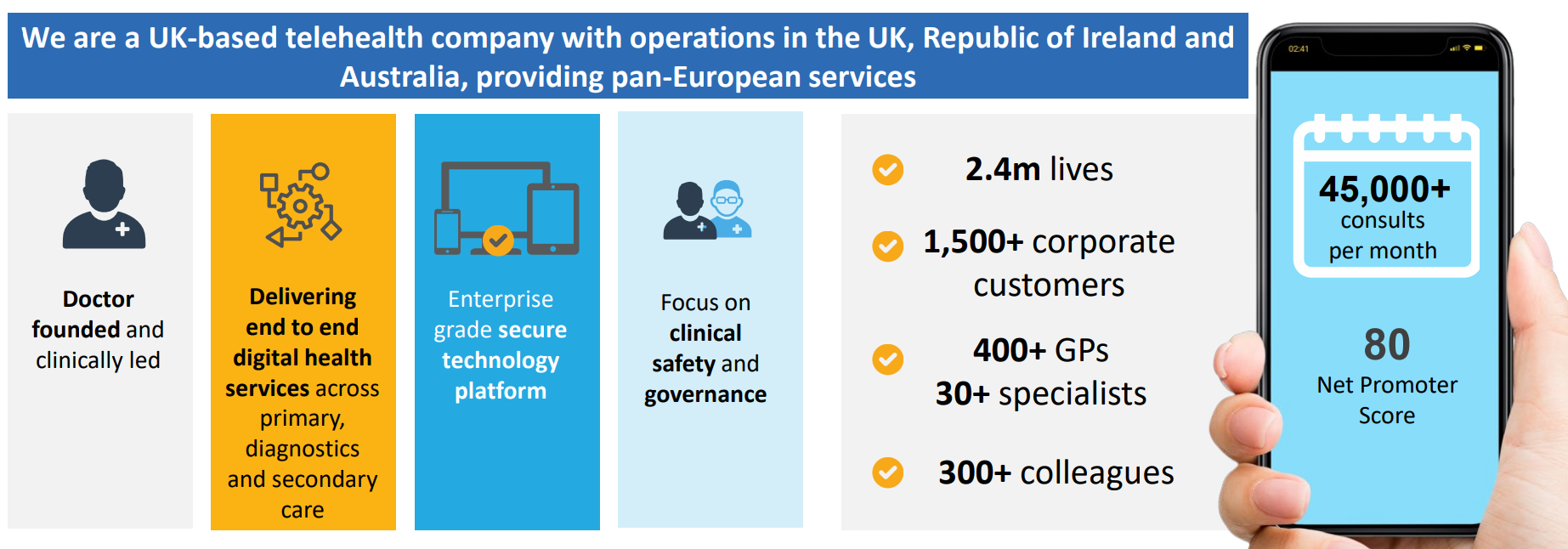

Through these private channel partners, DOC gains access to 2.4m eligible clients who can use their telehealth services. As of Q4 2021, the vast majority of these clients were based in the UK, with smaller amounts in Ireland and Australia.

DOC does not serve clients without public health insurance. These clients can access medical services through the government-funded National Health Service (NHS) in the UK.

DOC is becoming more than a simple telehealth provider

One of the things that first attracted me to DOC (other than their 100%+ revenue growth rates) was management’s push to become a coordinated digital health platform which facilitates: (1) virtual GP or advanced nurse practitioner consultations, (2) referrals for diagnostic tests, and (3) virtual specialist reviews. Rather than being a simple provider of GP consultations (which has become a commoditised business with lots of competition), DOC is positioning themselves as a digital health platform capable of servicing all patients needs with patient electronic medical records stored on the one platform. This approach has a number of benefits for all stakeholders:

DOC is able to generate more revenue and gather patient data, while benefiting from increased efficiencies;

The insurer receives greater cost savings as all medical services can be carried out through DOC’s platform, reducing the need to work with multiple providers; and

Customers are provided with a much faster and more efficient service as all follow-up services are coordinated on DOC’s platform.

Compare the two experiences from the perspective of a patient. This is the future of healthcare.

Now let’s delve into DOC’s recent financial/operational performance, their valuation, and some of the drivers that make me confident that DOC will deliver market-beating returns from the current share price.

1) Long waiting times in the UK NHS increases demand for private alternatives

The UK NHS has an unwanted reputation for poor service and long waiting times, and these concerns have been exacerbated with continued COVID-19 lockdowns in the UK. See the following graphs:

DOC estimates that waiting times in the NHS are 2-3 weeks for a routine GP consultation and three weeks for a standard diagnostic test. Imagine catching a cold, booking a GP appointment, and then only being able to see the GP a fortnight later after you’ve already fully recovered from your cold. This rapid increase in waiting times for medical services is a major driver for people in the UK to seek private health insurance to gain access to time-efficient telehealth services, such as DOC.

2) Rapid organic growth in revenues and consultations

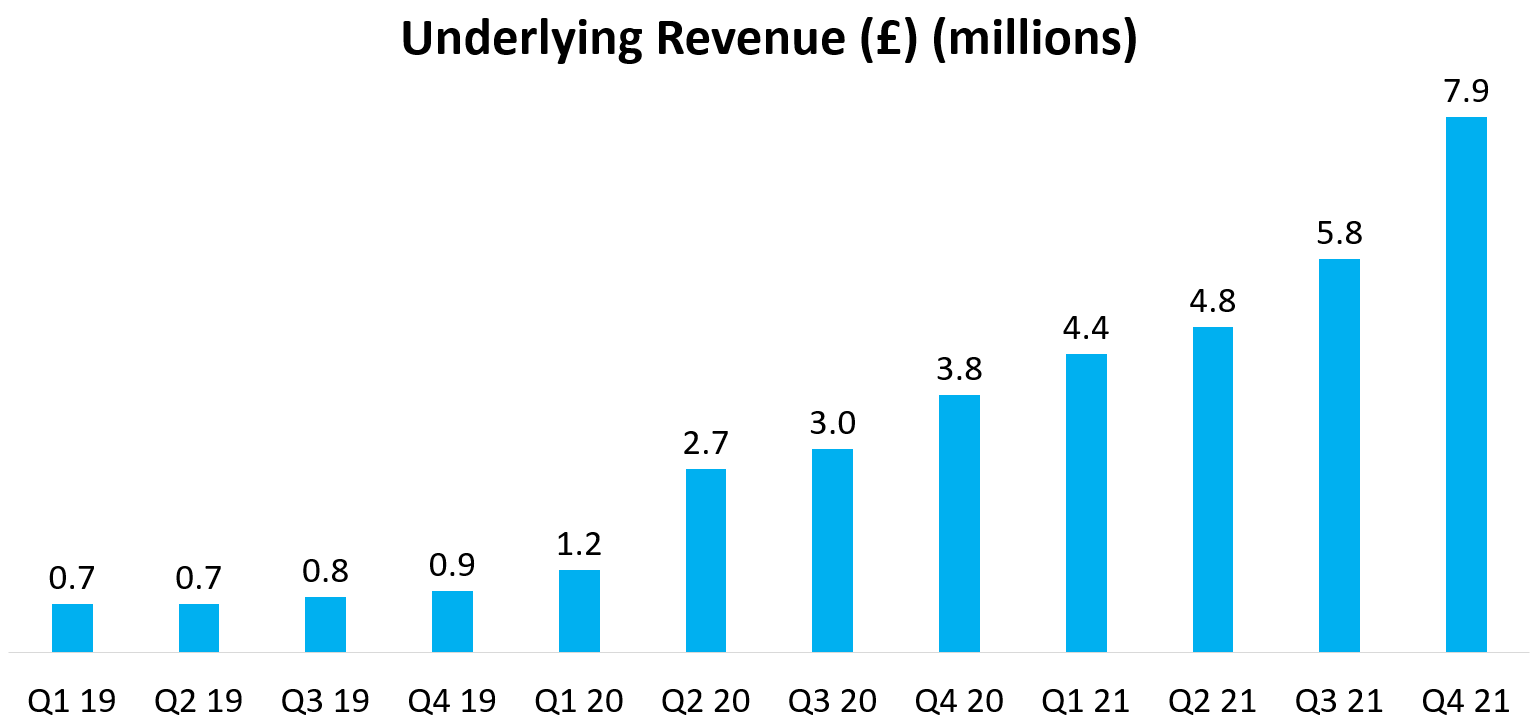

DOC’s core top-line metrics are: (1) revenues and (2) consultations. In 2021, DOC reported total revenues of £25.0m ($46.3m AUD), which represented YoY revenue growth of 116%, well ahead of their guidance for at least 100% YoY revenue growth. One of the main reasons I believe DOC’s share price sold off over the past few months was scepticism that DOC would not be able to meet their 2021 revenue guidance. DOC proved the doubters wrong and produced a fantastic Q4 result, generating £7.9m revenue, which was up +36% QoQ and +108% YoY (when comparing underlying revenues between Q4 2021 and Q4 2020).

Since Q1 2019, DOC has grown underlying revenues (excludes irregular revenue items like technology platform licensing fees and digital design service fees) at a CAGR of 141%, demonstrating the strong demand for their telehealth services. What is more impressive is that almost all of this revenue growth has been organic and achieved without acquisitions.

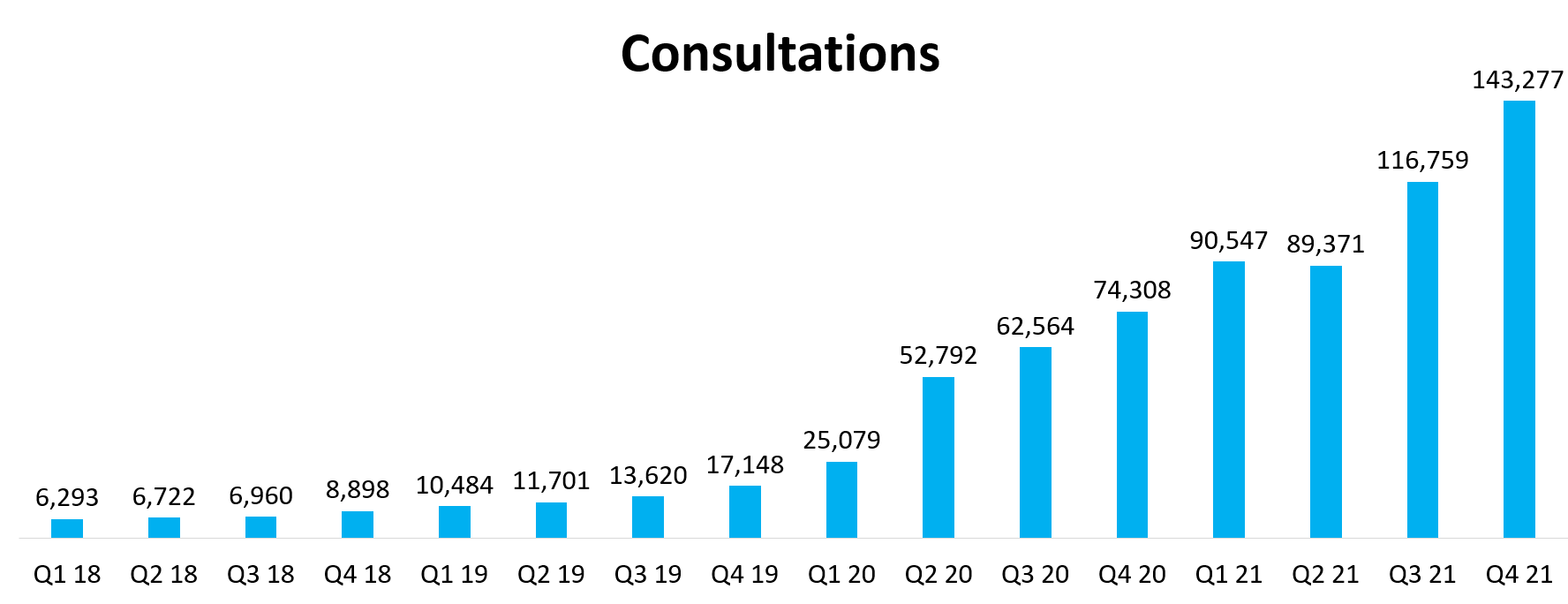

The main driver of revenue growth is an increase in the number of consultations carried out on DOC’s platform, as DOC receives revenue from their private health insurance partners for each completed consultation.

Since Q1 2018, DOC has grown consultations at a phenomenal CAGR of 130% from 6,300 consultations (Q1 2018) to 143,000 consultations (Q4 2021). DOC reported 440,000 consultations in 2021, representing 94% YoY growth, and this includes a QoQ decline from Q1 to Q2 as DOC struggled to onboard and train GPs fast enough to meet the demand for their services after snap lockdowns were introduced in the UK.

3) DOC has lots of room to further convert eligible lives into activated lives

In addition to the number of consultations delivered, the two most important operational metrics for DOC are:

Eligible lives (the total number of people who are eligible to use DOC’s services through their private health insurer); and

Activated lives (the total number of people who create an account and enter their personal details on DOC’s website, demonstrating their ‘activation’ and willingness to use DOC’s services).

DOC has an impressive database of 2.44m eligible lives, which grew 10% YoY in 2021. Growth in eligible lives has trailed growth in revenues and consultations over the past 12 months because (1) more than 80% of DOC’s eligible lives come from their partnership with AXA Health and (2) Nuffield Health and Walgreens Boots Alliances are the two sole channel partners that DOC has added in the past 12 months.

While a relative plateau in the number of eligible lives might concern some investors, I believe growth in activated lives is the far more important metric to watch. To use an analogy of a podcast, I think of eligible lives as the total number of people who have subscribed to a given podcast, while activated lives represents the number of people who listen to podcast episodes on a frequent basis. Both are important, but activated lives is what drives revenue and engagement.

Since Q1 2018, DOC has grown activated lives at a CAGR of 100% from 50,000 (Q1 2018) to 675,000 (Q4 2021). This is a pleasing trend and is indicative of increasing client engagement with DOC’s platform.

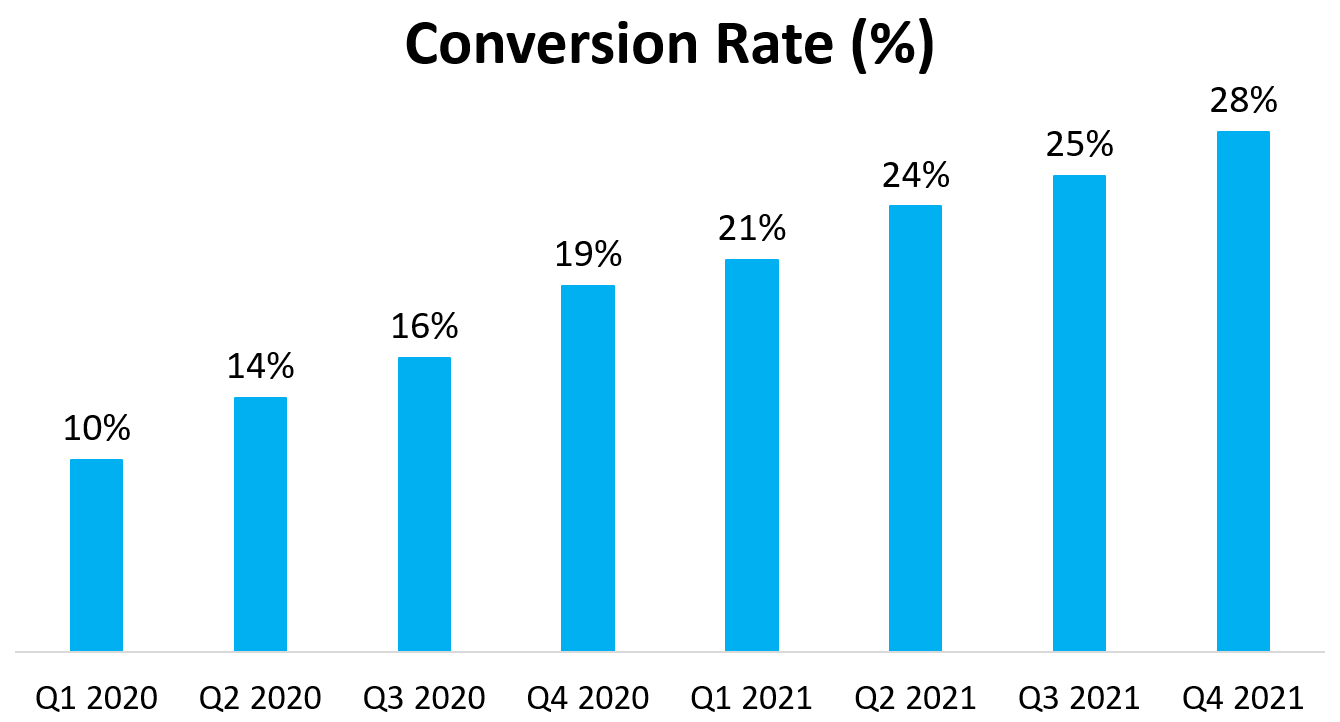

Another important metric to watch is DOC’s conversion rate, which I calculate as the ratio of activated lives to eligible lives. As investors, we want to see this conversion rate increasing over time. Since 2020, this conversion rate has increased QoQ from 10% to 28%, which is a good sign. However, keep in mind that if DOC signs a new large channel partner and gains (overnight) lots of new eligible lives, their conversion rate would decrease as it takes time for DOC to convert these clients into activated lives. So, it is important to understand the context behind these numbers.

DOC CEO Bayju Thakar mentioned on a recent podcast appearance with Jarden that this conversion rate is a lever that DOC can pull to drive demand for their services in a sustainable fashion. For example, if DOC wanted to increase this rate to above 30% next quarter, they could conduct more targeted advertising and switch on push notifications to certain eligible lives through their channel partners. On the other hand, if DOC was forecasting insufficient GP supply ahead of time (e.g., around a holiday period), they could dial down their direct marketing spend in the lead-up to that time to prevent excess demand for their services from new activated lives.

4) DOC is experiencing significant traction within their integrated secondary care pathway

Since management began to position DOC as an integrated digital health platform, rather than as a simple provider of GP consultations, DOC has experienced significant traction within their secondary care referral pathway. The number of patients who engaged in their secondary care pathway (including both diagnostic referrals and specialist review of diagnostic results) has been the following in 2021:

Q1 2021: 2,500 patients.

Q2 2021: 3,300 patients (+32% QoQ growth).

Q3 2021: 5,100 patients (+55% QoQ growth).

Q4 2021: 6,500 patients (+28% QoQ growth).

Seeing consistent 25%+ QoQ growth in the number of patients engaging with their secondary care pathway is very promising as DOC is able to monetize each step of this patient journey. Rather than receiving revenue for a single GP consultation, DOC can now also receive revenue for referring clients to a diagnostic centre and for specialist review, increasing average revenue per user (ARPU) and customer lifetime value (LTV).

5) High percentage of recurring consultations indicates high customer satisfaction

DOC reports solid retention rates for a telehealth business. In 2020, DOC had a 75% repeat user rate, meaning that 75% of patients who attended at least one GP consultation in 2019 booked another appointment in 2020. In both Q3 and Q4 2021, DOC reported that 65% of consultations came from returning patients, demonstrating customer satisfaction with their platform. Not all activated lives will need to see a GP or specialist in a given quarter, so I would expect DOC’s repeat user rate to be > 75% in 2021 and an improvement on the prior corresponding period (note: DOC seems to have stopped reporting this metric).

While these retention figures might seem weak relative to other businesses (e.g., a B2B SaaS business with gross retention figures in the 95%+ range), it is important to note that not all clients will need to see a GP in a given period, so these customers will be counted as ‘churn’ even though they might be satisfied with the platform and book an appointment in the following period.

Consistent with the above claims of high customer satisfaction, DOC reports excellent product reviews on both the App Store and Google Play stores from > 11,000 combined reviews. Overall, I’m happy with DOC’s product reviews, but will be closely monitoring these reviews and retention rates over the coming quarters.

6) Declining gross margins capture DOC’s struggles to service excess demand

As one might expect, DOC experienced a step-change in demand for their telehealth services after the first COVID-19 outbreak in 2020. While this has led to phenomenal growth in revenues and consultations, this sudden surge in demand forced DOC (along with other telehealth providers) to offer significant incentives (i.e., increased wages) to rapidly attract GPs onto their platform to meet excess demand.

Given that gross margins represent the difference between the revenue generated from a given medical consultation and the wages paid out to the medical professional who provided that service (e.g., GP or advanced nurse practitioner), it is unsurprising that DOC’s gross margins bounced around a lot in 2020 and trended down in 2021 as they offered greater wage incentives.

However, I am not worried. I think DOC management made the right call to sacrifice short-term gross margins to ensure that patient demand could be met without extended waiting times. As mentioned earlier, one of the main attractions of private telehealth services is reduced waiting times and increased convenience relative to the UK NHS. Thus, not offering incentives to onboard GPs for the sake of preserving gross margins would have likely resulted in lower customer satisfaction with DOC. Given their high annual retention rates (> 75%), this would have led to a sharp drop in future bookings and revenues.

7) Change in operational model provides a clear catalyst for gross margin expansion

In December 2021, DOC management announced a change in their operating model which I believe provides a clear impetus for gross margin expansion. Rather than offering a single 20-minute GP consultation, DOC will now offer a range of options. Customers will fill out a short questionnaire and then a computer-based algorithm will recommend one of the following treatment options:

Approval of a routine prescription medication which can be completed without the need for a GP consultation;

15-minute GP consultation (with the option for a diagnostic/specialist referral);

20-minute GP consultation (with the option for a diagnostic/specialist referral); or

Appointment with an advanced nurse practitioner.

Let’s break down each of these changes below.

Following the model of Australian start-up extraordinaire InstantScripts (disclosure: the VC fund I work for has an active investment in InstantScripts), DOC will now enable patients to renew a routine prescription medication without the need for a GP consultation. Similar to InstantScript’s model, I imagine that a GP employed by DOC would be sitting behind their computer evaluating incoming applications for prescription medications based on patient’s questionnaire responses. This process should only take a few minutes per application. Thus, a GP (in theory) should be able to approve many more prescriptions in a given hour (while likely being paid a similar wage), compared to their previous model where each consultation would have lasted 20 minutes.

Offering 15-minute GP consultations for more straightforward medical concerns (e.g., seasonal flu) will enable GPs to see more patients in a given period of time, as the maximum number of consultations per hour has been increased from three to four.

Adding the option to see an advanced nurse practitioner enables DOC to (1) facilitate more consultations through their platform and (2) reduce their dependence on GPs. The wages paid to advanced nurse practitioners would also be much lower than that paid to GPs which, provided there is not an equivalent decrease in the revenue generated per consultation, should be accretive to gross margins. I imagine that DOC management would not have considered this option if it did not materially increase gross margins.

DOC’s CEO has highlighted numerous times his ambition to achieve gross margins at scale in excess of 50%. Given his track record of outperforming internal guidance, I see no reason to doubt these claims and, given the above changes to their operating model, would be surprised to see 2022 annual gross margin below 40%.

8) A strong cash position with no imminent need for a capital raising

DOC ended Q4 2021 with £17.1m in cash ($32.2m AUD) on their balance sheet and no long-term debt. This cash balance represents more than 20% of DOC’s current market cap of $151.6m, as of 8th February 2022.

In 2021, DOC had net operating cash outflows of £16.1m, but the CFO noted on their Q4 conference call that (1) this cash burn would reduce a lot in 2022 and (2) that there was no imminent need for a capital raising in 2022. Thus, I remain confident that DOC has at least 12-18 months of cash burn before needing to tap the public markets for additional cash.

However, the CFO did remain open to the idea that DOC would raise further capital to pursue further acquisitions. I would prefer to see DOC continue to execute their organic growth plans and minimise shareholder dilution, but am open to further acquisitions to consolidate their market leadership in the UK and/or continue expansion into the Asia-Pacific region.

9) A compelling valuation for a high-growth business

As of 8th February 2022 and according to TIKR data, DOC has a market cap of $151.6m. If we subtract $32.2m in cash, DOC has an enterprise value of $119.4m.

Based on 2021 figures, DOC trades on a trailing EV/sales multiple of 2.6x and a trailing EV/gross profit multiple of 6.1x. If we assume 30% revenue growth in 2022 (note: management have not put forth 2022 revenue guidance so I have attempted to be conservative) and stable gross margins (also conservative), DOC trades on a forward EV/sales multiple of 2.0x and a forward EV/gross profit multiple of 4.7x.

The below graph demonstrates how much DOC’s EV/sales multiple has contracted since their IPO (note: Sentieo data reports an incorrect market cap for DOC so the absolute numbers here are wrong, but the overall trend of multiple contraction remains the same).

If we compare DOC to public telehealth competitors (all of which happen to be down > 70% in the past 12 months, making DOC the best performer of the bunch …), we can see that the industry as a whole trades at attractive valuations based on their growth rates and gross margins. For full disclosure, I also own shares in Teladoc (NYSE:TDOC) and have been researching Hims and Hers (NYSE:HIMS) for the past few months.

Given DOC’s small market cap and revenue base, one new large channel partner could have a significant impact on revenue over the next 12-24 months. Thus, I see little value in conducting detailed revenue projections as growth estimates are so sensitive to new deals and partnerships, and DOC has enormous room to expand within both Europe and the Asia-Pacific.

For an investment in DOC, I just need to be confident that: (1) I am purchasing shares at a reasonable valuation, (2) the business should continue to grow revenues at a 20%+ CAGR through to 2026, and (3) there is room for gross margin expansion and eventual GAAP profits. DOC ticks all these boxes for me.

If we assume that DOC holds their current multiple of around 2x forward sales, future shareholder returns should approximate their revenue growth rates. Thus, a 20% revenue CAGR through to 2026 would result in 20% compounded shareholder returns. Future multiple contraction would of course reduce shareholder returns, but I regard this as a low probability outcome as: (1) DOC has already fallen more than 65% in the past 12 months (on strong FY21 results) and (2) DOC has multiple levers to increase gross margins, which will drive them closer to profitability.

10) DOC has concentration risk, but the partnership with AXA Health seems solid

More than 80% of DOC’s eligible lives come from their channel partnership with AXA Health, which is one of Europe’s largest insurance companies. Thus, there is clear concentration risk with an investment in DOC, which is probably contributing to the poor share price performance since IPO.

However, DOC routinely claims that their services result in claims savings of > 25% for their channel partners, which is a win-win for their partnership with AXA Health. Moreover, there are provisions in their contract with AXA Health that prohibits DOC from partnering with direct competitors in the UK (note: it is unclear if this also applies outside of the UK), which in a sense limits their growth in the UK to growth in AXA’s customer base. However, DOC has converted < 30% of their eligible lives into activated lives, so there is still a long runway for growth with AXA Health and other smaller channel partners before this contract clause becomes an impediment to DOC’s growth plans.

Overall, I see no material risks to the partnership with AXA Health in the next 6-12 months, especially after DOC successfully varied their agreement with AXA Health in December 2021 to incorporate the above changes in their operating model.

Conclusion

Overall, DOC operates in an attractive space which has garnered lots of investment dollars in the push to digitise and modernise healthcare. DOC has an innovative value proposition for their private insurance partners and growth in their top-line metrics since IPO has been nothing short of phenomenal. Mr Market seems concerned that DOC is a ‘COVID stock’ and will not be able to continue to grow over the coming quarters, but management’s comments in the Q4 conference call make me optimistic that DOC will continue to chalk up strong results in 2022 (e.g., > 30%+ YoY revenue growth), with material improvements to gross margins and profitability.

While there are risks related to their partnership with AXA Health, I am comfortable adding to DOC at the current share price given the undemanding valuation. I expect DOC to be a significant market beater from the current price and will continue to add over the coming quarters on continued business execution.

Best,

Jordan