Brief Q2 Earnings Review of 3 of My Highest Conviction US Stocks

Coupang, Duolingo, and MercadoLibre all reported strong Q2 2023 results.

1) Coupang (NYSE:CPNG)

Coupang is the largest e-commerce business in South Korea with a core focus on traditional e-commerce (1st and 3rd party), grocery, and food delivery.

The simple investment thesis for Coupang

Coupang is the clear market leader in e-commerce in South Korea and benefits from economies of scale, high brand recognition, and strong pricing power.

Coupang’s CEO is unreservedly following the tried-and-tested Amazon playbook of customer obsession, low prices, and a subscription membership program (“Coupang WOW”). This is an e-commerce playbook that has worked well in most developed markets.

Coupang recently completed a massive CapEx cycle and is seeing tremendous operating leverage from those investments, so margins should continue to expand over the coming quarters.

Coupang is one of the cheapest e-commerce businesses available on global public markets.

Q2 2023 results

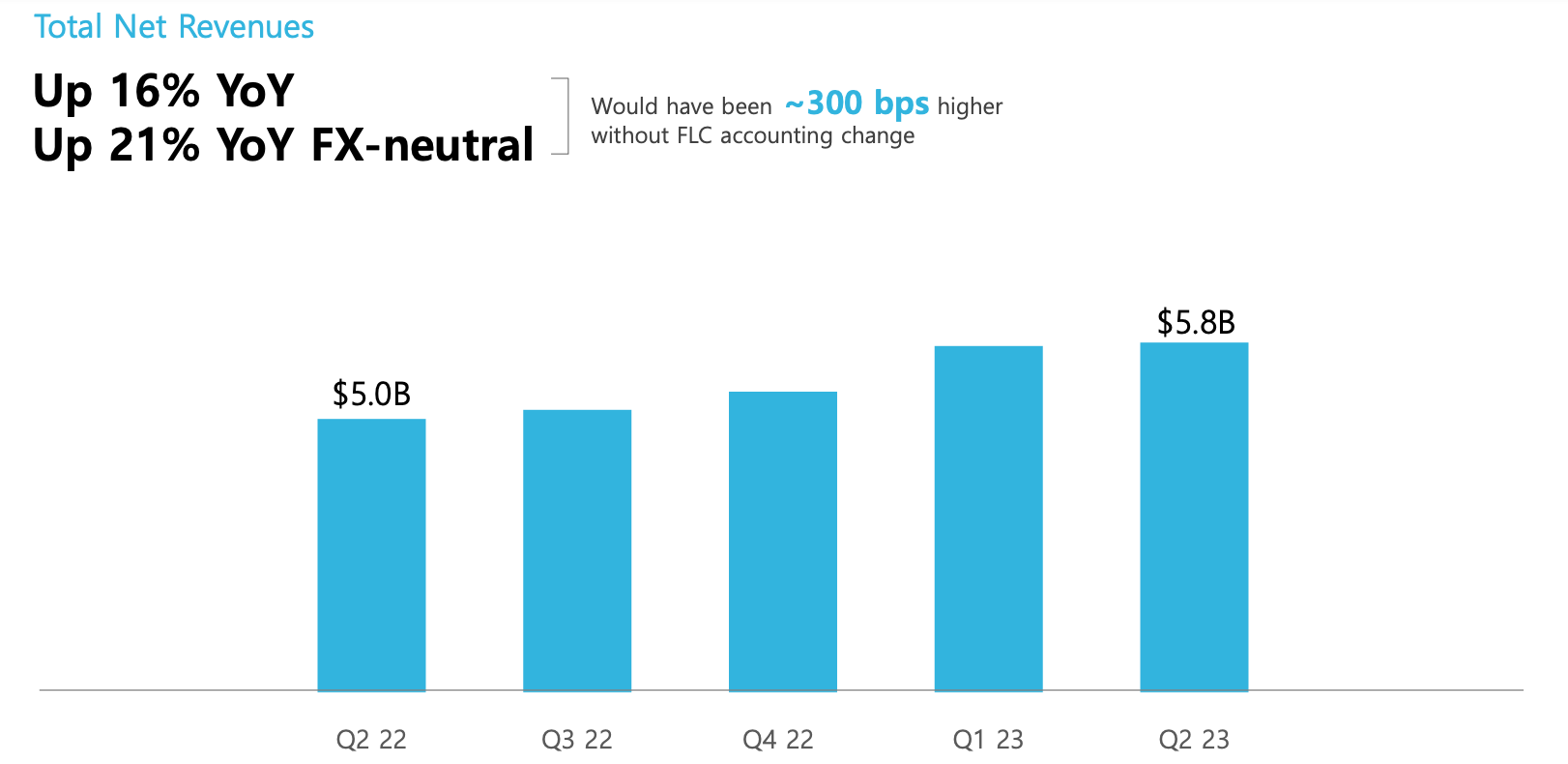

Coupang’s revenue growth has been solid, with consistent double-digit growth each quarter since IPO (21% FX neutral in Q2).

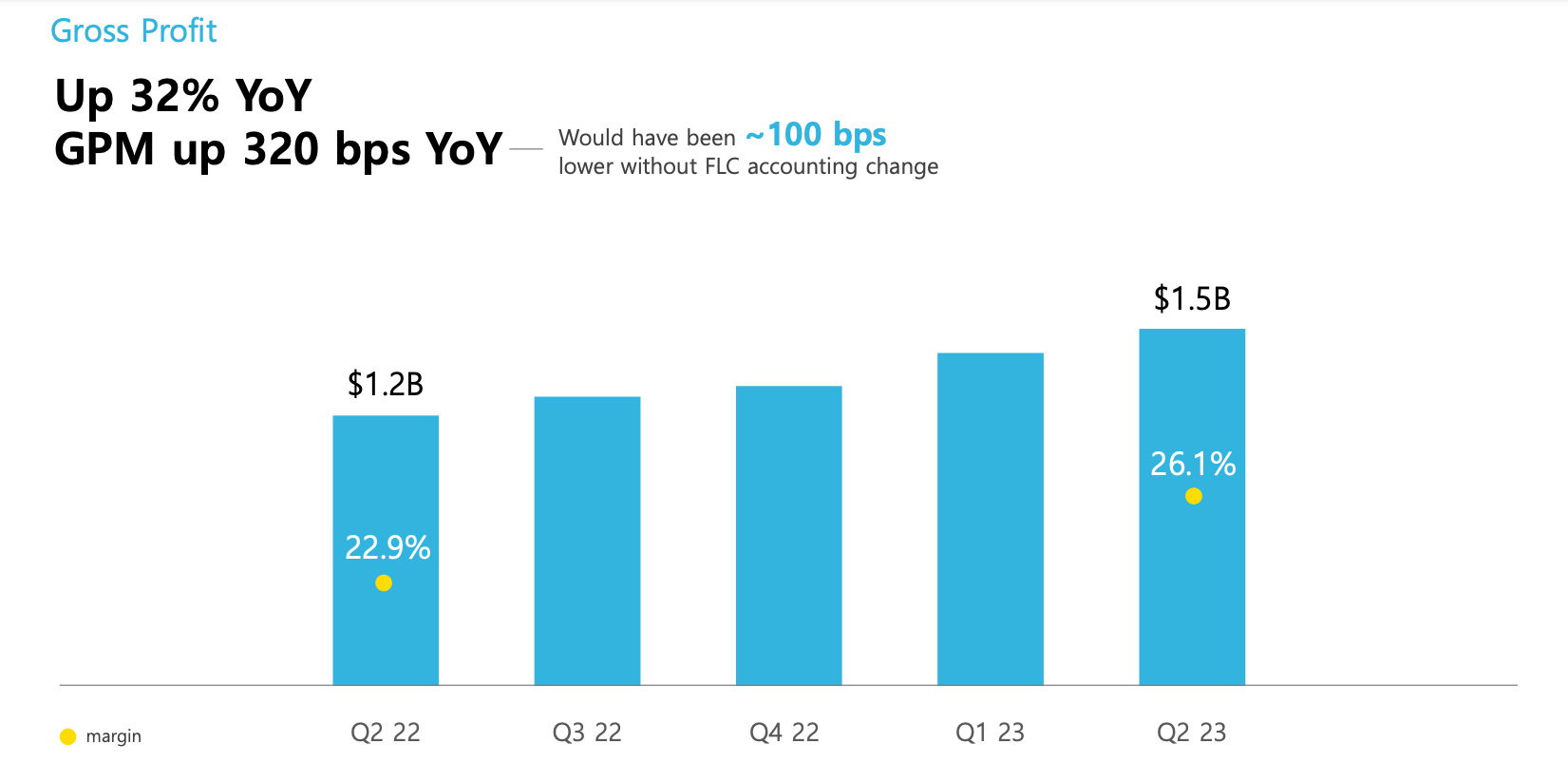

Gross margins have expanded substantially over the past five quarters from 22.9% (Q2 2022) to 26.1% (Q2 2023). Keep in mind that Coupang is a low-margin business (akin to the e-commerce side of Amazon’s business), so gross margins should cap out around the 30-35% mark unless adjacent and higher-margin verticals (e.g., fintech, video streaming, etc) begin to take off.

Coupang has also flipped from being an unprofitable to profitable business (based on GAAP net income) over the past 12 months. While the business looks expensive on a classic P/E ratio due to small base effects, we should see net income rise consistently each quarter moving forward to a more normalised level so that the P/E ratio becomes meaningful.

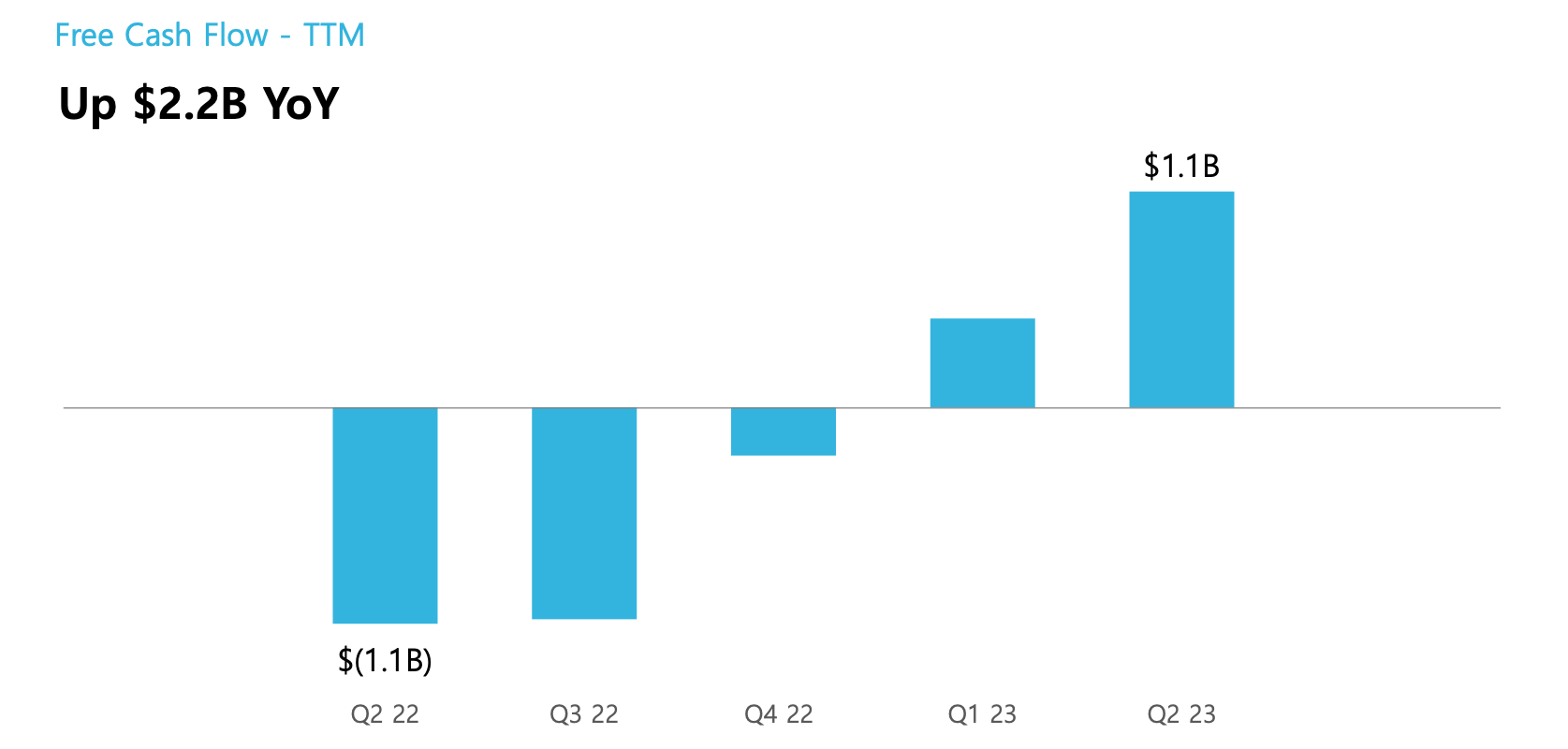

My favourite measure of profitability - free cash flow - has followed a similar trend. On an LTM basis, Coupang generated $1.1b in free cash flow in Q2, representing a 5.0% free cash flow margin.

However, in Q2 alone, Coupang generated $450m in free cash flow, representing a 7.8% free cash flow margin.

Keep in mind that free cash flow (both margins and in absolute dollar terms) should continue to explode higher over the coming quarters as the ratio of 3P to 1P e-commerce increases and revenue scales higher.

Core metrics ($USD)

Market cap: $34.3b

Net cash position: $3.6b

Enterprise value: $30.7b

LTM revenue: $22.1b

EV/LTM revenue multiple: 1.4x

Q2 2023 gross margin: 26.1% (all-time high)

Q2 2023 adjusted EBITDA margin: 5.1% (all-time high)

Q2 2023 free cash flow margin: 7.8% (all-time high)

LTM free cash flow: $1.1b

LTM free cash flow yield: 3.3%

Q2 2023 annualised free cash flow: $1.8b

Free cash flow yield (Q2 annualised): 5.9%

What do I expect from Coupang over the next 12 months?

Revenue growth to remain solid in the 10-20% range (in constant currency), despite macroeconomic concerns.

More clarity on international expansion and growth in fintech revenue.

Margins to continue to rise steadily each quarter. Adjusted EBITDA should come near their long-term target range of 7-10%.

Valuation multiple to re-rate higher to trade in line with global e-commerce peers.

The bottom line

I remain a buyer of Coupang at these levels (note: my average cost basis is around the current share price).

2) Duolingo (NASDAQ:DUOL)

Duolingo is the largest language learning app worldwide with 74m monthly active users (MAUs). The business monetises through paid subscriptions, ads for free users, in-app tokens, and an English accreditation test.

The simple investment thesis for Duolingo

Duolingo operates in a very large market of language learners where there is little digital penetration (i.e., most language learning takes place F2F in classrooms; not via apps).

Duolingo is the dominant market leader with near 100% brand awareness, resulting in very low customer acquisition cost and attractive unit economics.

Duolingo has a capital-efficient business model with 73% gross margins and 25%+ free cash flow margins.

Duolingo has an “underpromise and overdeliver” management culture and has beaten guidance each quarter since their IPO in 2021.

Q2 2023 results

As per usual, Duolingo’s Q2 results were hard to fault.

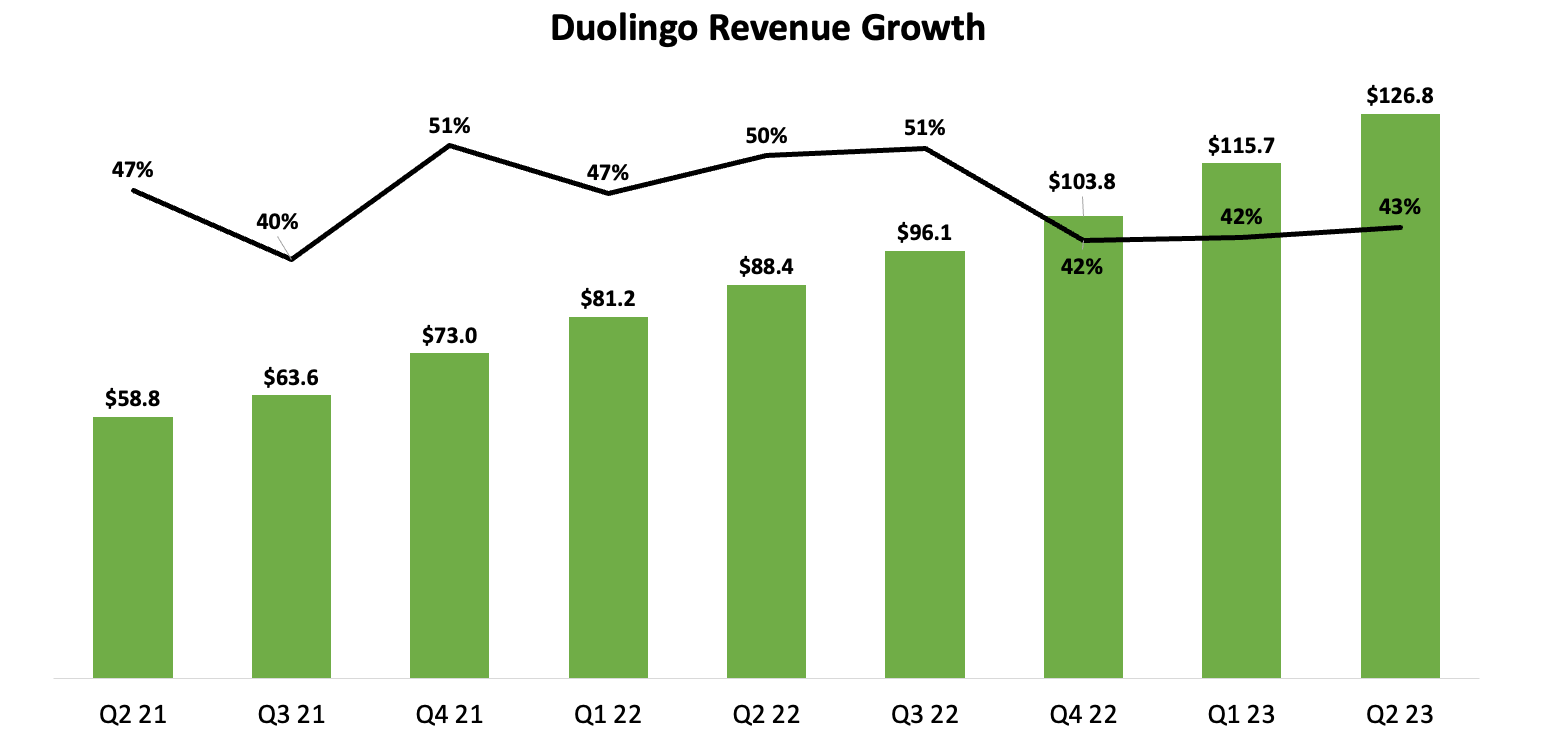

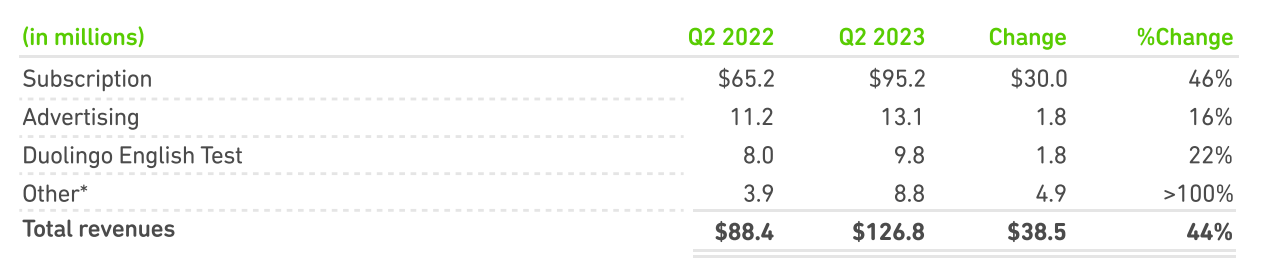

Revenue increased 10% QoQ and 43% YoY to $126.8m. Duolingo has grown revenues more than 40% each quarter since their IPO in 2021.

User growth was also very strong. MAUs increased 50% YoY to 74m while daily active users (DAUs) increased 62% YoY to 21m, leading to a record DAU:MAU ratio of 29% (i.e., 29% of all MAUs are DAUs).

The number of paid subscribers increased 59% YoY to 5.2m. Duolingo’s paid subscriber penetration rate is only 7.9%, showing how much room for growth there is within their existing user base.

Pleasingly, other revenue streams like advertising and in-app monetisation via tokens (“other”) also returned to healthy growth in Q2, supporting the ever consistent growth in subscription revenue from paid subscribers.

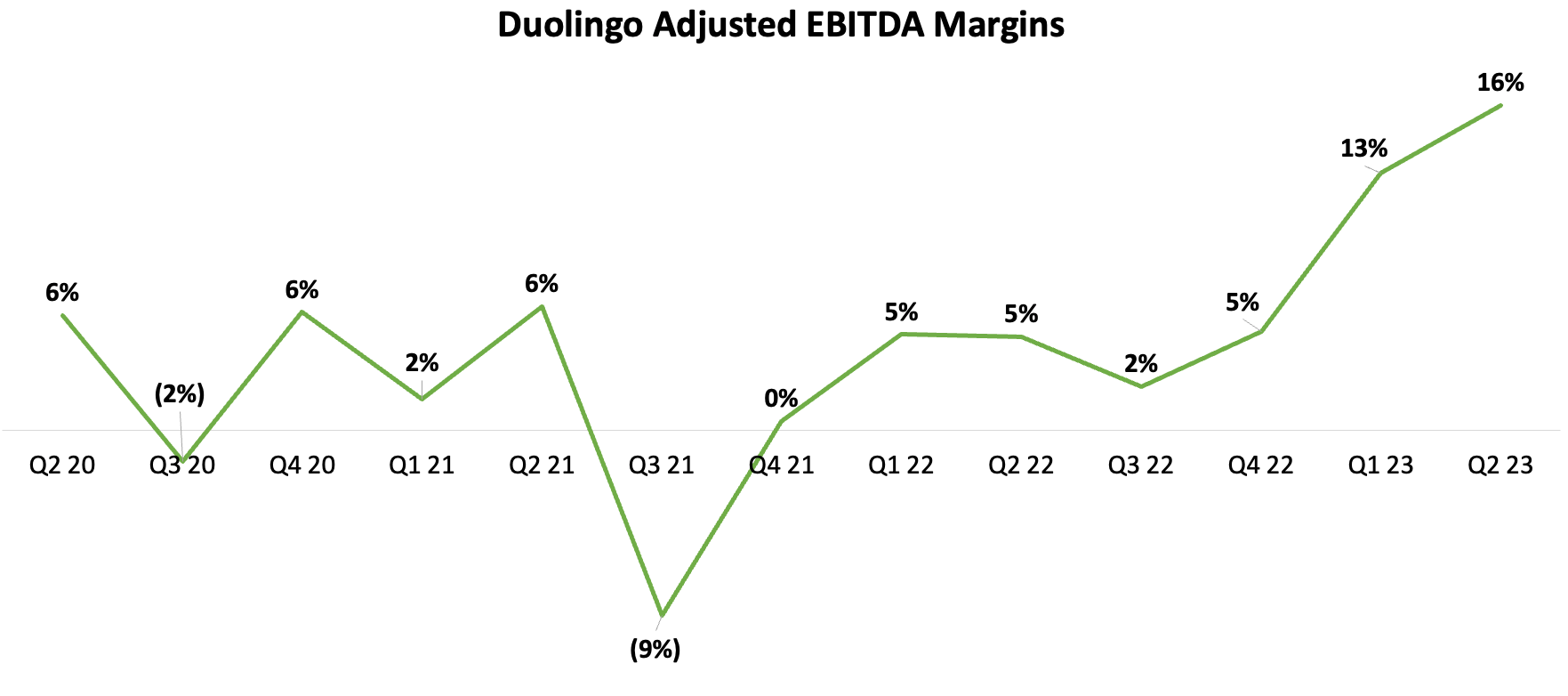

Duolingo has flipped a switch over the past 12 months and turned into a cash generating machine, demonstrating the capital-efficient nature of their business model.

As shown below, adjusted EBITDA margins on a quarterly basis have exploded to 16%.

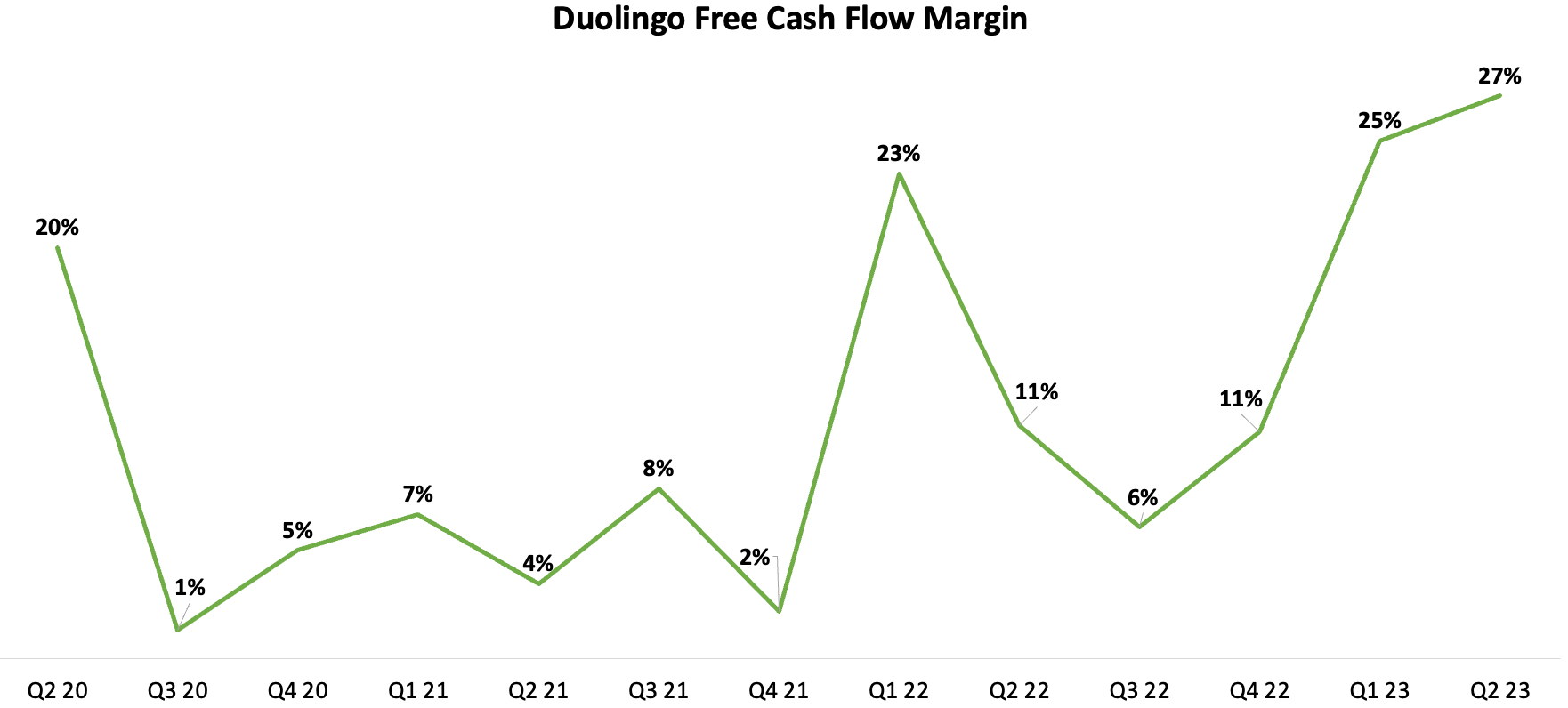

Free cash flow margins also rose substantially to an all-time high of 27% in Q2. While there has been substantial variability in Duolingo’s free cash flow margins since their IPO, I expect their margins to stabilise in the 25-35% range on an ongoing basis.

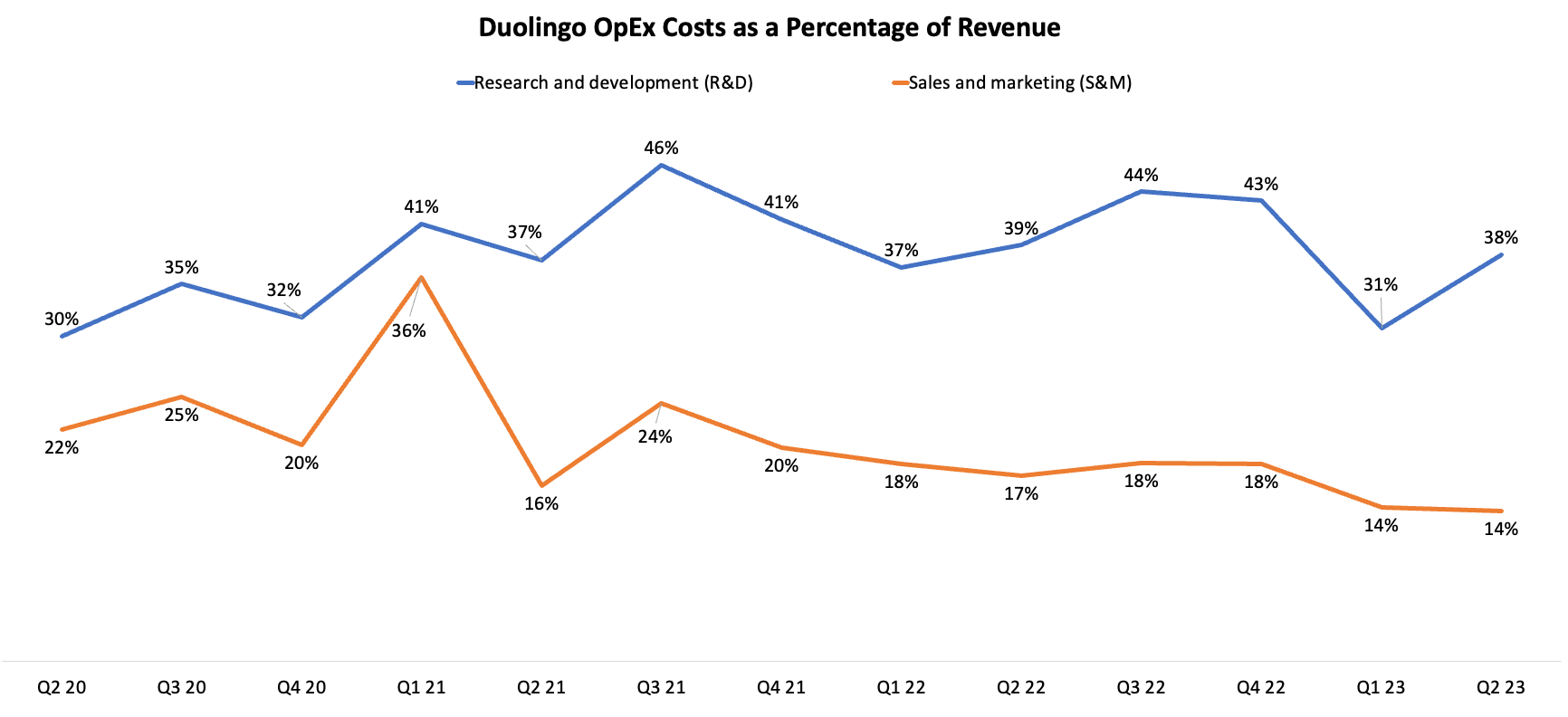

While margins are already strong, Duolingo still has additional room to extract operating leverage. R&D spend remained very high at 38% of revenue in Q2, indicative of their product-led vs. sales-led culture. In other words, while margins have exploded higher in recent quarters, Duolingo has continued to invest aggressively in new product development (e.g., adding new roleplay and AI-based mistake explanations), which should continue to support strong user growth over the coming quarters.

Core metrics ($USD)

Market cap: $5.95b

Net cash position: $680m

Enterprise value: $5.3b

LTM revenue: $442m

EV/LTM revenue multiple: 11.9x

Q2 2023 gross margin: 73.4%

Q2 2023 adjusted EBITDA margin: 16.5% (all-time high)

Q2 2023 free cash flow margin: 27.1% (all-time high)

LTM free cash flow: $80m

LTM free cash flow yield: 1.5%

Q2 2023 annualised free cash flow: $137m

Free cash flow yield (Q2 annualised): 2.6%

What do I expect from Duolingo over the next 12 months?

Revenue growth to remain strong in the 30-45% range, driven by increasing paid subscriber penetration and in-app monetisation.

Adjusted EBITDA margins to exceed 20% on a quarterly basis and free cash flow margins to exceed 30% on a quarterly basis.

Duolingo to continue to perform ahead of management guidance.

EV/LTM revenue multiple to drift down towards the high-single digits.

The bottom line

It’s tough to argue that Duolingo is a “cheap” stock based on classic valuation metrics, but I believe it warrants a premium vs. broader software multiples given the growth rates and attractive unit economics. Nonetheless, I think the current valuation is appropriate (or slightly overvalued) and have not added to my position so far in 2023 (note: my average cost basis is in the $60s).

3) MercadoLibre (NASDAQ:MELI)

MercadoLibre is a powerhouse conglomerate in Latin America, boasting the largest third-party e-commerce business in the region (think eBay), along with a rapidly growing fintech platform (MercadoPago; think PayPal), logistics business (MercadoEnvios; think Amazon), and credit portfolio (MercadoCredito; think an innovative credit lender).

The simple investment thesis for MercadoLibre

MercadoLibre is the dominant market leader in e-commerce in Latin America, with economies of scale, strong brand recognition, and lots of pricing power (similar to Coupang in South Korea).

MercadoLibre has a world-class management team that has proven to be adept at adjusting to market conditions, e.g., investing heavily to build out their infrastructure in 2020/2021 when the cost of capital was low and pulling back on CapEx in 2022/2023 to show operating leverage when the cost of capital was higher.

MercadoLibre has substantial optionality and many avenues for growth, either within existing business lines or adjacent business areas (e.g., investment advisory services, digital banking), leveraging their strong brand in Latin America.

MercadoLibre trades near the bottom of their 10-year EV/LTM revenue valuation range despite strong business performance, rapidly expanding margins, and improving leverage ratios.

Q2 2023 results

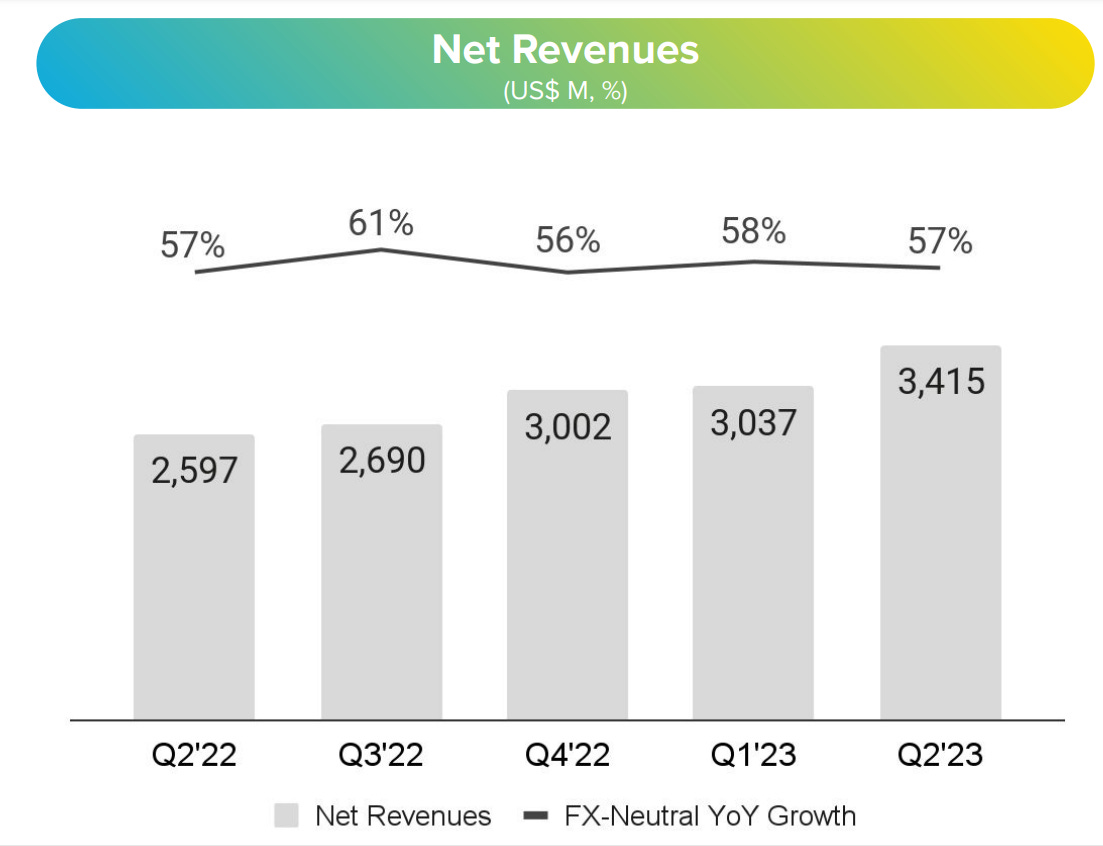

MercadoLibre is a beast. In the face of tough macroeconomic conditions in Latin America, growth rates continue to remain strong. Currency effects are pronounced in Latin America, so most of their charts are presented in USD constant currency. As is shown below, net revenue growth rates in constant currency (includes all their different business segments) have remained above 50% for the last few quarters.

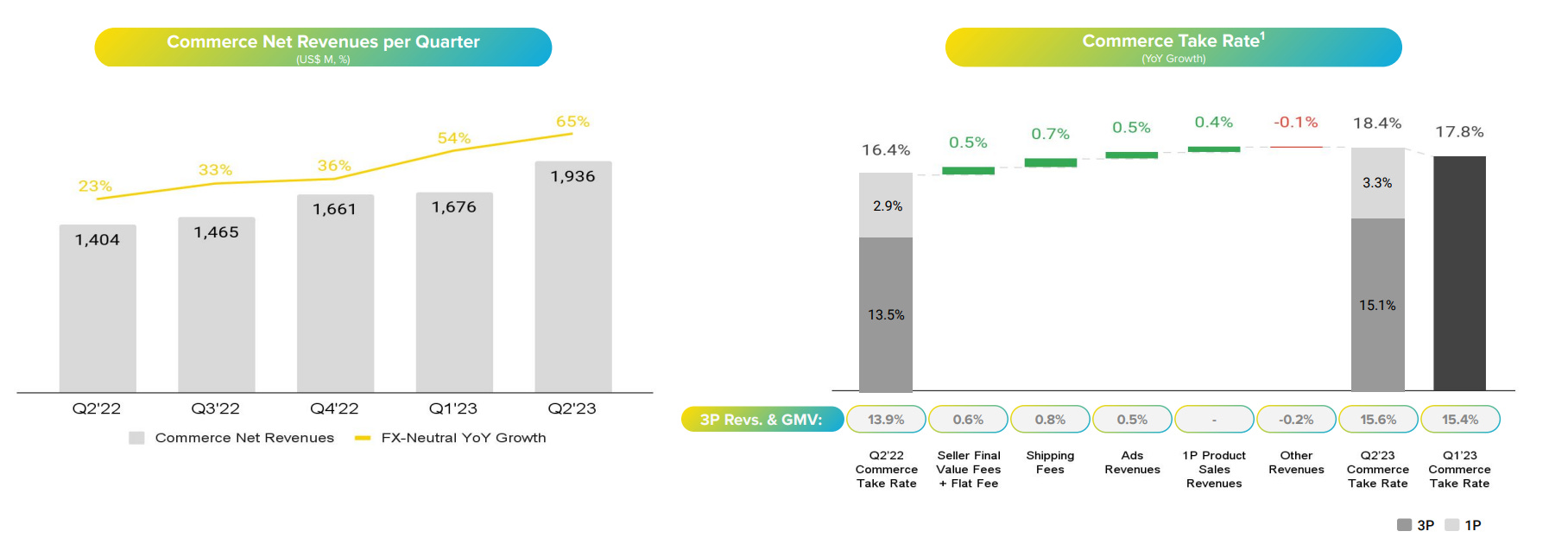

Commerce net revenue growth rates have even accelerated in recent quarters as MercadoLibre continues to gain market share and flex their pricing power, resulting in higher take rates.

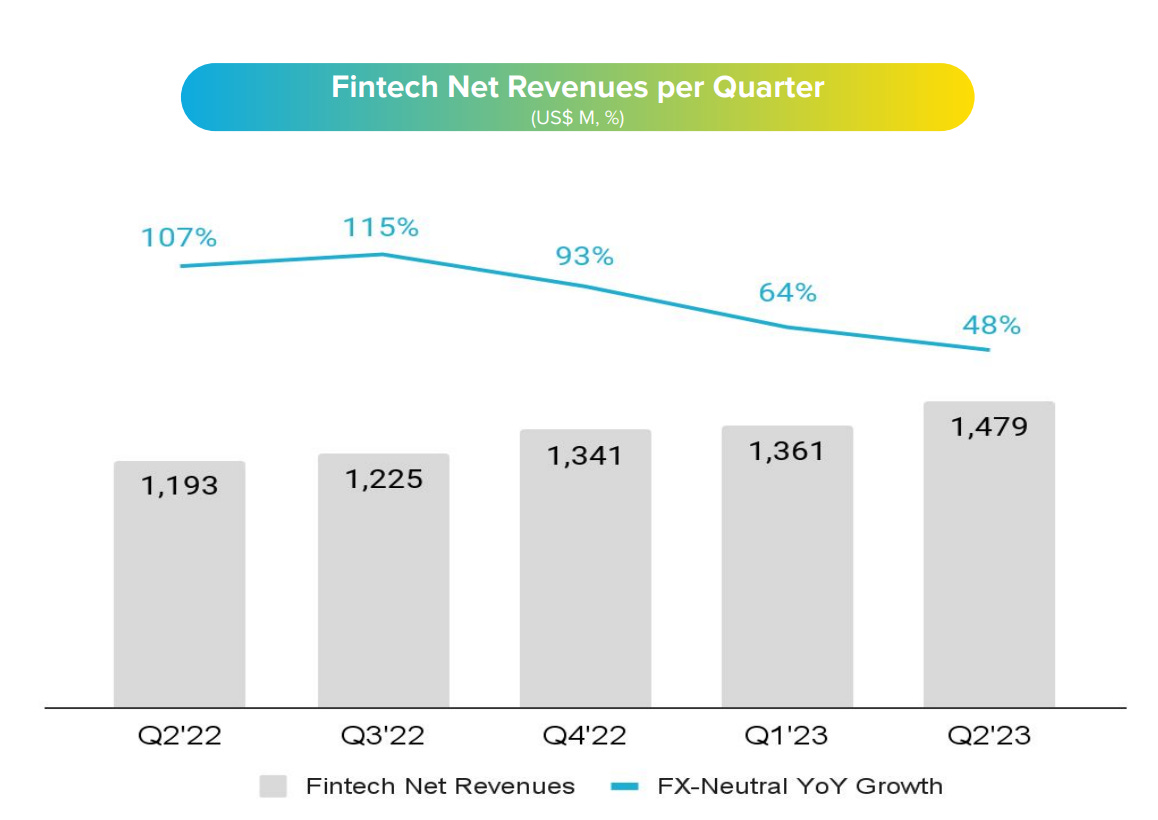

Fintech net revenues (primarily transaction-related both on their e-commerce platform and also off-platform) have decelerated substantially in recent quarters, but remain very strong in absolute terms (48% in Q2).

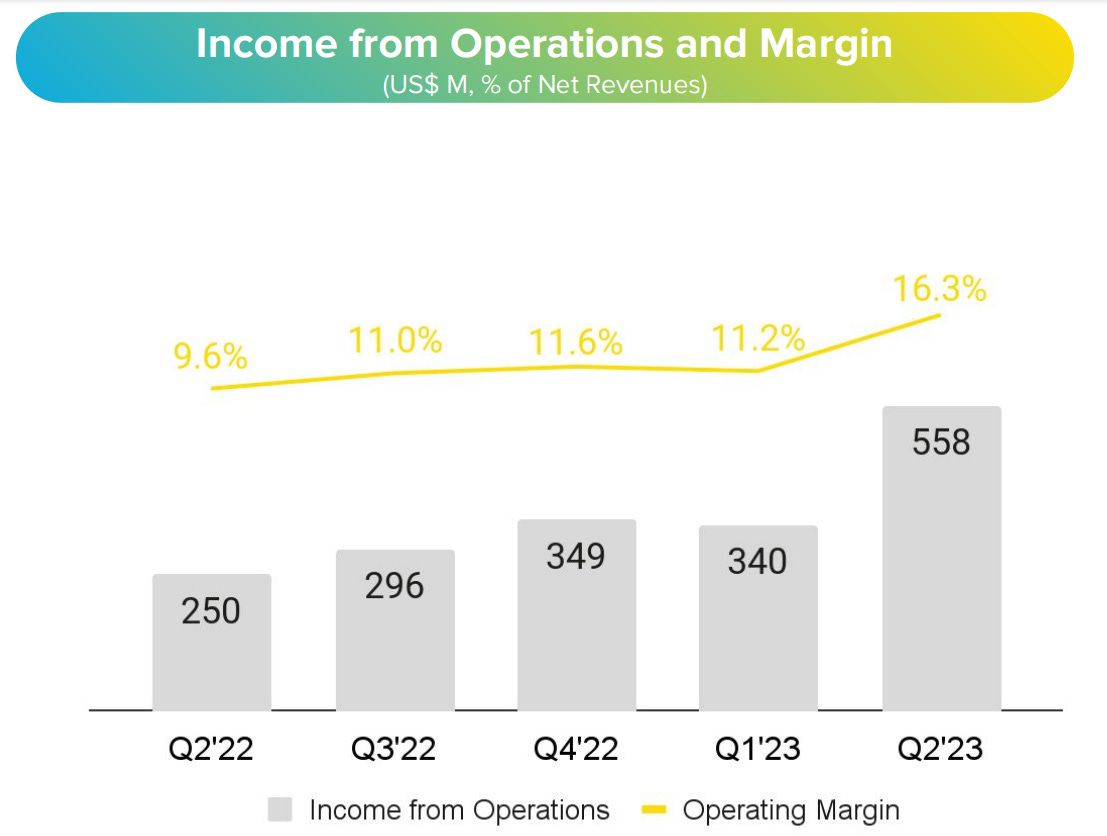

Arguably the highlight of MercadoLibre’s Q2 release was their strong YoY expansion in operating margins from 9.6% (Q2 2022) to 16.3% (Q2 2023), even as they continue to invest in product development and expand their workforce. A large part of this improvement in operating margin was attributable to scaling back their credit portfolio and associated provisions for doubtful accounts (i.e., bad debts).

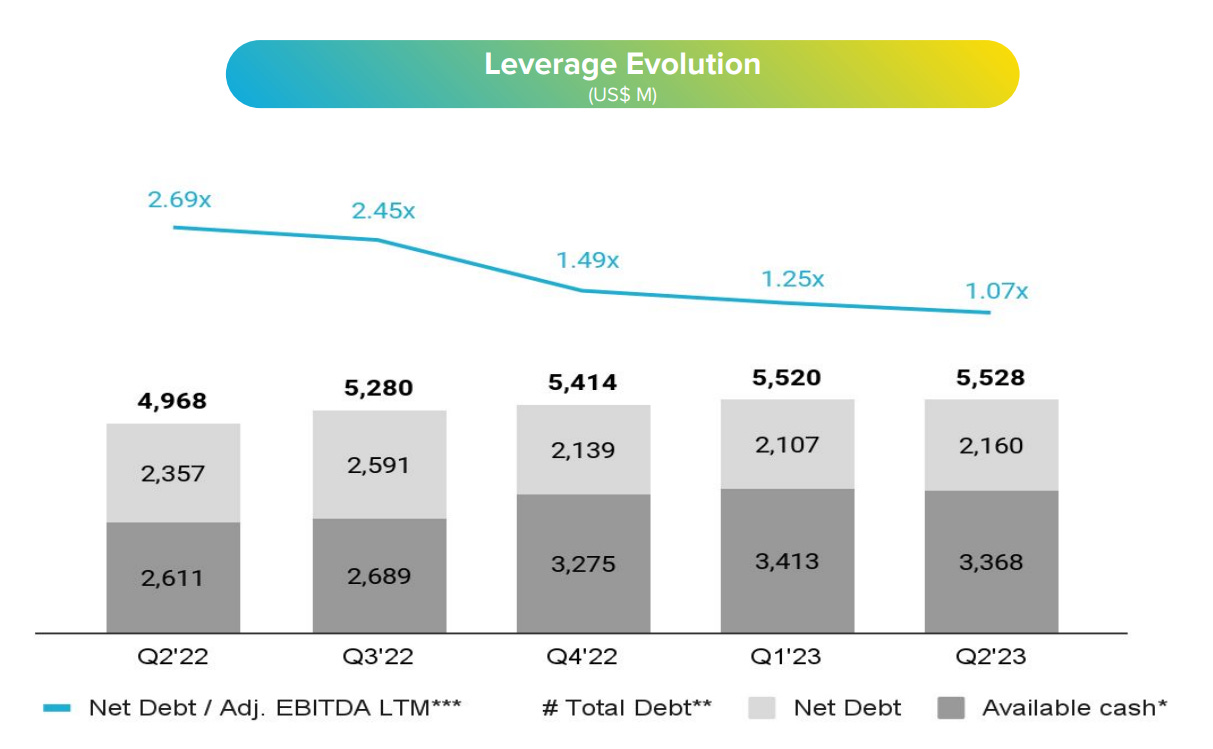

One of my longstanding concerns with MercadoLibre (albeit minor) has been their net debt position (I prefer to invest in companies with a strong net cash position), but it’s pleasing to see their leverage ratios coming down over time as a function of strong free cash flow generation and minimal issuance of new debt.

Core metrics ($USD)

Market cap: $65.75b

Net debt: $2.16b

Enterprise value: $67.9b

LTM revenue: $12.1b

EV/LTM revenue multiple: 5.6x

LTM operating income (EBIT): $1.54b

EV/LTM EBIT multiple: 44.1x

Q2 2023 gross margin: 50.4%

Q2 2023 operating margin: 16.3%

H1 2023 free cash flow: $2.07b

Annual free cash flow (annualised): $4.14b

Annualised free cash flow yield: 6.1%

What do I expect from MercadoLibre over the next 12 months?

Net revenue growth rates to decelerate from current levels to the 15-30% range (more normalised levels in the face of macroeconomic headwinds).

Operating margins to continue to expand, even as MercadoLibre continues to invest heavily in product development and building out their logistics infrastructure.

MercadoLibre’s valuation to return to its long-term average (high single-digit EV/LTM revenue multiple) as margins continue to expand.

The bottom line

MercadoLibre is a company I wouldn’t want to bet against as their operating performance surpasses my expectations almost every quarter. Take a look at a long-term stock price chart to see why it pays (handsomely) to back MercadoLibre and its management team. I’ll look to buy more shares on short-term price weakness (note: my average cost basis is in the $800s).

Summary

Each of these three companies are in my top 10 largest stock positions, all united with some common themes which are representative of my investment approach:

Founder-led.

Product is “loved” by customers.

Market leaders in their respective industries which have notable barriers to entry.

Demonstrated track-record of strong 10%+ top-line growth.

Strong free cash flow margins or undergoing a period of rapid margin expansion.

Management team that tend to “underpromise and overdeliver” on guidance.

Does not trade at an egregious valuation.