Airtasker: An Under-The-Radar High-Margin Marketplace With a Long Runway for Growth

Airtasker is a two-sided marketplace for local labour services with a capital-light business model, high inside ownership, long runway for growth, and attractive valuation.

General details (as at 26th September 2021)

IPO date: 23rd March 2021

Share price: $1.00

Market cap: 414m (AUD)

YTD return: -4.76%

Distance from 52-week high: 49%

Founding story

Airtasker (ASX:ART) was founded in February 2012 by Tim Fung and Jonathan Lui. Tim Fung conceived of the idea for Airtasker when he was moving apartments and wondered why there was no app where he could easily hire a removalist to assist with the process. Instead, he had to ask friends for recommendations for local removalists, which he thought (rightfully so!) was cumbersome and time-inefficient.

What is Airtasker?

Airtasker is a two-sided marketplace for local labour services that connects people who need a task completed (customers) with service providers (taskers). Example tasks that can be ordered through Airtasker include repairing a broken fridge, installing a TV, cleaning a house, and finding a lost drone, as well as more complex tasks, such as architectural design and legal advice. Airtasker operates their online marketplace with both a desktop and mobile app (see here), which is sleek and intuitive to use.

Labour services can be classified as local or remote services. Airtasker’s bread and butter is local face-to-face services which are more blue collar in nature and are carried out in the presence of the customer. These local services account for 89% of the global labour market (reference), so there is no shortage of available demand for Airtasker.

This distinction between local and remote services is important because it differentiates Airtasker from larger service-based marketplaces, such as Upwork, Fiverr, and Freelancer, all of which are public companies. These marketplaces focus on remote services which are more white collar in nature and can be carried out anywhere, for example, graphic design, video editing, and copywriting.

The below diagram compares Airtasker with their domestic and international competitors based on (1) whether the services offered tend to be local or remote and (2) whether revenue is primarily generated from a service fee or advertising. Only Airtasker and TaskRabbit offer local services through a service fee model and TaskRabbit does not operate in Australia, which accounts for more than 95% of Airtasker’s FY21 revenue. Hipages is Airtasker’s main competitor in the Australian market and a detailed comparison of both companies is made later in this article.

Customers can order a service through Airtasker via one of three methods:

Legacy model. This process is as follows: (1) customers post a task that needs completing with a specific date, time, and budget; (2) taskers offer a price within that budget; and (3) the customer chooses a tasker to complete the task.

Listings model. Taskers pre-package a service and offer it for a fixed price. Customers browsing Airtasker for listings might discover one of these service packages and purchase it ‘off the shelf’ from the tasker. This listings model was introduced in 2021.

Subscription model. For tasks that are recurring in nature (e.g., house cleaning), customers are able to organise a subscription schedule for the task to be completed. This model currently accounts for a very small portion of overall activity on the platform.

Airtasker makes the booking process open and transparent. All taskers registered on Airtasker have a public profile where prospective customers can appraise previous star ratings, customer reviews, qualifications, licenses, and even COVID-19 vaccinations. Taskers and customers are able to message through the app for the duration of the task without sharing personal contact details.

Business model

Airtasker does not charge upfront fees to customers or taskers to join the platform. Instead, Airtasker earns a commission from both sides of the marketplace for each transaction. Customers are charged a booking fee ranging from $2.90-24.90 and taskers are charged a service fee according to a tiered pricing structure. Both these fees are calculated as a percentage of the total task value and are not charged unless the task is successfully completed. In other words, neither customers or taskers are charged for no-shows.

Airtasker’s tiered pricing structure means that devoted taskers who complete more tasks through the platform are rewarded with lower service fees. This incentivizes taskers to (1) work more exclusively with Airtasker and (2) keep transactions on the platform (more on this issue later!)

Airtasker’s take-rate in FY21 was 17.4%, which means that for every $100 of tasks ordered through the platform and completed (gross merchandise volume; GMV), Airtasker keeps $17.40 as revenue. In short, more frequent transactions and/or higher transaction amounts results in a higher GMV, which, assuming take rate remains constant or increases over time, results in higher revenue for Airtasker.

Growing network effects

Airtasker has experienced rapid year-over-year growth in active customers from 18,000 (FY15) to 415,000 (FY21). On average, these customers transact 1.9 times each year through the platform with an average task price of $198. This average task price has increased consistently since FY15, possibly as customers become more familiar and trusting of the Airtasker platform.

Critical to building a network effect in marketplaces is: (1) ensuring growing demand from customers; and (2) building out the supply of people delivering the product or service (taskers). More customers and greater demand for services attracts more taskers to the platform, who then offer a wider range of tasks to differentiate from competitors. This positive feedback loop also serves to decrease the median response time taken for a customer to receive a first initial offer from a tasker, which has dropped from 5.9 minutes in 2015 to 1.9 minutes in 2020.

Customers like Airtasker (a lot)

While writing this article, I did some good old-fashioned scuttlebutt research asking around 10 friends who had used Airtasker to describe their experience. Overall, I was pleasantly surprised by how positive their feedback was, with only one person reporting a negative past experience. A quick google search of Airtasker on Product Review, App Store, and Google Play store validated their experiences. Airtasker scores:

4.4/5 from 10,300 reviews on Product Review.

4.8/5 from 128,000 reviews on the App Store (see below).

4.8/5 from 13,100 reviews on the Google Play Store.

These are fantastic scores and a testament to the investments that Airtasker has made in optimising their user experience. Nonetheless, a number of friends raised concerns about the Airtasker business model which is worth noting.

Apparently, when they posted a task to be completed on Airtasker, many (but not all) taskers would message through the app with their contact details asking to complete the transaction off-platform to circumvent the service fee (remember Airtasker only collects fees AFTER the task has been completed). One friend who works at Airtasker confirmed that Airtasker is keenly aware of this issue and has measures in place to detect and ban taskers who engage in this kind of behaviour.

Friends also noted that several taskers provided their contact details in-person after a task has been completed and offered a reduce price for future transactions completed off-platform. In other words, these taskers use Airtasker for lead generation, but not for recurring transactions. Airtasker’s tiered pricing structure (explained above) attempts to counteract this issue and encourage repeated use of the platform to attract lower service fees, but it still appears there is work to be done on this end for Airtasker, particularly for part-time taskers who complete the occasional task as a ‘side-hustle’ but do not work enough to benefit from reduced service fees in the silver, gold, or platinum tiers.

Organic customer acquisition

One significant (but often under-appreciated) benefit of excellent customer experiences is the subsequent positive word-of-mouth, which increases organic customer acquisition and reduces customer acquisition cost (CAC). Think about Tesla who has never spent a dime on marketing but has waitlists for their newer models out to late 2022.

Airtasker has managed to add more than 90,000 new customers in the past 24 months while pulling back on sales and marketing expenses. Indeed, 99% of new customers in FY20 were acquired from non-paid marketing channels (source).

Airtasker has noted their strategic plan to increase marketing costs in FY22, which, combined with their powerful organic customer acquisition, should result in a rapid growth of customers in FY22. Backing up this move, Airtasker recently hired Noelle Kim — who was the former head of marketing for the Asia-Pacific region at Instagram — as their chief marketing officer (CMO).

Financials

Revenue & GMV

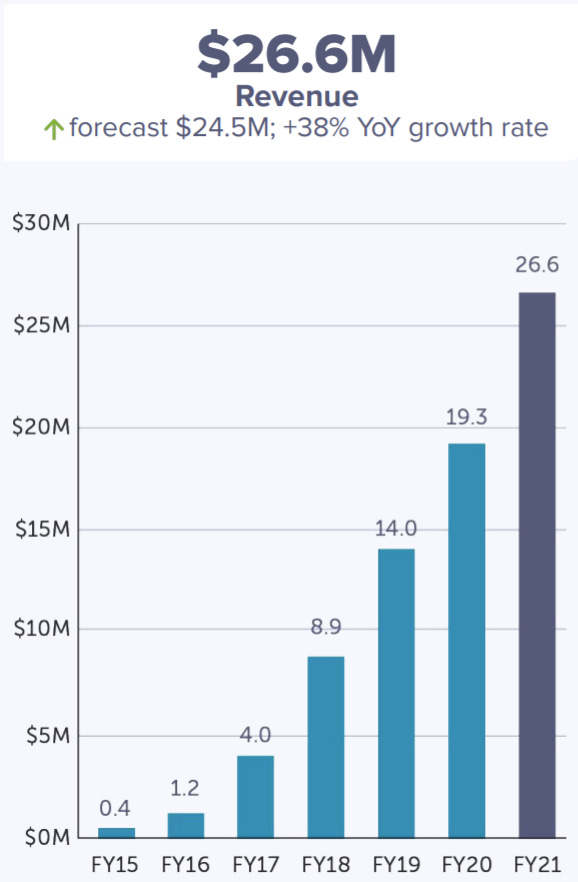

Airtasker has reported a compound annual growth rate (CAGR) in GMV since inception (FY15-FY21) of 91%, with revenues increasing at a staggering 101% CAGR. Their FY21 revenue of 26.6m smashed their prospectus forecast of 24.5m and represented a 38% year-over-year increase. Their GMV grew 35% year-over-year to 153.1m, also well ahead of their prospectus forecast of 143.7m.

Airtasker is forecasting FY22 revenue of at least 35m (32% year-over-year growth), which includes the COVID-19 lockdowns in Sydney and Melbourne (remember Australia accounted for more than 95% of Airtasker’s FY21 revenue). Taking into account that these lockdowns have persisted for the past 3-4 months in Australia’s two largest cities, this guidance is solid. However, there is a possibility of a revenue downgrade in the event of further COVID-19 restrictions in late 2021 or 2022, so I will be monitoring their quarterly revenue numbers very closely.

Margins and cash flow

Airtasker consistently reports gross margins above 90%. In both FY20 and FY21, their gross margin was 93%. In FY21, they also reported positive operating cash flow of 5.5m as they increased in scale and cut back on marketing spend during COVID-19 lockdowns.

As has become the fashion with fast-growing technology companies, Airtasker is not profitable, reporting a net loss of 9.7m in FY21. Personally, I am not worried about the current lack of profitability - Airtasker is a very small company with only 26.6m in annual revenue and limited brand recognition, so I am happy to see them invest more into sales and marketing, refining the product experience, and hiring additional customer support staff. With a capital-light business model and 93% gross margins, there are plenty of profits to be earned later if Airtasker gains significant market share and can begin to reap the rewards afforded from network effects.

Cash position

Airtasker has 45.9m in cash with no debt, resulting in a current enterprise value of 368m.

International expansion - a key element of Airtasker’s future growth

Revenue from Australia currently accounts for more than 95% of Airtasker’s revenue, but international revenue should become a more meaningful contributor to revenue from FY22 onwards. In 2020, Airtasker launched marketplaces in the UK, New Zealand, Singapore, and Ireland and expanded into the US in 2021 via their acquisition of Zaarly. Based on management commentary in their FY21 results, it appears that the US and UK are the most exciting international growth levers so I discuss their expansion into each of these countries below.

Expansion into the lucrative US market

Airtasker established a presence into the US via the acquisition of Zaarly in May 2021 for 3.4m (AUD). Zaarly is an interesting business and this acquisition is a critical element of Airtasker’s future growth plans so it’s worth delving into their backstory.

Zaarly was founded in 2011 and operated as an open marketplace for local services, very similar to Airtasker. They raised 15.2m (USD) across both their seed and series A funding rounds from some very well-known investors, including Kleiner Perkins (one of the most renowned VC firms in the US), Naval Ravikant (CEO of AngelList), Paul Bucheit (managing director at Y Combinator), and Ashton Kutcher (famous actor).

Zaarly exploded in popularity in 2011 at a breakneck pace that management felt was too fast to handle without comprising the user experience. In 2013, Zaarly fatally pivoted to a closed marketplace model to ensure centralised control over which service providers were able to register to use the platform, enforced via strict hiring and vetting processes. In other words, rather than letting star ratings and customer reviews act as decentralised quality control measures, Zaarly chose to centrally control quality through the interview and hiring process.

While this decision seems logical at first glance, it acts as tremendous resistance to the natural network effects and scale that comes from a decentralised marketplace. Imagine if Amazon conducted a detailed vetting process on each prospective seller before allowing them to join the Amazon marketplace … would we have even heard of Jeff Bezos?

Open marketplaces benefit from an intrinsic positive feedback loop: more customers brings more suppliers and a wider range of products/services, which in turn attracts more customers. Customers rate/review suppliers (or taskers) after each transaction on a public profile for all future customers to see. If a tasker has poor reviews, customers are much less likely to choose to work with that person. When was the last time you ate at a restaurant with an average google review score of 2.2/5 or booked an Airbnb destination with a 3.4/5 rating? Decentralised control at its finest.

At the time of the acquisition, Zaarly had around 900 active service providers and a database of more than 597,000 registered users (note: most of these users would not have used the platform for many years). Their top three cities in terms of registered users were: (1) Kansas City; (2) Dallas; and (3) New York. Exact revenue numbers are hard to find, but I’m going to assume it wasn’t pretty.

Zaarly was on the verge of shutting down the platform in 2021 before Airtasker acquired them for less than 20% of the total capital invested, just across the seed and series A financing rounds (note: they also raised a series B and an additional venture round but these amounts are not disclosed on Crunchbase). Another possible valuation metric is that Zaarly was acquired for around $5.70 per registered user.

So, how is this acquisition accretive to Airtasker?

Airtasker will be rebranding Zaarly to Airtasker US and … converting it from a closed to an open marketplace, which should lead to a large jump in the number of taskers registered on the platform.

Zaarly has an average task price of $500 (USD), which is around 3.5x the average task price of Airtasker ($198 AUD). This should provide a tailwind for Airtasker’s average task price to increase over time.

Airtasker aims to launch into 4-5 additional US cities throughout FY22, which should result in further revenue growth.

Re-bookings accounted for more than 75% of Zaarly’s GMV as many customers used the platform for recurring subscription purchases. Tim Fung has noted that Zaarly has developed sophisticated back-end processes that reduce the service and booking fees charged for each successive transaction between a customer and tasker. Airtasker plans to integrate this software into their marketplace across other geographies, which should help to drive recurring revenue and reduce leakage from off-market transactions.

Organic expansion into the UK market

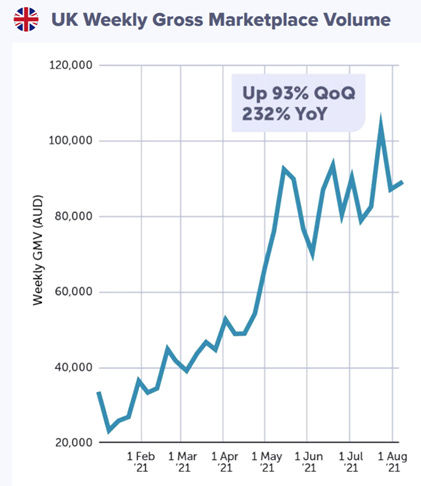

Airtasker expanded into the UK in 2020 and have experienced rapid sales traction, albeit off a low base. Airtasker UK reported 93% quarter-over-quarter and 232% year-over-year increase in GMV in Q4 FY21. Tim Fung has noted that UK customers have similar behavioural patterns to Australian customers, which means that the blueprint for expansion in Australia might translate to the UK.

Comparison with competitors

Airtasker’s main competitor in the Australian market is hipages (ASX:HPG), which went public in late 2020. Below I have compared their notable operational and financial metrics with Airtasker.

Comparing these metrics, it is clear that hipages is the more established business with annual revenue more than twice that of Airtasker. However, Airtasker has a 3-year revenue CAGR of 44% and higher gross margins, which demands a higher enterprise value to trailing-12 month (TTM) revenue multiple. While hipages is hyper-focused on one vertical (tradies) and has transitioned over time to a digital-centred subscription model, Airtasker has a much broader service offering and was founded on a digital backbone.

While Airtasker and hipages are competitors, their main competition is services that are initiated outside of marketplaces, such as calling up local service providers to ask for a quote. As has become the trend with most goods and services (think the shift from in-person retail to e-commerce), I think more and more of these transactions will over time be carried out via marketplaces, such as Airtasker.

Management and insider ownership

Insiders at Airtasker own more than 50% of outstanding shares. Below I describe some of the core members of the management and board with notable ownership stakes.

Tim Fung (co-founder and CEO) has an impressive and diverse background. He worked for five years as an analyst at Macquarie Bank before pivoting to work for a fashion modelling talent agency. He was also a founding team member at Amaysim — a domestic provider of mobile phone plans — which was founded in 2010, went public in 2015, and was acquired by Optus in 2020 for 250m (I hope Tim held onto his shares!). Tim owns around 12% of outstanding shares in Airtasker.

James Spenceley (independent non-executive chairman) founded Vocus Communications, serves as a non-executive director at Kogan, and has been twice awarded Young Australian Entrepreneur of the Year. He owns around 1% of outstanding shares.

Peter Hammond (non-executive director) co-founded and is director of Exto Partners, a Sydney-based VC firm. He owns around 16% of outstanding shares.

Fred Bai (non-executive director) co-founded and is managing partner of Morning Crest Capital, a Chinese-based VC firm, and was also the co-founder of Reven Housing REIT (NASDAQ:RVEN). He owns around 14% of outstanding shares.

Valuation (as at September 26th 2021)

Given that Airtasker is not currently profitable and is heavily re-investing for future growth, I have decided to value the business using EV/sales and EV/gross profit multiples. I have attempted to forecast revenues five years out into the future, which I believe is a sufficient holding period to judge whether the growth story has played out.

As at 26th September 2021, on a trailing 12-month (TTM) basis, Airtasker trades on an EV/sales multiple of 13.8x and an EV/gross profit multiple of 14.8x.

Assuming Airtasker meets their FY22 revenue guidance of 35m and maintains consistent 93% gross margins, the business trades on a 1-year forward EV/sales multiple of 10.5x and an EV/gross profit multiple of 11.3x.

Below I have compiled a table comparing different return multiples and internal rates of return (IRRs) over a 5-year period with conservative, base case, and aggressive revenue forecasts based on: (1) Airtasker’s 3-year CAGR in the Australian market; and (2) possibilities for international expansion. Given some of the comparative valuations for marketplace businesses in the public markets, these exit EV/sales multiples might appear conservative for a business with 93% gross margins growing at a healthy double digit rate, but this is by design to add some margin for error (i.e., buffer) into the model.

Thesis

To summarise, the bull case for Airtasker is as follows:

Operates in a very large and fragmented industry with no clear market leader (i.e., the equivalent of Amazon for US e-commerce).

Founder-led business where the CEO owns around 12% of outstanding shares and insiders own more than 50% of outstanding shares.

Capital-light and scalable business model with 93% gross margins and a demonstrated ability to be operating cash flow positive with only 26.6m annual revenue.

Growing network effects with more customers and taskers joining the marketplace due to positive past experience and organic word-of-mouth.

Lots of scope for product-related improvements to reduce off-market transactions and increase repeat bookings, both of which will be aided by the recent acquisition of Zaarly.

Rapid sales traction in the UK market (232% year-over-year growth) with lots of potential for the Airtasker US business to become a meaningful contributor to revenue once the marketplace is converted from a closed to an open structure.

Trailing-12 month valuations of 13.8x EV/sales and 14.8x EV/gross profit is reasonable given the growth rates and margins. Base case scenario over five years of 30% revenue CAGR and an exit EV/sales multiple of 10x generates a 21.8% IRR, which is well above my 15% threshold.

Risks to the thesis include:

A large player (e.g., Amazon, IKEA) enters the local services market.

Airtasker is unable to reduce off-market transactions.

Major reputational damage to the brand of Airtasker from a PR crisis.

Sales traction in the UK slows down and Airtasker is unable to gain sales traction in other countries (e.g., US, New Zealand, Ireland).

Additional COVID-19 variants result in continue lockdowns.

Overall

Airtasker is a two-sided marketplace for local service providers with a capital-light business model, high inside ownership, and a long runway for growth, both in domestic and international markets. I initiated a small starter position in August 2021 at around the current share price and intend to aggressively add to the position if Airtasker is able to execute on the thesis outlined above.

Best,

Jordan Martenstyn