Lemonade: Not an Investment for the Faint of Heart

Lemonade: Not an Investment for the Faint of Heart

Lemonade is a high-risk, high-reward investment with an enormous TAM and a management team with ambitions to disrupt insurance as we know it. This quarter had something for the bulls and the bears.

Lemonade (NYSE:LMND) is an insurance business founded in 2015 with grand ambitions to disrupt the process of purchasing insurance and handling insurance claims. Using artificial intelligence and lessons learned from renowned behavioural economists such as Dan Ariely (who served as Lemonade’s Chief Behavioural Officer and was awarded a Nobel Prize in 2008), Lemonade has simplified the process of purchasing insurance, enabling customers to purchase policies within minutes through conversation with a chat bot (AI Maya). As of March 2022, Lemonade offers five products: (1) renters, (2) homeowners, (3) pet, (4) term life, and (5) car insurance.

I’ve published two previous articles on Lemonade, including a 9-000 word deep dive on the business and a shorter article discussing their recent Q3 2021 results.

In the midst of geopolitical conflict, rising inflation, and tighter monetary policy, we have seen large factor rotations out of ‘growth’ stocks into ‘value’ stocks. And Lemonade (along with their peers) has been no exception. See the below drops in share price over the past 12 months for Lemonade and their insurtech competitors:

Oscar Health (NYSE:OSCR) - down 77%.

Lemonade (NYSE:LMND) - down 82%.

Hippo (NYSE:HIPO) - down 82%.

Root Insurance (NASDAQ:ROOT) - down 86%.

Metromile (NASDAQ:MILE) - down 93%.

Despite this sharp drop in share price, I remain bullish on Lemonade’s long-term prospects, particularly at the current valuation. In this article, I delve into their recent Q4 2021 results, including both the ‘good’ and ‘bad’ aspects of their results.

The ‘Good’ of Lemonade’s Q4 2021 Results

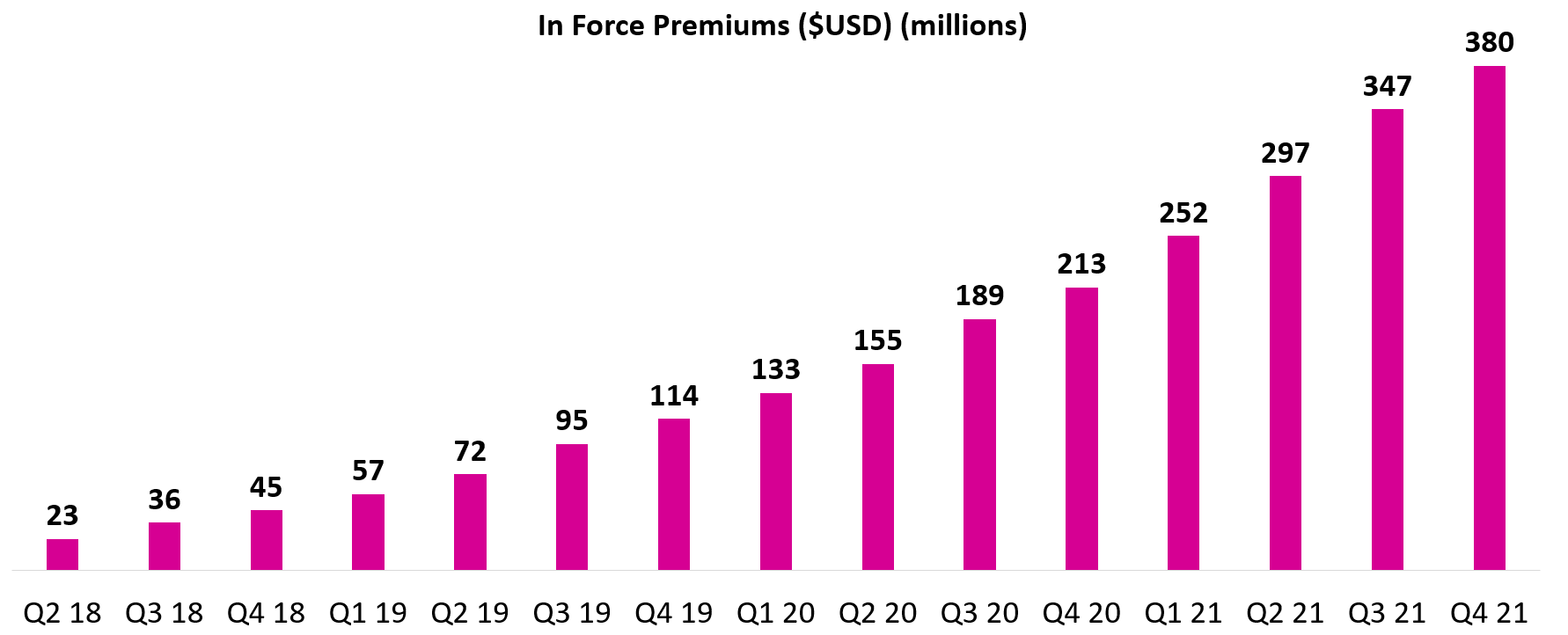

1) Top-line growth remains strong

In Q4, Lemonade reported in force premium (IFP) of $380m, which was up 10% QoQ and 78% YoY. Lemonade guided for $380-384m of IFP, so this ends Lemonade’s unbroken streak since IPO of outperforming IFP guidance. Taking a step back, Lemonade has reported the following compound annual growth rates (CAGR) for IFP:

2-year IFP CAGR: 83% pa.

3-year IFP CAGR: 104% pa.

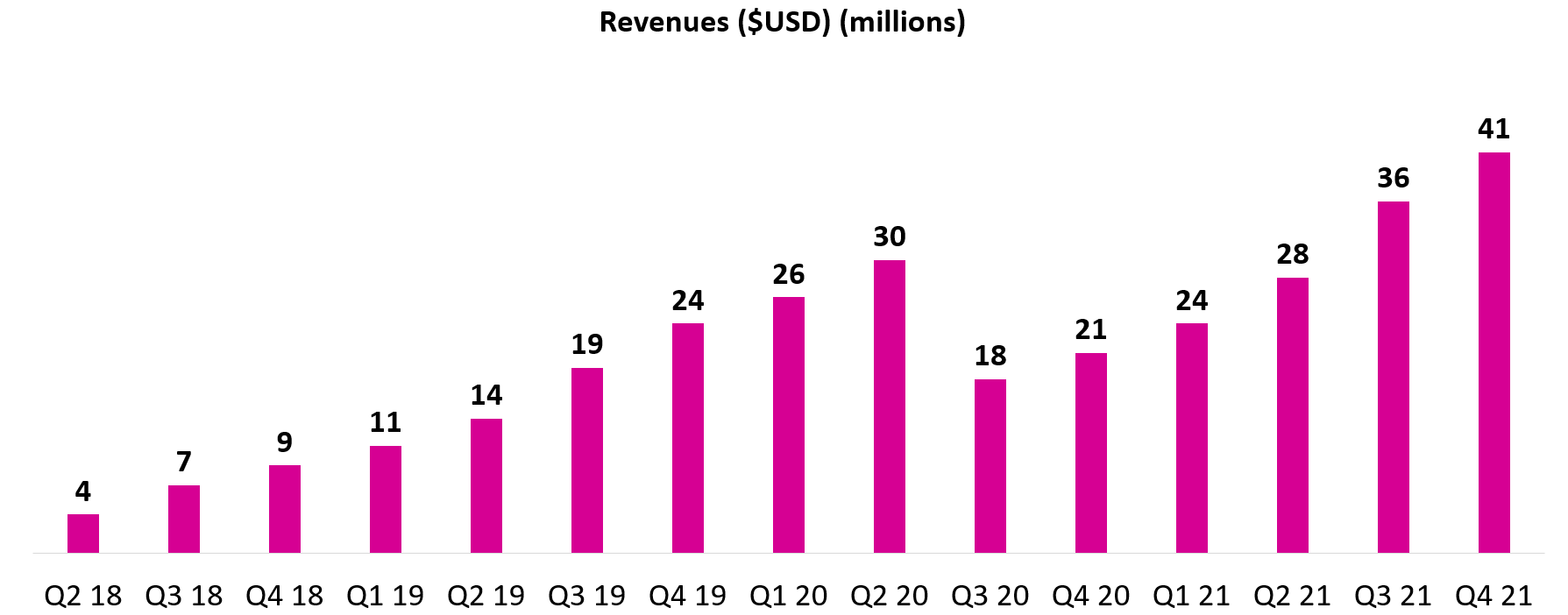

In Q4, Lemonade also reported $41.0m in revenue, which was up 15% QoQ and 100% YoY, and ahead of their guidance for revenue of $39-40m. Revenue in 2021 increased 36% to $128.4m, however, keep in mind that changes in Lemonade’s reinsurance agreements in Q3 2020 makes YoY revenue comparisons difficult. Until YoY comparisons normalise on an annualised basis, IFP is the best metric to judge Lemonade’s top-line growth.

2) Continued growth in customers and average premium per customer

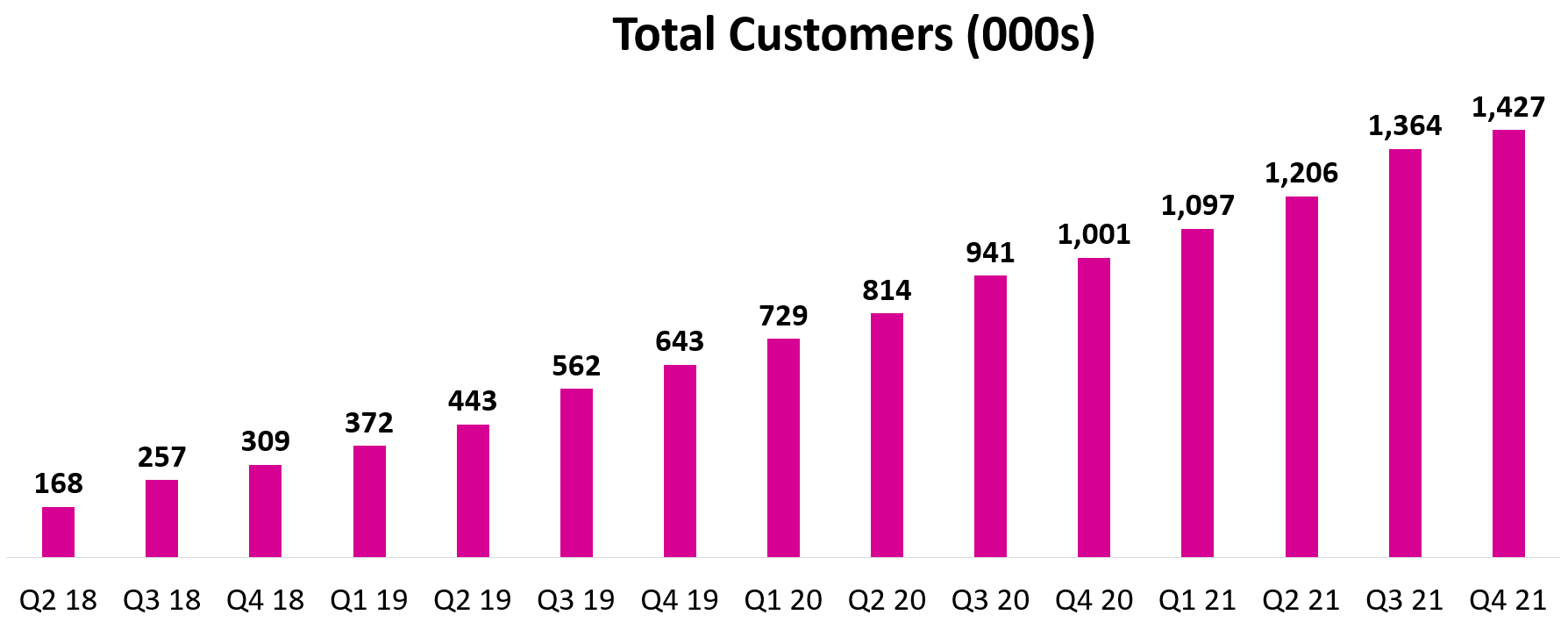

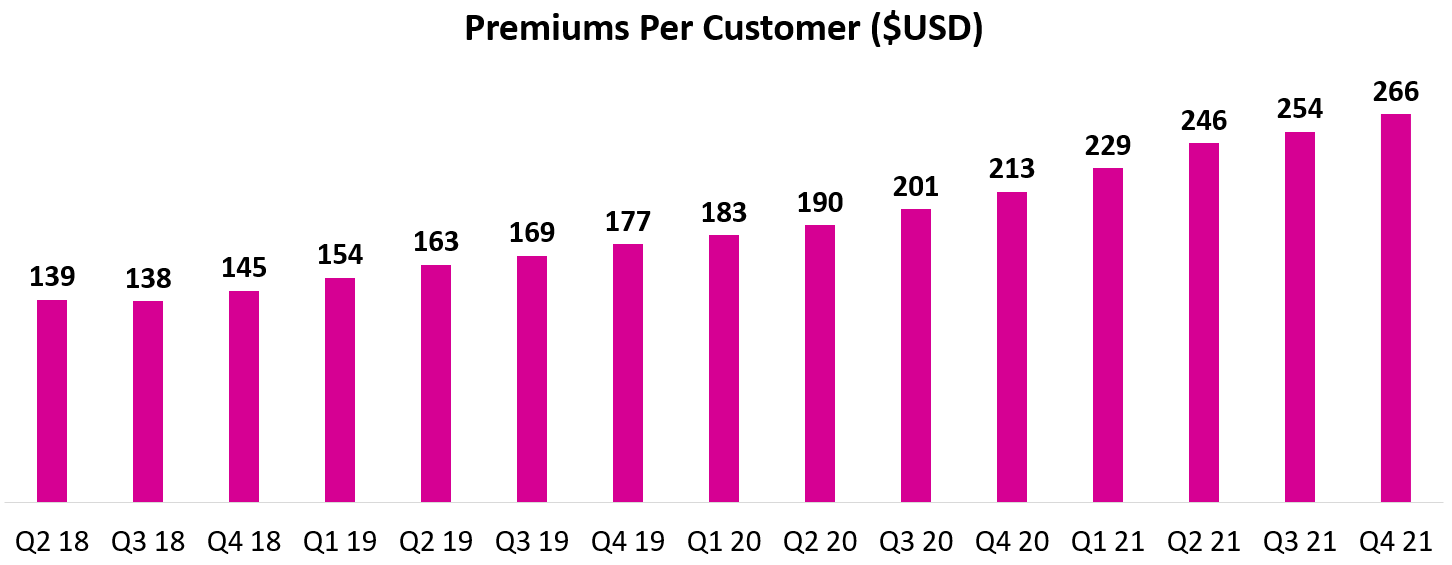

Lemonade’s two core drivers of top-line growth are: (1) total customer count and (2) average premium per customer. As investors, we want to see more customers using Lemonade’s products and those customers spending more with Lemonade over time.

In Q4, Lemonade added 63,000 customers (+5% QoQ; +43% YoY), reaching 1.43m total customers. It is important to note that while Q4 tends to be Lemonade’s weaker quarter for new customer additions, this was Lemonade’s weakest quarter of customer growth since IPO. While disappointing, a natural deceleration in growth rates is to be expected as Lemonade expands their customer base, so I am not concerned. Over the medium-term, customer growth has compounded at the following rates:

2-year customer CAGR: 49% pa.

3-year customer CAGR: 67% pa.

Lemonade also reported an average premium per customer of $266 (+5% QoQ; +25% YoY), consistent with their historical growth rate since 2018 of 3-8% sequential growth each quarter. On a YoY basis, Lemonade’s growth in average premium per customer has exceeded 20% each quarter since Q4 2020 as Lemonade expands their product range and customers bundle multiple products together.

As Lemonade rolls out their car insurance product over the next 12-18 months, I expect average premium per customer to continue to compound at greater than 20% pa throughout 2022 and 2023, providing a strong tailwind for IFP and revenue growth.

Lemonade’s CFO Timothy Bixby re-iterated the importance of Lemonade’s bundling strategy in their Q4 conference call:

“I think it’s important to note that there’s a real or certainly a growing potential there with our ability to cross-sell and bundle where the cost of that incremental IFP is significantly lower, in some cases, 0. And so that’s where we’ll start to see what I think is a declining reliance on direct customer acquisition and an improving balance between growing existing customers and bringing in new customers.”

3) Greater insight into Lemonade’s path to profitability

Lemonade’s CEO Daniel Schreiber provided more insight this quarter on Lemonade’s path to profitability. In short, Lemonade expects losses to peak on an annualised basis in 2022, with YoY improvements in EBITDA margins from 2023 onwards. Here are some interesting comments from Daniel on the conference call:

“We project that 2022 will be a year of peak losses with our EBITDA improving in each subsequent year.”

“We’re probably 6 to 9 months away from our peak losses and we expect to see our losses decline with each every successive year and our EBITDA margin to be on a steady path of improvement in the years to come, and that will chart a clear and steady path to profitability.”

“I do expect to be able to display trend lines for both expense ratios and loss ratios that begin to evidence the force and the power of what we’ve been building and for those to manifest towards the end of this year.”

It was reassuring to get concrete guidance on the path of Lemonade’s EBITDA margins in the medium-term as their cash burn continues to be a significant concern for investors (me included).

4) Initial traction for car insurance appears promising … but Metromile integration will not happen overnight

To date, Lemonade’s car insurance product is only available in one US state (Illinois), so it is tough to judge customer demand with such a small sample size. However, initial traction appears promising. Lemonade reported that car insurance saw 3x the traction of pet insurance in the same time period after launching in Illinois. While there could be some data dredging going on here (e.g., "traction” might refer to total IFP which is misleading because car insurance policies cost more than pet insurance policies), it is worth noting that Lemonade’s pet insurance product has grown to represent almost 20% of Lemonade’s IFP within 18 months of launching.

Lemonade also mentioned that 3/4 of car customers in Illinois bundled car insurance with another Lemonade product, which is a strong testament to Lemonade’s multi-product offering. If customers with an existing Lemonade insurance product bundle with car insurance as it becomes available in all 50 US states, Lemonade should see large increases in both premiums per customer and LTV/CAC ratio (unit economics).

Lemonade expects to close the Metromile acquisition in Q2 2022 and be able to offer car insurance to most Lemonade customers within 12 months of that point (i.e., mid-2023). Thus, while Metromile’s existing IFP (around $117m) will be added to Lemonade’s book of business after the acquisition is closed in mid-2022, it will take another 12 months (at the earliest) until Lemonade can offer car insurance to all 50 US states.

5) A compelling valuation after a steep contraction in multiple

As of 12th March 2022 (and using data from Koyfin), Lemonade has a market cap of $1.16b, with $271m in cash and cash equivalents, and $802m in investments, resulting in total cash, cash equivalents, and investments of $1.07b. In other words, the market is valuing Lemonade’s core business, excluding their cash and investments, for $90m. Keep in mind that Lemonade ended 2021 with $380m of IFP, 1.43m customers, and $128m of revenue.

If we exclude cash and cash equivalents, Lemonade trades on a forward EV/sales multiple of 4.4x, after reaching a ludicrous 100x forward multiple in January 2021 (note: I was NOT bullish at these levels). While most established US-listed public insurance companies, such as Progressive Corporation (NYSE:PGR), Allstate (NYSE:ALL), Cincinnati Financial (NASDAQ:CINF), and Travelers (NYSE:TRV) trade on forward EV/sales multiples of 1.0-2.5x, it is worth noting that the 3-year revenue CAGRs of these businesses range from 5-21% (compared to 55% for Lemonade which includes a change in reinsurance agreement; 3-year IFP CAGR is 104%).

I agree that comparing Lemonade’s EV/sales ratio with that of larger incumbent competitors is overly simplistic as these incumbents are profitable; however, the purpose of the exercise is to show that the large premium afforded to Lemonade in the first half of 2021 due to their phenomenal growth rates has evaporated.

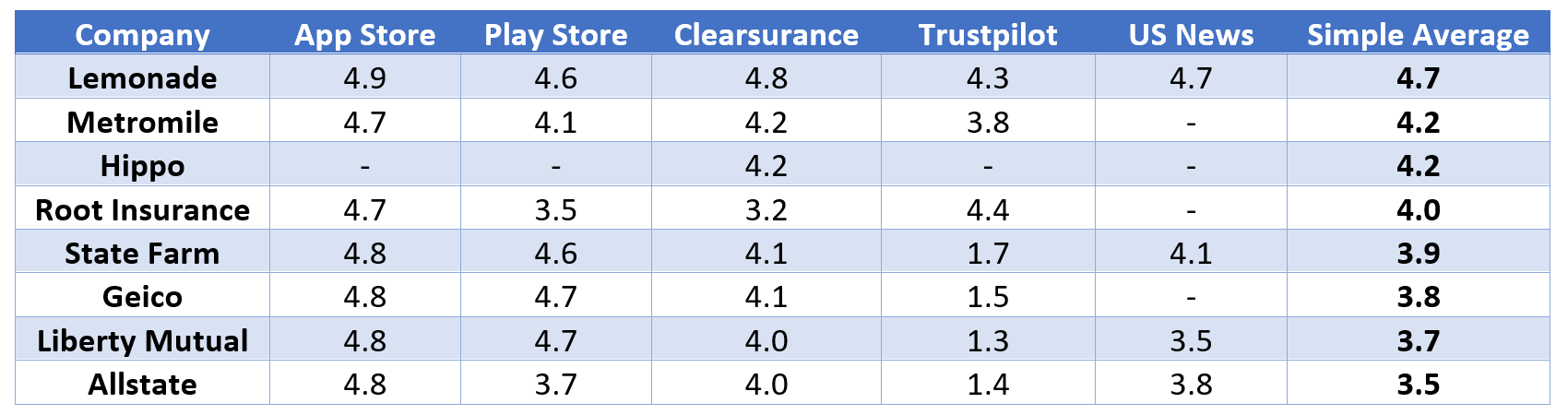

While I agree that there are legitimate concerns about Lemonade’s fluctuating loss ratios and high cash burn, it is undeniable that Lemonade has a strong brand that resonates with 1.43m millennial and gen z customers, and product reviews well above those of their incumbent and modern competitors. The current valuation appears to assume that Lemonade will continue bleeding cash forever, forcing them to dilute existing shareholders to oblivion just to survive. While this is a non-zero probability event, I believe the current valuation more than compensates patient investors for that risk.

The ‘Bad’ of Lemonade’s Q4 2021 Results

1) 2022 guidance calls for slower top-line growth

Lemonade put forth the following guidance in core metrics for 2022:

IFP growth of 39-42% (excluding Metromile acquisition) or IFP growth of 70% (including Metromile acquisition).

Revenue growth of 57-60% (excluding Metromile acquisition).

Adjusted EBITDA loss of $275m to $290m.

At first glance, headline guidance for organic growth in IFP of 39-42% seems like a marked slowdown from the 78% growth reported in 2021, however, context is needed here. Through the acquisition of Metromile, Lemonade is replacing their existing car insurance product which would’ve been rolled out in 2022 and 2023. Thus, while IFP gained from the acquisition of Metromile is inorganic in a technical accounting sense, some of this growth in IFP would have occurred in 2022 regardless as Lemonade launched their own car insurance product. See the below comments from CEO Daniel Schreiber in the conference call:

“We’ve never thought about it [Metromile] as a stand-alone business or something that is additive in terms of its business, it’s replacement … So in our operational plans, we don’t think of Metromile as being a bolt-on or an addition, but being organic and being part of our car launch plans. I say that because that gives you our perspective on the year, which is that we’re going to see a 70% year growth based on the guidance that we’re providing, and this year was a 78% growth. So it’s very much in line with the kind of growth that we saw in ‘21.”

With this context in mind, the deceleration in IFP growth is not as large as it first seems. However, one could also argue that 39-42% growth in IFP represents the ‘true’ growth rate for Lemonade’s four products (excludes car insurance as little revenue was generated from car insurance in 2021), which is also a fair point.

It is also worth noting that CEO Daniel Schreiber made the following comment in the conference call, which is consistent with the perspective that there will not be a marked slowdown in growth in 2022:

“I think 2022 will be very similar in terms of its top line and other metrics growth to ‘21.”

2) Another spike in loss ratios

In Q4, Lemonade reported a large spike in both gross (96%) and net loss ratios (98%) due to some unforeseen damage to insured properties. While I am understanding of increasing loss ratios due to major natural disasters outside of Lemonade’s control (e.g., the Texas Freeze in Q1 2021), I am less forgiving in this case because Lemonade admitted to being under-reserved for the claims. I also found it frustrating how vague Lemonade management were in disclosing what caused this elevated loss ratio in the conference call. I would prefer for them to be upfront with investors, own their mistake, and learn from it, rather than beating around the bush.

Notwithstanding this blip, Lemonade again re-iterated as in previous quarters that loss ratios for each of their newer products are improving with time. However, this trend gets masked when assessing total loss ratios as the growth in newer products (with higher loss ratios) exceeds the growth in more mature products (e.g., renters insurance with a lower loss ratio), resulting in Lemonade’s newer products becoming a greater contributor to overall loss ratios with each successive quarter. If Lemonade remained a sole provider of renters insurance and had not expanded into other products, their loss ratios would be sub 70% and much more stable, but their TAM would be much smaller.

“Nonetheless, we’ve seen a few quarters with elevated loss ratios. The underlying cause is the welcome and intentional shift in our business mix with U.S.-based renters comprising less than half of the book today compared to about 2/3 a year ago. The lines of business that have captured that share, home and pet, demonstrate higher loss ratios than our more mature, stable renters book.” (Lemonade COO Shai Wininger)

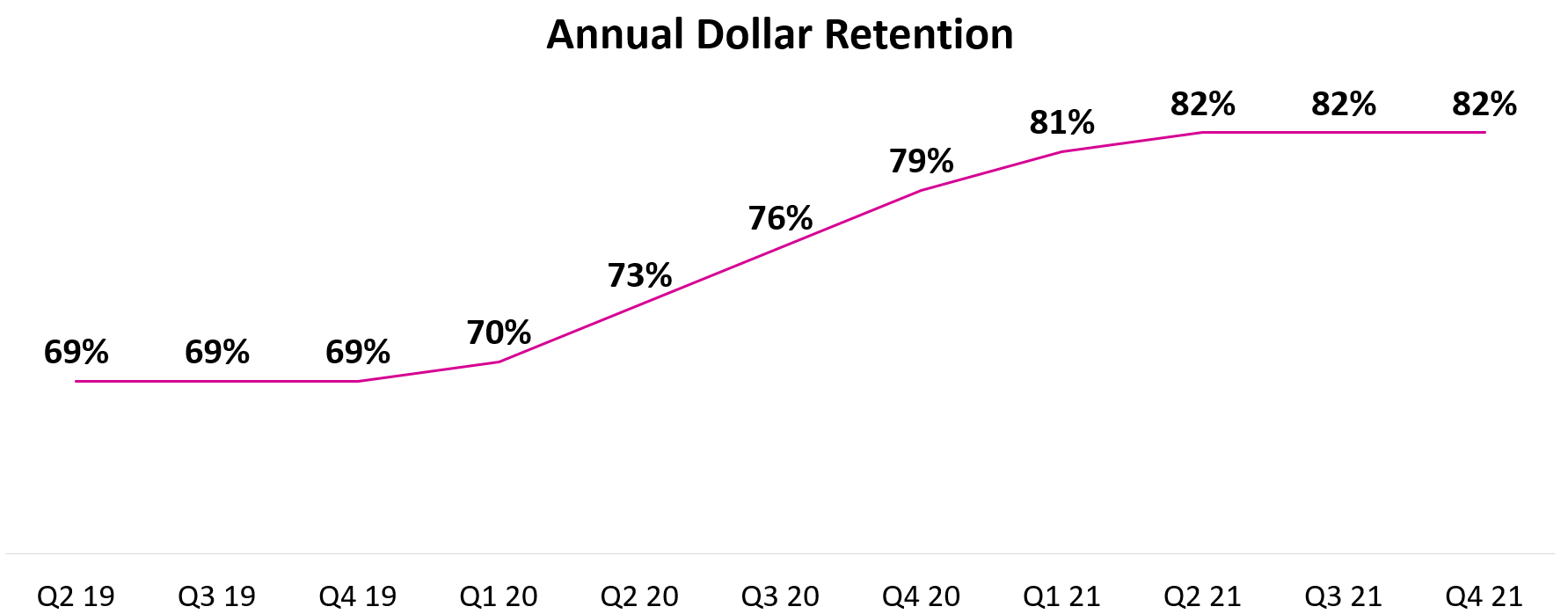

3) A plateau in annual dollar retention rate

In my last article on Lemonade’s Q3 2021 results, I discussed the concerning trend that annual dollar retention rate appeared to be plateauing in the low 80% range. Indeed, Q4 confirmed this trend with Lemonade’s annual retention rates again coming in at 82%.

While in line with industry standards, I would expect Lemonade’s retention rates to be much higher than competitors given their exceptional customer satisfaction ratings. One possible explanation for this lower-than-expected retention rate could be that (1) most of Lemonade’s customers are millennials and gen z, and (2) almost half of their IFP comes from renters insurance, so this demographic might be less stable and more price sensitive than older customers, while also being more susceptible to cancelling policies due to major life transitions (e.g., moving back home or into a college dorm, losing a job, re-enrolling for higher education, etc). While this explanation could account for Lemonade’s lower-than-expected annual retention rates, I am nonetheless disappointed to see this plateau in the low 80% range.

4) Horrendous net losses and operating cash outflows

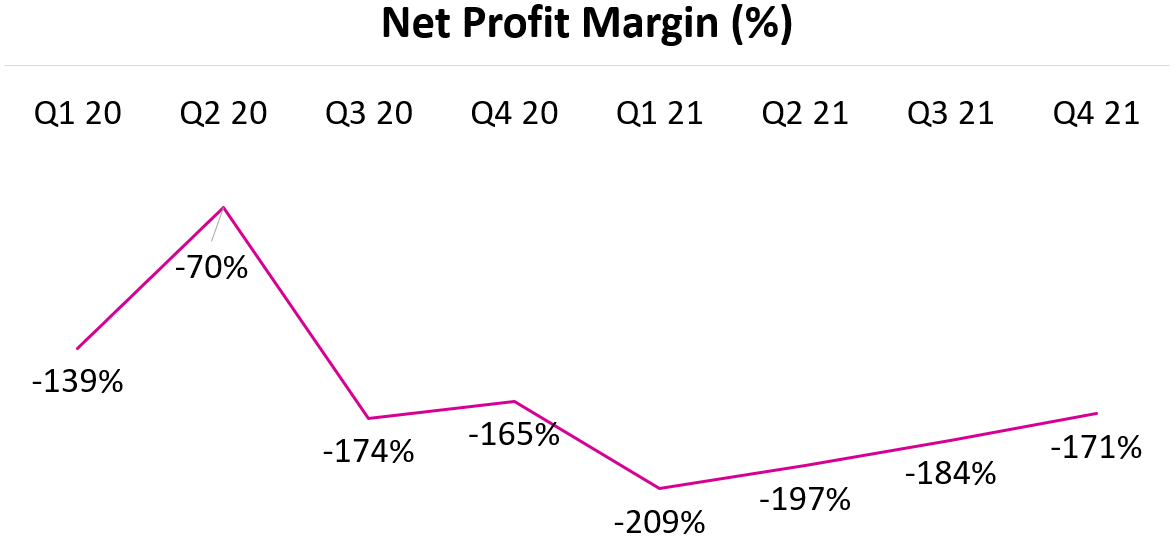

Lemonade reported a net loss of $70m in Q4 2021, which more than doubled from a net loss of $34m in Q4 2020. For the whole of 2021, Lemonade had a net loss of $241m, up 98% from a net loss of $122m in 2020. Over the past four quarters, net loss as a percentage of revenue (net profit margin) has reduced with each successive quarter from -209% to -171%, but these still represent enormous losses by any measure.

While these net profit margins are horrendous and leave a lot to be desired, context is also important. Over the past 24 months, Lemonade has launched four new products (homeowners, pet, term life, and car insurance) and expanded into new geographical regions, such as France and the Netherlands. All of these moves require capital and large upfront investments/expenses, however, it takes time for Lemonade to reap the rewards of these investments and generate premiums/revenue. As long as unit economics are positive and trending in the right direction (note: Lemonade called out improving unit economics several times in their conference call), such investments are justified, provided that the business has the balance sheet to withstand such losses. However, I would like Lemonade to begin disclosing unit economics so we can judge them for ourselves.

As of Q4 2021, Lemonade had $1.07b in cash, cash equivalents, and investments (note: $271m is cash and cash equivalents) with no long-term debt. However, Lemonade reported an operating cash outflow of $145m in 2021 and an adjusted EBITDA loss of $184m. As mentioned earlier in this article, Lemonade expects losses to peak in 2022 with an adjusted EBITDA loss of $275m to $290m, so let’s assume this translates to operating cash outflows of $200-250m. With $271m in cash and cash equivalents, Lemonade would be forced to raise capital in the next 12 months, which would result in significant dilution for shareholders if carried out at the current price.

However, two things make me optimistic that Lemonade can weather this storm without needing to raise capital in 2022:

Lemonade has no plans to launch a new product in the immediate future which will help to reduce future expenses; and

Through their acquisition of Metromile, Lemonade will acquire their cash and cash equivalents, which totalled $121m as of Q4 2021 (note: this represents 98% of their current market cap of $123m).

Thus, Lemonade’s current cash balance if we take into account Metromile is closer to $400m, which provides a larger buffer for expected operating cash outflows of around $200-250m in 2021.

“Over the past 6 years since we founded the company, we’ve raised about $1.5 billion, all told, of which $1.1 billion remain in the bank. And in fact, the acquisition of Metromile brings with it not only great licenses and IFP and talented people and technology but a fair amount of cash as well. So our cash position is going to receive something of a little boost in the coming months.” (Lemonade CEO Daniel Schreiber)

5) Increasing stock-based compensation

Lemonade reported $44m of stock-based compensation (SBC) in 2021, which equated to 34% of revenue. In 2022, Lemonade expects SBC to rise to $80m, which represents a jump to 39% of revenue, assuming the midpoint of their 2022 guidance.

I understand that SBC is needed to retain talent and helps to reduce cash expenses, but rising SBC as a percentage of revenue is not something I want to see as an investor. I expect high amounts of SBC to become a talking point for bears throughout 2022.

6) Rising headcount - counter to the narrative of Lemonade’s technological advantage?

One of the things that most attracted me to Lemonade was their vertical integration on a ‘digital substrate’ which automated operational procedures that most larger incumbents required human intervention to complete (e.g., process of purchasing insurance, handling certain claims, etc.). Such automation is attractive as a business proposition because it reduces costs while also increasing the speed at which customer needs and requests can be serviced, resulting in higher customer satisfaction (which we see materialise in online customer reviews).

However, Lemonade reported a 97% increase in global headcount in 2021 to 1,119 staff. Most of these new hires were in customer-facing departments or product development teams. The increase in product development staff makes sense given the rapid pace of Lemonade’s product launches in the past 24 months, but I am concerned about the increase in customer support staff as this to some extent questions Lemonade’s technological advantage over competitors. I would like updated metrics from Lemonade as to the proportion of claims being handled through AI Maya and AI Jim to get a sense of their current automation standards. In the absence of such figures, I will be monitoring the change in headcount throughout 2022 to see if this trend continues.

Conclusion

Overall, Lemonade remains a high-risk, high-reward investment. Lemonade has an enormous TAM and a management team with skin in the game and ambitions to disrupt insurance as we know it.

On the positive side, Lemonade continues to report excellent growth in premiums, revenue, customers, and average premium per customer, is seeing strong traction with their car insurance product, and trades at their lowest relative valuation since IPO.

However, there are a number of question marks about the business, including their spike in loss ratios, plateau in annual dollar retention rate in the low 80% range, widening losses, and increasing SBC as a percentage of revenue.

In hindsight, Lemonade went public too soon. It is a classic VC investment with an enormous 'right-tail’ outcome that requires significant upfront investments and bleeding losses to build a critical mass of customers and disrupt incumbents. However, I believe the recent drop in share price (> 55% in 2022 alone) which values Lemonade’s core business at around $90m more than accounts for the above risks and neglects the tremendous progress that Lemonade has made since IPO. The market seems to be concerned about the risk of a capital raise in 2022 but I would be surprised to see this happen due to the cash that will be acquired after the Metromile acquisition, bolstering Lemonade’s cash position to almost $400m. In doing so, Lemonade will be able to continue delighting their customers and executing on their path to long-term value creation. I leave frustrated shareholders with the following quote:

“Good things come to those who wait.”